Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Top 3 Reasons To Buy a Home Before Spring

If you’re planning to buy a home this year, you may be focused on the spring market. And hoping that when spring does hit, you’ll see:

- Mortgage rates drop a little more.

- More homes hit the market.

But here’s what most buyers don’t realize. Buying just a few weeks earlier could mean paying less, dealing with less stress, and feeling less rushed.

Here are three reasons why accelerating your timeline over the next few weeks could actually be a better play.

1. Holding Out for Lower Rates May Not Pay Off

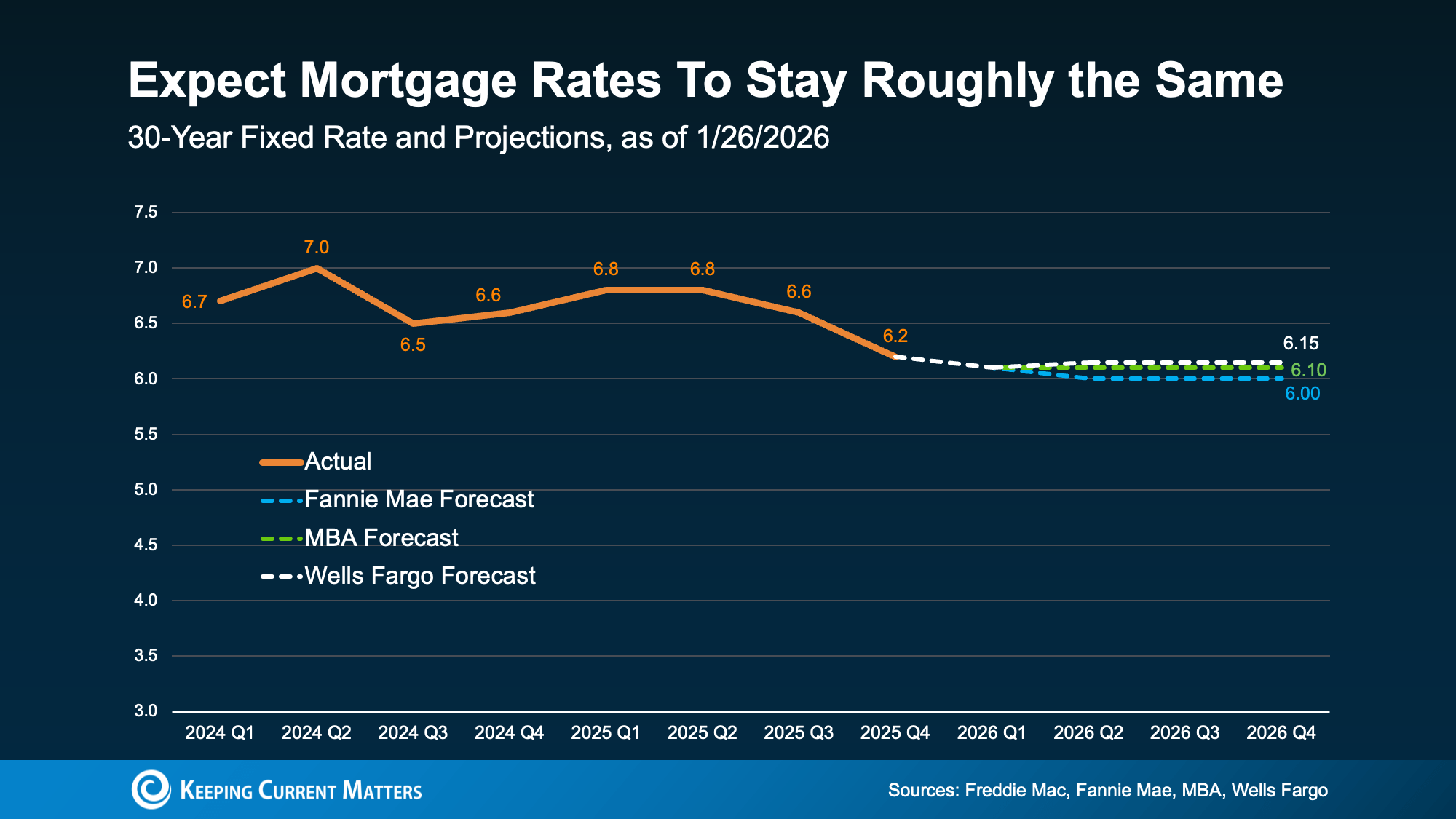

A lot of buyers are hoping mortgage rates will fall even further. But that’s not the best strategy. Here’s why. Experts are pretty aligned on this: rates are expected to stay roughly where they are.

Forecasts throughout the industry all point to the same thing: rates are projected to be in the low-6% range this year (see graph below):

That’s not a bad thing, especially if you consider how much rates have already come down. Over the past 12 months, they’ve dropped roughly a full percentage point. And for many buyers, that means affordability has already improved more than they may realize.

So why wait a few more weeks just for more buyers to jump in and act as your competition? You already have a window right now. As Chen Zhao, Head of Economics Research at Redfin, explains:

“House hunters should know that this may be near the lowest mortgage rates fall for the foreseeable future.”

2. Spring Means More Competition + More Stress

Speaking of competition, the spring market is popular for a reason, but with popularity comes pressure. With more buyers active at that time of year, you’ll have to move faster once you find a home you like. And no one likes feeling rushed.

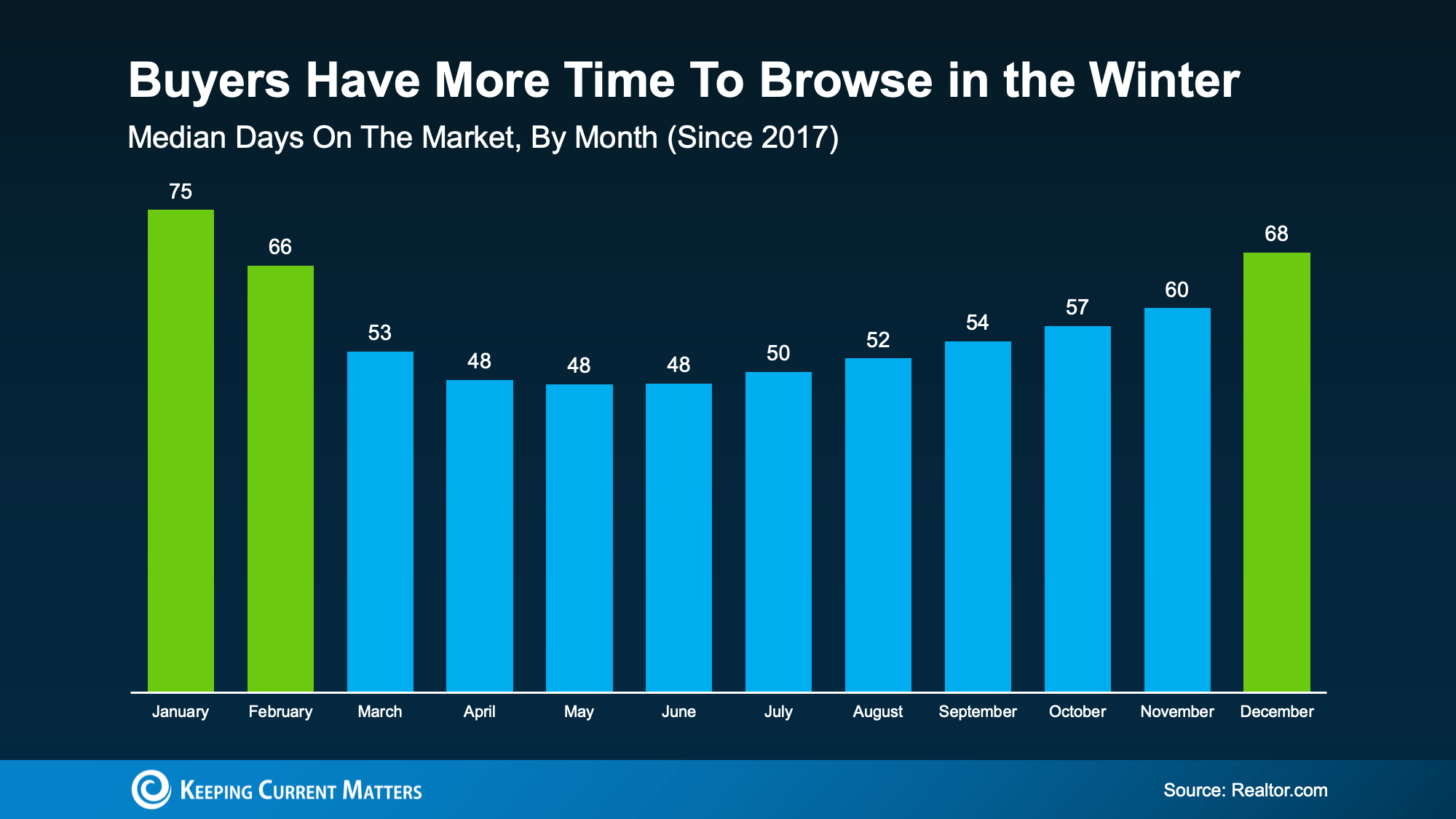

But buy now and you have more time to browse. Fewer people are looking, so homes sit longer.

You can see this play out in the data from Realtor.com (see graph below). In winter months, it takes an average of about 70 days for a home to sell. In spring? That drops to about 50 days. That’s a 20-day swing – and that pace is going to be more stressful.

Homes sell faster in the spring, and slower in the winter. And that can be a worthwhile perk for buyers who want to get ahead before their decisions start to feel rushed.

3. Prices Tend To Rise When Competition Heats Up

And here’s something most buyers forget to factor in. Prices usually respond to demand. So, when demand is higher, prices are too. Bankrate explains:

“Spring and early summer are the busiest and most competitive time of year for the real estate market . . . home prices tend to be steeper to reflect the increased demand.”

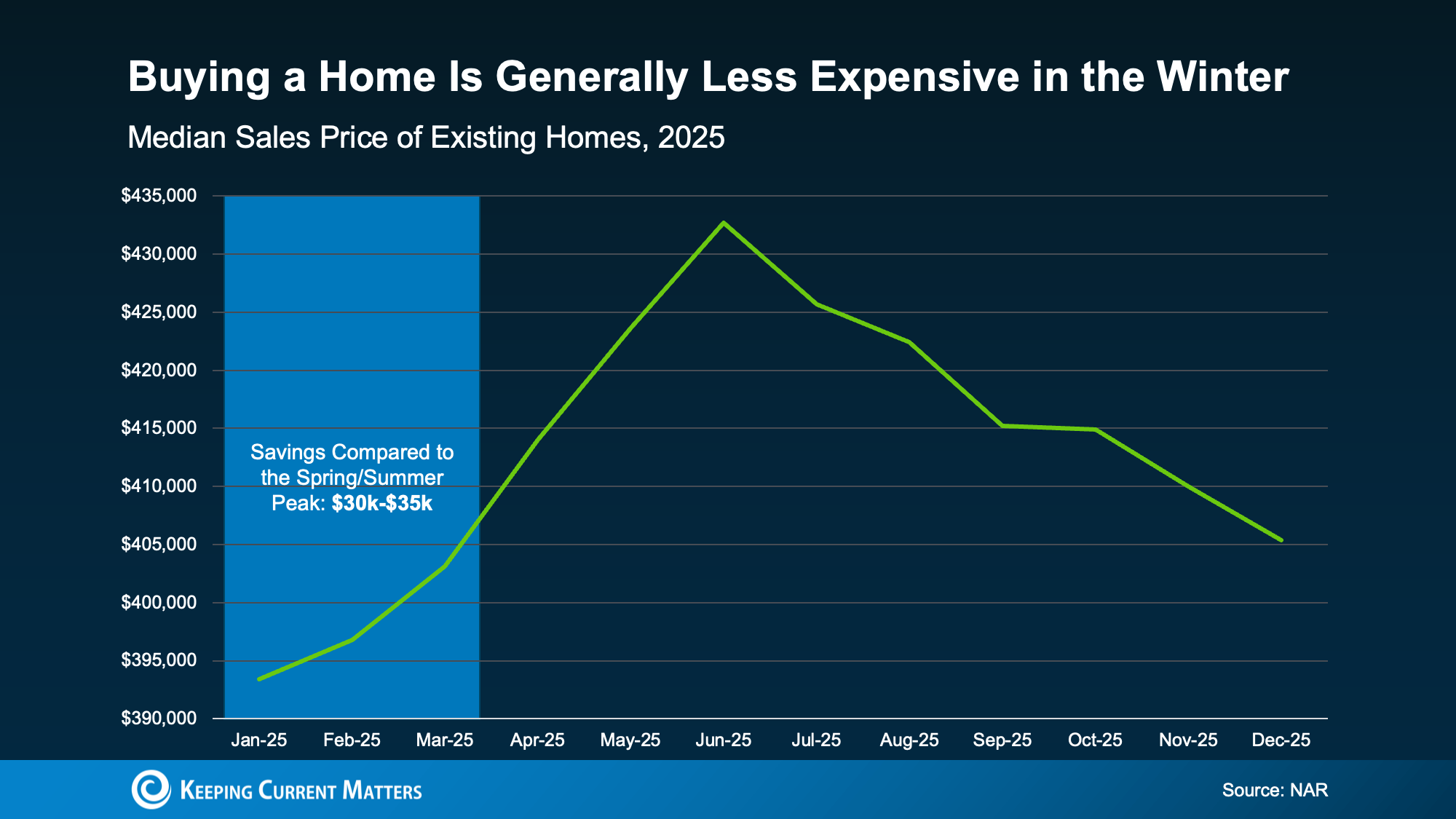

In fact, data from the National Association of Realtors (NAR) shows that in 2025, buyers who purchased in the beginning of the year saved roughly $30,000–$35,000 compared to those who bought when prices peaked in the spring or early summer.

And let’s be honest, for a lot of buyers today, every little bit of savings helps. That’s why buying just a few weeks earlier, before prices ramp up, will be better for you and your wallet.

Bottom Line

Buying a few weeks before spring isn’t about rushing. It’s about choosing to be ahead of the curve and knowing you want more leverage, less stress, and meaningful savings.

If you’re ready and able to buy now and want to get the ball rolling, give me a call!

Article provided by Keeping Current Matters

The Price You Set Can Make (or Break) Your Sale

There’s one decision you’re going to make when you sell that determines whether your house sells quickly, or it sits. Whether buyers make an offer, or scroll past it. Whether you walk away with the maximum return, or you end up cutting the price later.

And that’s your asking price.

The #1 Mistake Sellers Make Today: Trusting the Wrong Number

If you’re thinking of moving and trying to figure out what your house may sell for, it’s tempting to start with an online home value tool. They’re fast, free, and easy. And you don’t have to talk to anyone. But here’s the problem: they don’t know your house.

And that can be a bigger drawback than you realize.

Where Online Estimates Fall Short

Online tools often lag behind the market. They look in the rearview mirror, relying on closed sales and delayed information. And in that sense, they’re using incomplete data.

That’s not a miss in how these systems are built. Some information just isn’t available online. Bankrate explains:

“While these tools can be a useful starting point, keep in mind that they typically do not provide the most accurate pricing. Algorithms can only rely on the information available; they can’t account for things like a home’s condition or renovations made since the last public information was updated.”

They can’t see:

- The unique features that make your house special

- All the work you’ve put in to keep it in good condition

- Or, how in-demand your specific neighborhood is right now

So, while they may do a good job in some cases, they can’t be as accurate as a local agent who has boots on the ground day in and day out.

In a market where buyers have more options, a seemingly small margin of error can cost you thousands if you price too low, or weeks of lost momentum and time if you price too high.

If you want to sell for the most money and in the least amount of time, you don’t want the fast answer on how to price your house. You want the right one.

That’s why the savviest homeowners today don’t rely on algorithms when it actually matters. They rely on people, specifically trusted local agents.

What an Expert Agent Brings to the Table

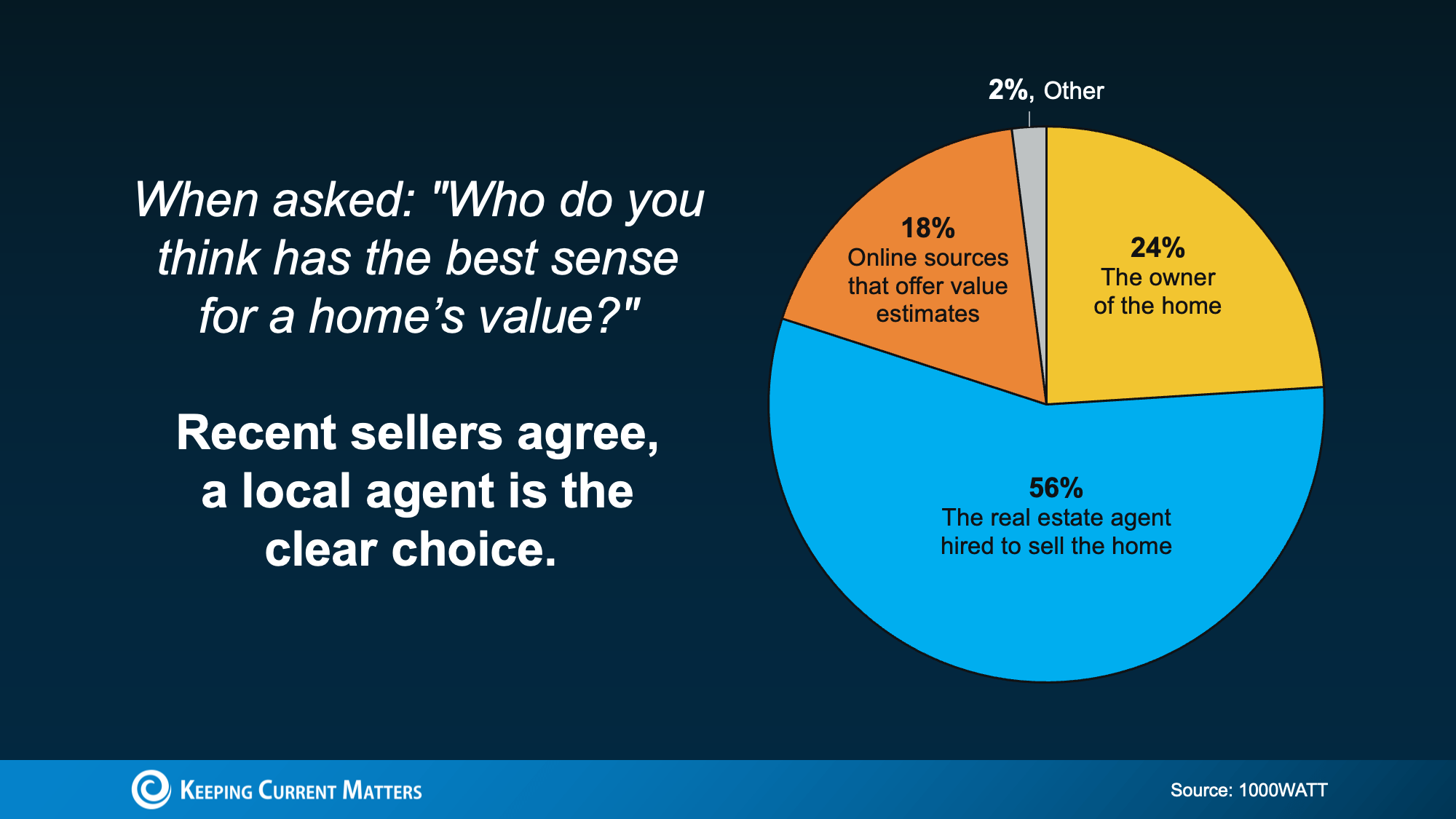

According to 1000WATT, sellers overwhelmingly believe real estate agents have the best sense of a home’s true value, far more than any automated tools.

That confidence isn’t accidental. As Bankrate puts it:

“A professional appraiser or real estate agent can visit the home in person, assess the neighborhood as a whole as well as the individual property, perform more thorough market research, and consider subjective details.”

And those details matter. A skilled local agent doesn’t just pull reports. They know what’s happening right now:

- What buyers are paying this month, not last month, or even last year

- How your home compares to the current competition in your neighborhood

- Which features add value based on what buyers are willing to pay for today

- How to price your house to create urgency in this market

And once an agent steps foot in your house, they may even find your online estimate undershot your value. So, if you stuck with the estimate you got online, you’d actually be leaving money on the table. And no one wants that.

Bottom Line

While online tools can give you a rough starting point, only a local expert can give you a price that actually works.

If you want to know the right number for your house, not just the easiest one to find, give me a call. I would love to help you, no obligation, just clarity.

Top Real Estate Agent in Granite Bay & Roseville, CA | Suzanne Volkman, Coldwell Banker Realty

When navigating today’s competitive real estate market in Granite Bay, Roseville, and communities throughout Placer, Sacramento, and El Dorado Counties, professional guidance and local expertise make a measurable difference.

Suzanne Volkman is a Broker Associate with Coldwell Banker Realty and a Top 100 Agent in the Sac/Tahoe Region, providing residential real estate representation across all price ranges and property types. Her practice is built on disciplined pricing strategy, direct client advocacy, and hands-on transaction oversight from consultation through closing.

Suzanne holds advanced professional credentials, including Certified Residential Specialist (CRS), Pricing Strategy Advisor (PSA), Accredited Buyer’s Representative (ABR), Global Luxury Specialist, Performance Management Network (PMN), and the Realtor® Emeritus distinction from the National Association of REALTORS®. She is a past President of the Placer County Association of REALTORS® and the Placer County Women’s Council of REALTORS®, reflecting long-standing leadership and service within the industry.

Clients work directly with Suzanne—not a handoff team—ensuring continuity, accountability, and clarity throughout every stage of the transaction.

For a confidential consultation or current market analysis, contact:

Suzanne Volkman, Broker Associate – Coldwell Banker Realty

🌐 https://suzannevolkman.com

📞 (916) 847-1445

✉️ suzanne.volkman@cbnorcal.com

DRE #00702179

Is Buyer Demand Picking Back Up? What Sellers Should Know.

The housing market hasn’t felt this energized in a long time – and the numbers backing that up are hard to ignore. Mortgage rates have eased almost a full percentage point this year, and that shift is starting to wake up buyers.

Home loan applications have risen. Activity has picked up. And sellers who step in early could benefit from the momentum long before the competition catches on.

Let’s take a look at what’s happening behind the scenes and how you can take advantage of it.

When Rates Come Down, Buyer Activity Goes Up

In today’s market, buyer demand is closely tied to what happens with mortgage rates. As rates come down, applications for home loans go up. Rick Sharga, Founder and CEO of the CJ Patrick Company, explains it like this:

“We’re in an incredibly rate-sensitive environment today, and every time we’ve seen mortgage rates drop into the low-to-mid 6% range, we’ve seen an influx of buyers hit the market.”

And that’s exactly what the data shows. More people who were sidelined are applying for mortgages again now that borrowing costs have come down. Of course, that’s going to ebb and flow just like rates ebb and flow. But the bigger picture is, there’s been improvement as a whole since rates started coming down.

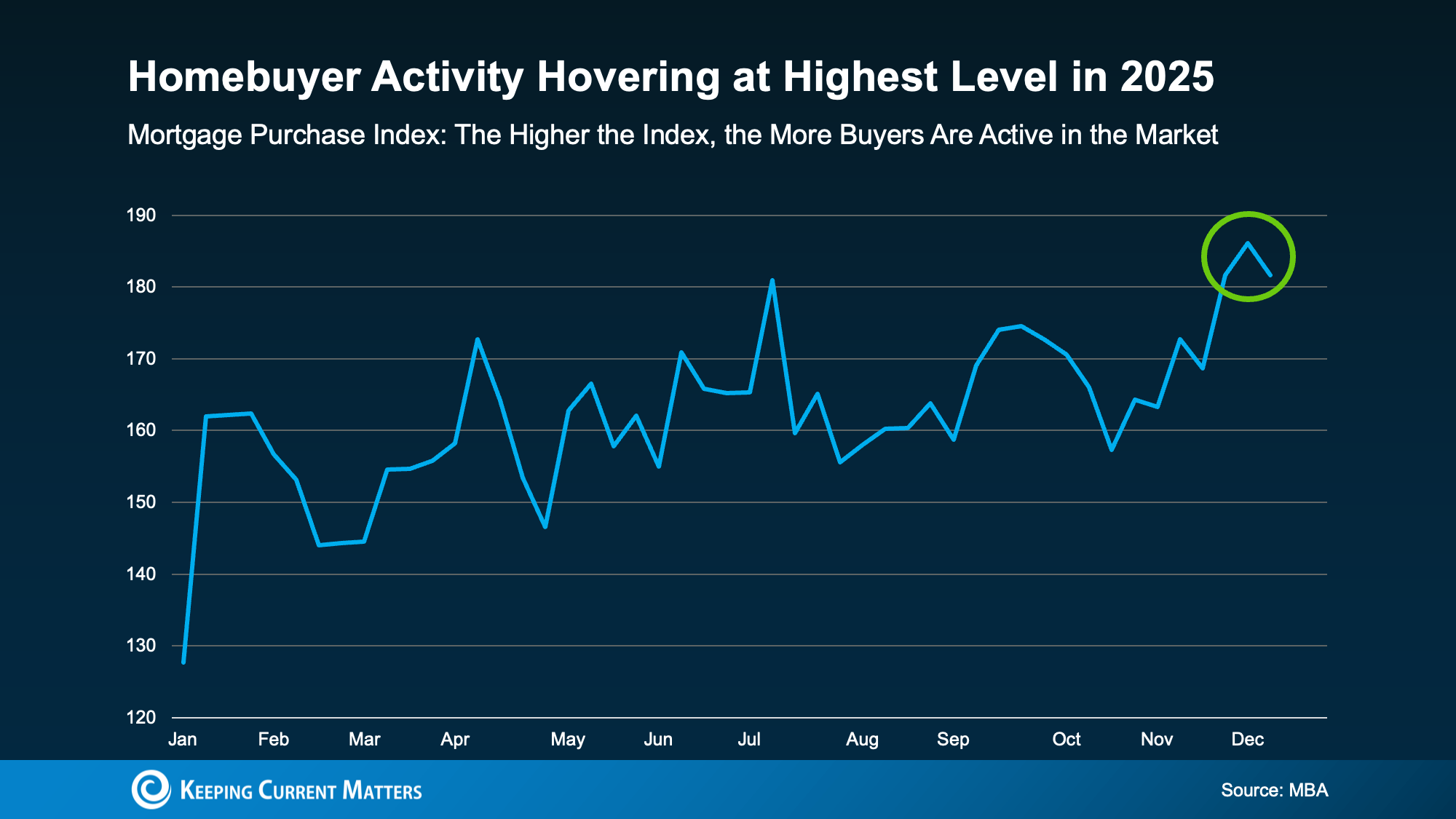

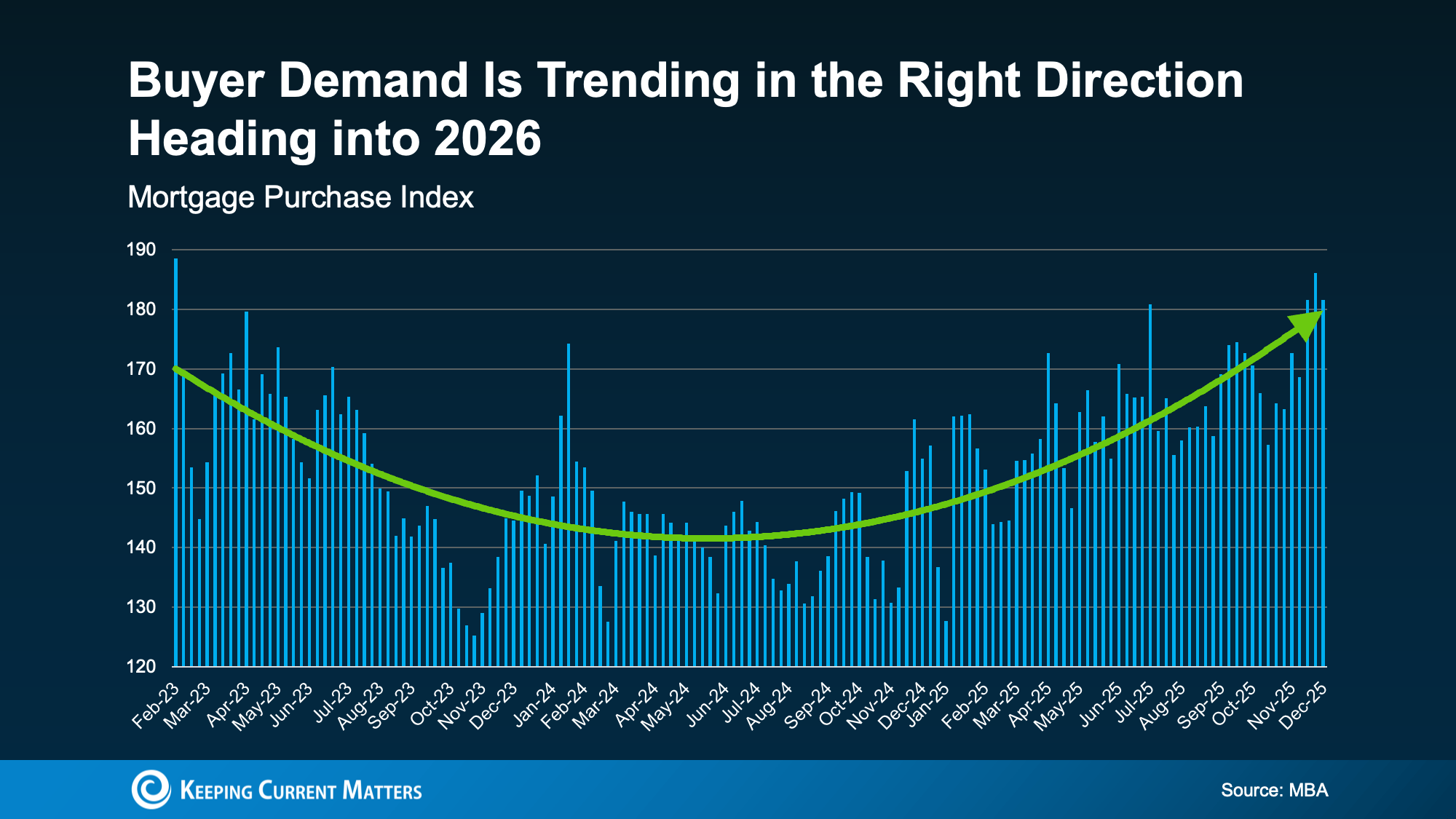

In fact, the Mortgage Bankers Association (MBA) shows the Mortgage Purchase Index is hovering at the highest level so far this year:

And that’s not the only sign of optimism. MBA also shows mortgage applications recently hit their highest point in almost 3 years too. A clear sign demand is moving in the right direction heading into 2026:

And just in case you were wondering, it’s not just pent-up demand coming out of the government shutdown that slowed some of the processing of government loans for a month or so. If you look back at the last graph, you’ll see the steady build-up of momentum throughout the entire year.

The big takeaway for you is this. Now that rates have come down, buyers are starting to ease back into the game. And that’s turning into real contracts on homes just like yours.

Home Sales Are Rebounding

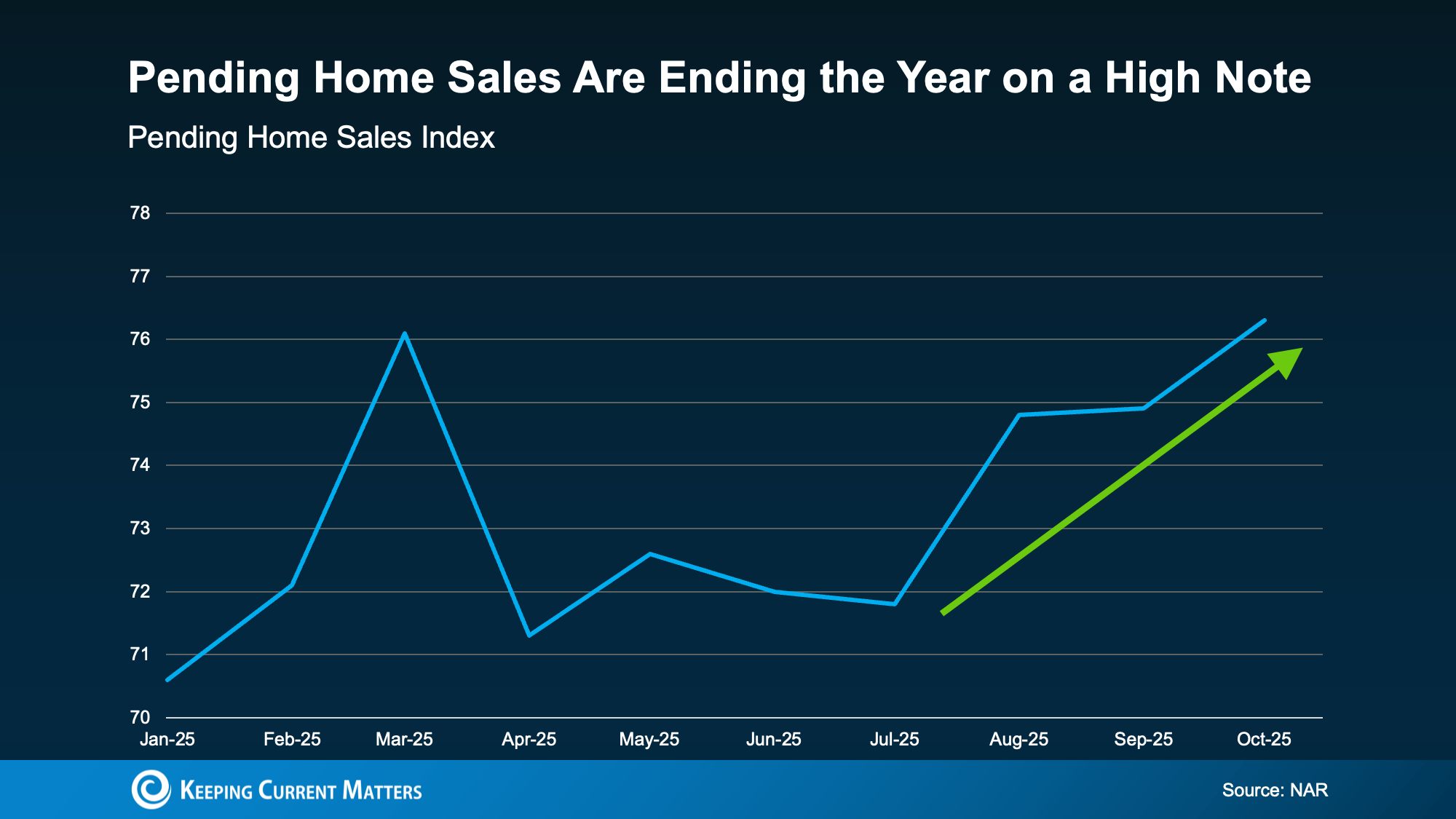

Just to really drive home that this is trending in a good direction, the most recent report from the National Association of Realtors (NAR) shows pending home sales (homes that are under contract) are picking up too. The Pending Home Sales Index is also at the highest it’s been all year (see graph below):

And that means the market is ending the year on a high note and headed into 2026 with renewed energy. While that may not seem like a big shift, it’s a rebound worth talking about.

Pending home sales are a leading indicator of where actual sales are going. If more homes are going under contract, it’s a good sign more homes will actually close over the next two months, ultimately boosting sales. This could be part of why experts project home sales will inch higher in 2026 than they were in 2025 or in 2024.

Of course, this may ebb and flow a bit as we see some year-end volatility with mortgage rates. But, it shouldn’t be enough to change this overall trend. Expert forecasts say rates should stay pretty much where they are throughout 2026. That means the stage is set for this momentum to continue going into the new year.

What This Means for You

Here’s the opportunity. Selling now means:

- More buyer demand. As affordability improves, you could see more buyer traffic and home showings (if your house is priced and staged right). And the best part? The buyers who are re-engaging feel like they’ve already waited too long for this moment. So, they’ll be eager to move.

- Being ahead of the curve. Listing sooner rather than later puts you ahead of the game, before other sellers realize something’s shifted.

Whether you’ve been putting off selling because you thought buyers weren’t buying, or you took your house off the market because you weren’t getting any bites, this is your sign to act.

Bottom Line

Want to know what’s happening with buyer activity in your area, and what it could mean if you want to sell your house in the new year?

Let’s talk about getting your house listed in early 2026, so you can take advantage of this momentum building in the market.

You May Not Want To Skip Over That House That’s Been Sitting on the Market

When you see a house that’s been sitting on the market for a while, the reaction is almost automatic. You start thinking:

- What’s wrong with it?

- Why hasn’t anyone bought it yet?

- Am I missing something?

That mindset made sense a few years ago. But in today’s market, you may actually miss out.

More Time on Market Isn’t Automatically a Concern Anymore

A few years ago, homes sold in just a matter of days. Sometimes, hours. Anything that lingered longer than that raised concerns. But that’s no longer the baseline.

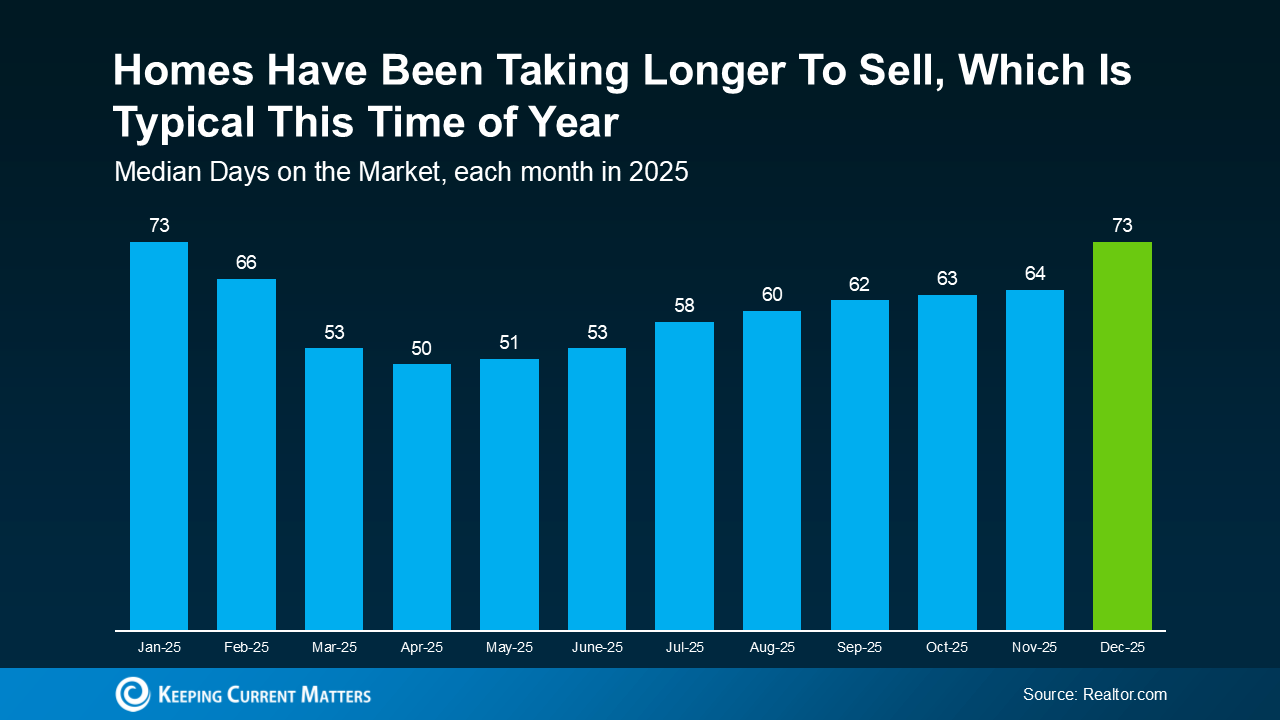

Inventory has grown. Buyers have more choices. And homes are taking longer to sell across the board. Those are some of the reasons why the typical time it takes a home to sell has climbed this year:

And it’s not that 73 days is slow. That’s actually pretty normal for this time of year. It just feels slow because you heard so much about houses being snapped up in the buying frenzy a few years ago.

And it’s not that 73 days is slow. That’s actually pretty normal for this time of year. It just feels slow because you heard so much about houses being snapped up in the buying frenzy a few years ago.

That shift alone explains a lot of what you’re seeing. It’s not necessarily that there’s anything wrong with the house itself. Although, let’s be honest, sometimes that is the case.

Most of the time today, a house that’s taking longer to sell simply means:

- There are a lot of homes for sale in that area

- The seller priced a little too high at first

- The home didn’t photograph as well online

- Buyers passed it over for flashier listings nearby

- The timing just wasn’t right when it first hit the market

None of those are necessarily deal-breakers.

What Buyers Often Get Wrong About These Listings

Because even though you may assume a house that hasn’t sold must have hidden issues, the reality is, that’s not always the case. And, if the house does have issues, it’ll show up quickly in your inspection.

That’s information you can use to negotiate. Not a reason to walk away automatically. And in many cases, that’s where buyers find the best deals.

The key is knowing which homes that have been sitting for a while are worth a second look – and which ones aren’t. That’s why working with a local agent makes a real difference. They’ll be able to look at disclosures and more to help you uncover hidden gems other buyers may overlook.

Bottom Line

A home sitting on the market isn’t always a warning sign. Sometimes it’s an overlooked opportunity.

If you want help identifying which homes are worth a second look (and which ones to skip), give me a call and I can help you decide.

*Keeping Current Matters*

Why Pre-Approval Should Be Your First Step – Not an Afterthought

Finding the right home feels exciting – but being pre-approved for your loan is what makes it possible. Whether you’re planning to buy soon or still just thinking about it, getting pre-approved is one of the best moves you can make. Here’s why.

1. What Is Pre-Approval, Really?

Pre-approval is much more than a guess. It means a lender has reviewed your finances (things like your income, assets, credit score, debts, and savings) and told you how much they’re willing to let you borrow for your loan.

It’s basically a reality check for your home search, so you can make sure it aligns with your budget and shop confidently when you’re ready to go.

2. Why It’s a Power Move (Especially Right Now)

The housing market’s been shifting lately with mortgage rates moving, prices moderating, and inventory rising. So, knowing what you’re working with in the current market is a big reason why pre-approval matters. Here’s what it gives you:

- Clarity: You’ll know what you can afford before you fall in love with a house that’s potentially out of reach.

- Confidence: Sellers will take your offer seriously when they see you’re pre-approved because you’re not a risky buyer.

- Control: If rates come down and you want to jump on the moment, you’re already a step ahead with your plan.

As Experian explains:

“. . . you’ll want to make sure you receive your preapproval letter before you start looking at homes so you can submit a strong offer as soon as you find what you want. The process can take anywhere from a day to a few weeks, so if you procrastinate, you may lose out to a competing offer.”

And once you find a home you want to put an offer on, pre-approval has another big perk. It not only makes your offer stronger, it shows sellers you’ve already undergone a credit and financial check. As Greg McBride, Chief Financial Analyst at Bankrate, says:

“Preapproval carries more weight because it means lenders have actually done more than a cursory review of your credit and your finances, but have instead reviewed your pay stubs, tax returns and bank statements. A preapproval means you’ve cleared the hurdles necessary to be approved for a mortgage up to a certain dollar amount.”

Translation: Pre-approval helps you make stronger, more informed decisions – and it helps you avoid missing out on a home or getting stuck on the sidelines when the right one hits the market. Because the reality is, competition might be lower these days, but desirable homes (especially the ones that are priced well) still go quickly.

3. Don’t Wait Until You’re “Ready”

Think of it this way: pre-approval doesn’t mean you’re buying a house tomorrow. It just means you’ll be ready when the time comes. And most pre-approvals are good for 60–90 days and can be refreshed easily if your plans change.

So, here’s a good place to start. Ask yourself this question: “If the perfect home came along today, would you be ready to make an offer?”

If your answer is “not quite,” then pre-approval is your next step.

Bottom Line

Pre-approval doesn’t box you in. It opens doors.

In today’s market, buyers who win aren’t the ones who wait. They’re the ones who plan. So, if you’re even thinking about buying in the next few months, get ahead of the game by connecting with your trusted lender. If you would like a referral to an agent that I have worked with, give me a call.

We can help you understand what how the process works and walk you through every step along the way, so when the right home pops up, you’re ready.

Thinking about Selling Your House As-Is? Read This First.

If you’re thinking about selling your house this year, you may be torn between two options:

- Do you sell it as-is and make it easier on yourself? No repairs. No effort.

- Or do you fix it up a bit first – so it shows well and sells for as much as possible?

In 2026, that decision matters more than it used to. Here’s what you need to know.

More Competition Means Your Home’s Condition Is More Important Again

Over the past year, the number of homes for sale has been climbing. And this year, a Realtor.com forecast says it could go up another 8.9%. That matters. As buyers gain more options, they also re-gain the ability to be selective. So, the details are starting to count again.

That’s one reason most sellers choose to make some updates before listing.

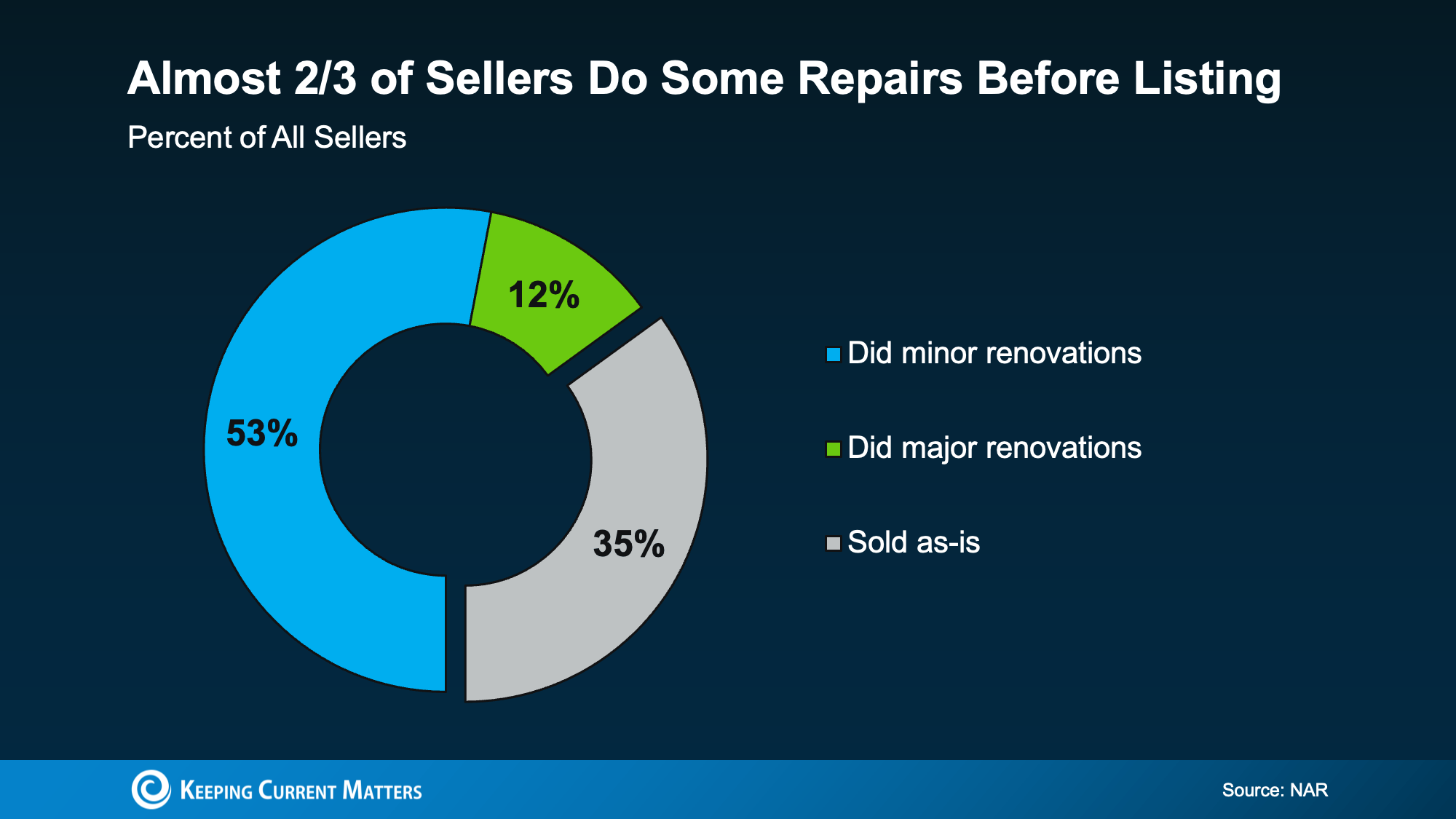

According to a recent study from the National Association of Realtors (NAR), two-thirds of sellers (65%) completed minor repairs or improvements before selling (the blue and the green in the chart below). And only one-third (35%) sold as-is:

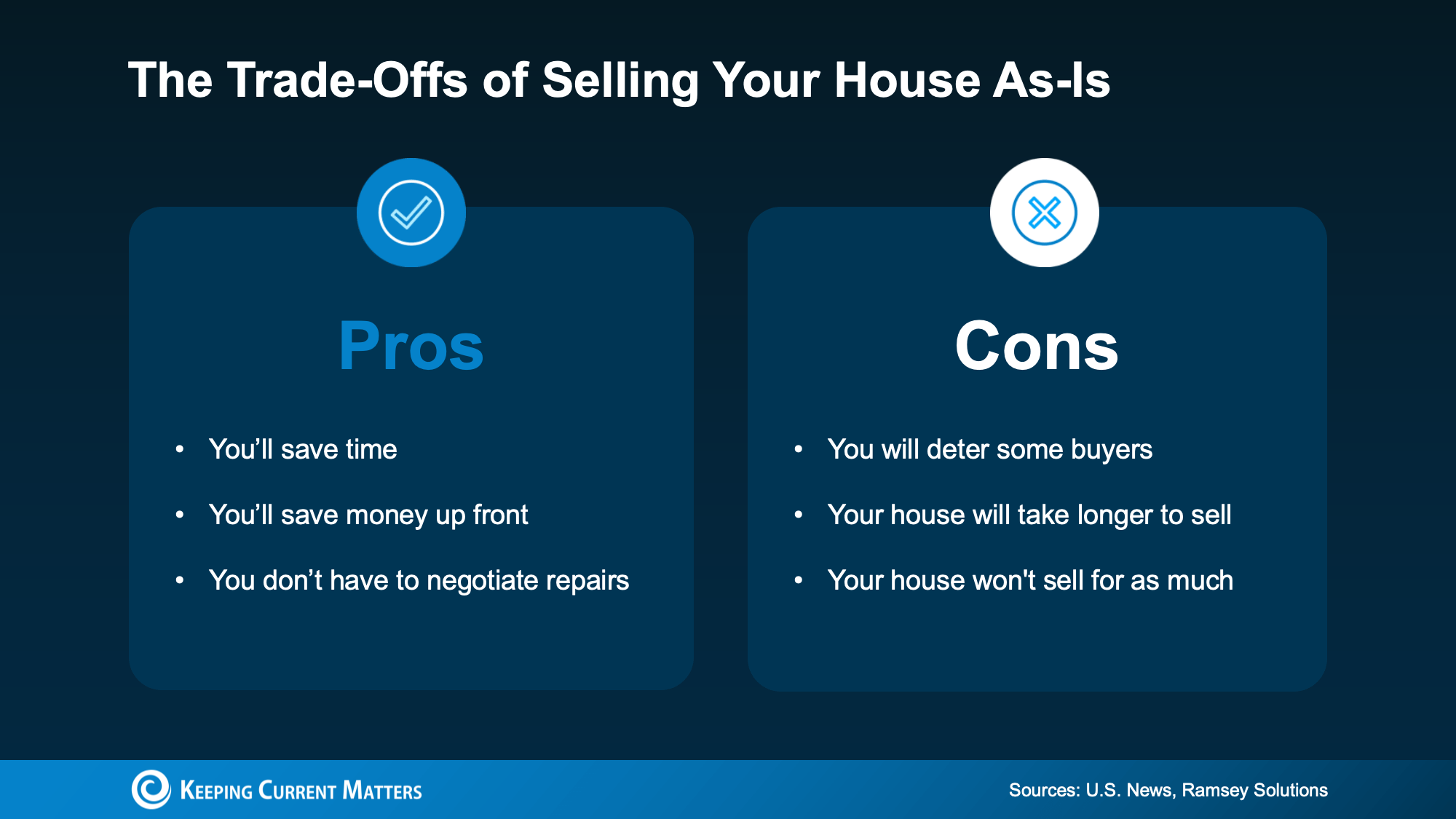

What Selling As-Is Really Means

Selling as-is means you’re signaling upfront that you won’t handle repairs before listing or negotiate fixes after inspection. That can definitely simplify things on your end, but it also narrows your buyer pool.

Homes that are move-in ready typically attract more buyers and stronger offers. On the flip side, when a home needs work, fewer buyers are willing to take it on. That can mean fewer showings, fewer offers, more time on the market, and often a lower final price.

It doesn’t mean your house won’t sell – it just means it may not sell for as much as it could have.

How an Agent Can Help

So, what should you do? The answer isn’t one-size-fits-all. It’s going to depend a lot on your house and your local market.

And that’s why working with an agent is a must. The right agent will help you weigh your options and anticipate what your house may sell for either way – and that can be a key factor in your final decision.

- If you choose to sell as-is: They’ll call attention to the best features, like the location, size, and more, so it’s easy for buyers to see the potential, not just the projects.

- If you decide to make repairs: Your agent can pinpoint what’s really worth the time and effort based on your budget and what buyers care about the most.

The good news is, there’s still time to get repairs done. Typically speaking, the spring is the peak homebuying season, so there are still several months left before buyer demand will be at its seasonal high. That means you have time to make some repairs, without rushing or stressing, and still hit the listing sweet spot.

The choice is yours. No matter what you end up picking, your agent will market your house to draw in as many buyers as possible. And in today’s market, that expertise is going to be worth it.

Bottom Line

While selling as-is can still make sense in certain situations, in some markets today, it may cost you. So, no, you don’t have to make repairs before you list. But you may want to.

To make sure you’re considering all your options and making the best choice possible, give me a call to have a quick conversation about your house.

Locked In Place: Why Millions of Homeowners Can’t Afford to Move

For years, America’s housing challenges have been framed as a simple supply-and-demand problem—low inventory, rising interest rates, and affordability constraints. But beneath those familiar headlines lies a deeper, structural issue we unintentionally created.

Today, millions of homeowners are wealthier on paper than ever before. They hold record levels of equity and historically low mortgage rates. Yet many of them cannot afford to move.

Not because they lack buying power.

But because moving no longer makes financial sense.

The Mortgage Lock-In Effect

Recent national data shows just how severe this gap has become. According to Realtor.com, the typical U.S. homeowner currently pays about $1,300 per month in principal and interest. Selling that home and purchasing a “typical” home today would require a monthly payment of approximately $2,236—a 73% increase in housing cost.

This growing gap is known as the mortgage lock-in effect. Homeowners who secured ultra-low rates during 2020–2021 are effectively trapped by them. Giving up a 3% mortgage to buy into today’s higher-rate, higher-price market often means paying significantly more—sometimes for a comparable or even smaller home.

The market isn’t frozen because people don’t want to move.

It’s frozen because moving comes with a financial penalty.

From Pandemic Stimulus to Market Stagnation

When mortgage rates fell below 3% during the pandemic, buyers surged into the market. Millions refinanced. Millions more purchased homes. Cheap financing softened the sting of rising prices, allowing values to climb rapidly—often 25% to 40% in many markets.

When inflation followed, rates snapped back sharply. Prices, however, did not.

The same mechanism that once encouraged mobility now suppresses it.

Federal housing research confirms this effect. A Federal Housing Finance Agency (FHFA) working paper estimates that rising mortgage rates have prevented millions of otherwise normal home sales by discouraging owners from listing their homes.

Why Homeowners Are Staying Put

It’s easy to assume homeowners stay because they “love their homes.” Many do—but that only tells part of the story. The real constraint is financial.

Homeowners face a stark choice:

-

Give up an exceptionally low interest rate

-

Buy into a market with both higher prices and higher borrowing costs

Even selling at a profit often results in higher monthly expenses and reduced flexibility. Equity becomes difficult to use when accessing it raises your cost of living.

This isn’t a lifestyle decision.

It’s a structural trap.

The Ripple Effect on the Housing Market

When homeowners can’t move, inventory shrinks. When inventory shrinks, affordability worsens—especially for first-time buyers.

This dynamic is already visible. Sellers are increasingly choosing to pull listings rather than cut prices or trade into higher-rate mortgages. According to Investopedia, delistings surged 45% year over year, highlighting the reluctance of owners to transact under current conditions.

Low inventory, in this context, is not the cause—it’s the symptom.

How We Unlock a Trapped Housing Market

This is not a short-term cycle. It’s a structural flaw that requires structural solutions:

-

Portable and assumable mortgages that allow buyers to take over existing low-rate loans

-

Incentives for downsizing and life transitions, particularly for long-time homeowners

-

Housing built for real demand, including townhomes, ADUs, and smaller, more attainable options

-

Modern mortgage products designed for flexibility and mobility—not just long-term lock-in

-

Greater transparency around equity use, so homeowners understand the true cost of moving

The Bottom Line

We built a housing system that rewards people for staying put and penalizes them for moving. The result is equity without freedom, ownership without mobility, and a market that struggles to function.

Mobility is not a luxury. It is a cornerstone of economic health and household well-being.

If we want a housing market that truly works, we must stop celebrating locked-in equity and start creating real pathways forward.

The American Dream only works if people can move with it.

Sources:

Source: Realtor.com – A 73.2% Spike in Monthly Payments for Moving Traps U.S. Homeowners in Place

Source: Investopedia – Delistings Jump 45% as Sellers Pull Homes Rather Than Cut Prices

Source: FHFA – The Lock-In Effect of Rising Mortgage Rates (PDF)

Why Buying a Home Still Pays Off in the Long Run

Renting can feel much less expensive and much simpler than buying a home, especially right now. No repairs, no property taxes, no worrying about mortgage rates – you just pay the bill and move on with your life.

But here’s the part people don’t talk about enough: renting doesn’t help you build your financial future. Meanwhile, homeowners grow their net worth just by owning a home.

So, if you’ve been wondering whether buying is still worth it, the long-term math is clearer than you might think.

Renting vs. Owning: How the Costs Really Compare

Let’s break down one of the key differences between renting and buying. When you rent, your payment goes to your landlord, and then it’s gone. When you own, part of your payment comes back to you in the form of equity (the wealth you build as the value of your home increases, and you pay down your home loan).

So, while renting may seem more affordable now, you have to remember it comes at a long-term cost: you’re not building your wealth. And it turns out, that’s a bigger miss than you may expect.

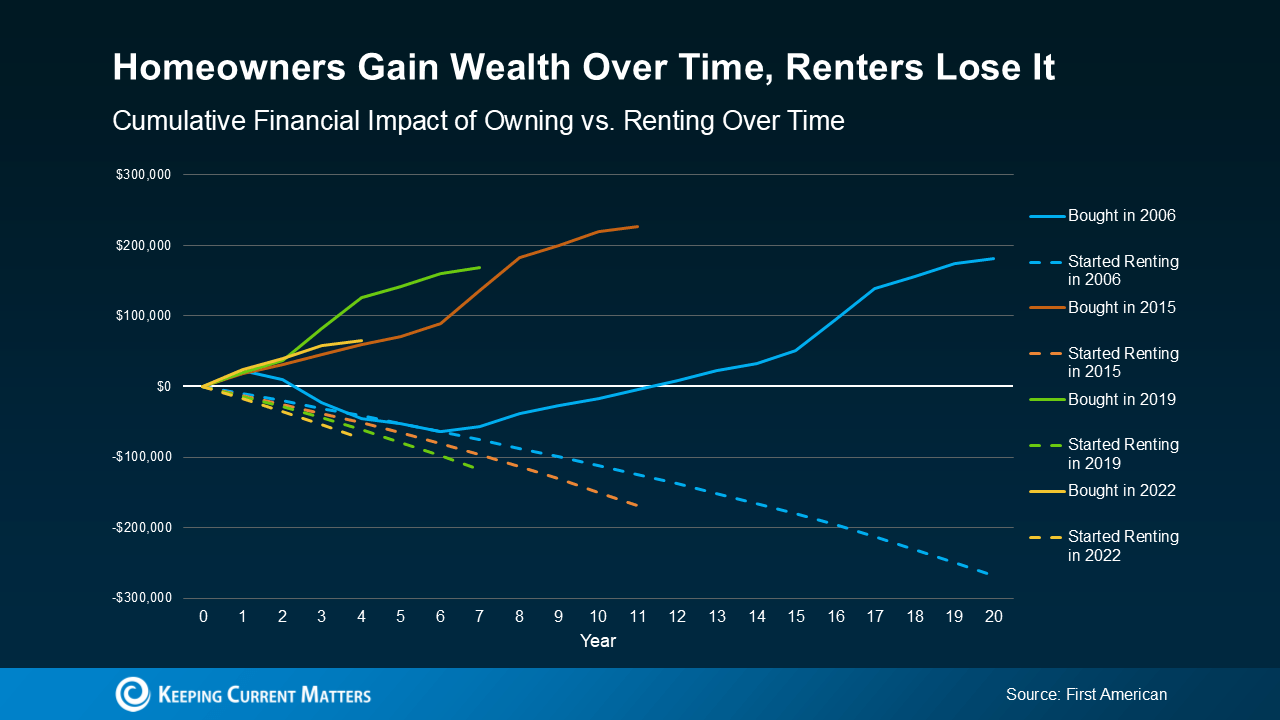

First American recently analyzed the long-term financial impact of renting versus owning a home. They compared mortgage payments, property tax, insurance, repairs, and maintenance against the equity gained through home price appreciation and paying down the mortgage. And they did that during several different time frames to see if it tells a consistent story:

- 2006: the start of the housing bubble

- 2015: 10 years ago

- 2019: just before the pandemic (the last normal years in the market)

- 2022: when mortgage rates jumped

In each time frame, two things were true: renters ended up losing money over time. And homeowners gained it.

Here’s some data so you can see this play out. Each color represents one of the key time frames. The solid lines show the buyer’s investment over time and how their net worth actually grew the longer they lived in their home. The dashed line represents the renter’s investment. In the end, they sank more and more cash into renting without gaining any financial benefit.

The takeaway is simple: time in a home builds wealth. Time renting doesn’t.

Basically, homeowners come out ahead. And the analysis shows that’s even after you factor in the other expenses that come with homeownership, like insurance, repairs, and property taxes. And that’s the case for every time frame First American looked into.

On the flip side, renters spent money on their rent, but didn’t gain any long-term financial benefit. That’s true no matter what window of time you look at in the study.

Now, that doesn’t mean buying always beats renting in the short term. But the longer you own, the wider the wealth gap becomes.

Affordability Is Starting To Improve

You might still be thinking, “Okay, but buying feels out of reach for me right now.” Fair.

The past few years haven’t been easy for buyers. But things are starting to shift. Mortgage rates have come down this year, home prices are softening, and incomes have been rising. And according to Zillow, typical monthly payments have gotten a little easier compared to this time last year. Not by a lot, but enough to make a difference.

No, buying isn’t suddenly easy. But it is easier than it was just a few months ago. And in the long run, history shows it’s worth it.

Bottom Line

Renting may feel less expensive today, but owning is what builds real wealth over time. And with affordability starting to improve, the path to homeownership may be opening up more than you think.

If you’re curious what buying could look like for you, give me a call and I can help you plan your next move, pressure-free.

Keeping Current Matters

Would You Let $80 a Month Hold You Back from Buying a Home?

I found this article from Keeping Current Matters very insightful! I hope you will too

Would You Let $80 a Month Hold You Back from Buying a Home?

A lot of buyers are stuck in “wait and see” mode right now. They’re watching rates hover a little above 6% and thinking, I’ll buy once they hit the 5s. Because who doesn’t want a better rate?

But here’s the thing: that 5.99% number might not save you as much as you think.

Affordability is still a challenge. There’s no question about that. But the market has given savvy buyers a head start. Mortgage rates have already come down over the past few months. And the drop we’ve seen saves you more than you’d think.

How Much You’ve Already Saved, Without Realizing It

Let’s put some real numbers to it. Rates peaked for the year in May when they inched above 7%. But since then, they’ve been slowly declining. Now, they’re sitting in the low 6s. And while that may not sound like a big deal, that change translates to real dollars.

According to data coming out of Redfin, the typical monthly payment on a $400,000 home is already down almost $400 since May.

That means if you’re buying a home now, you’re saving hundreds of dollars every month compared to what you would have been able to get earlier this spring. That’s real money that makes a real difference for buyers who paused their plans because they thought homeownership was out of reach.

And while it may be tempting to wait even longer to see bigger savings, that’s a gamble that could cost you. Here’s why.

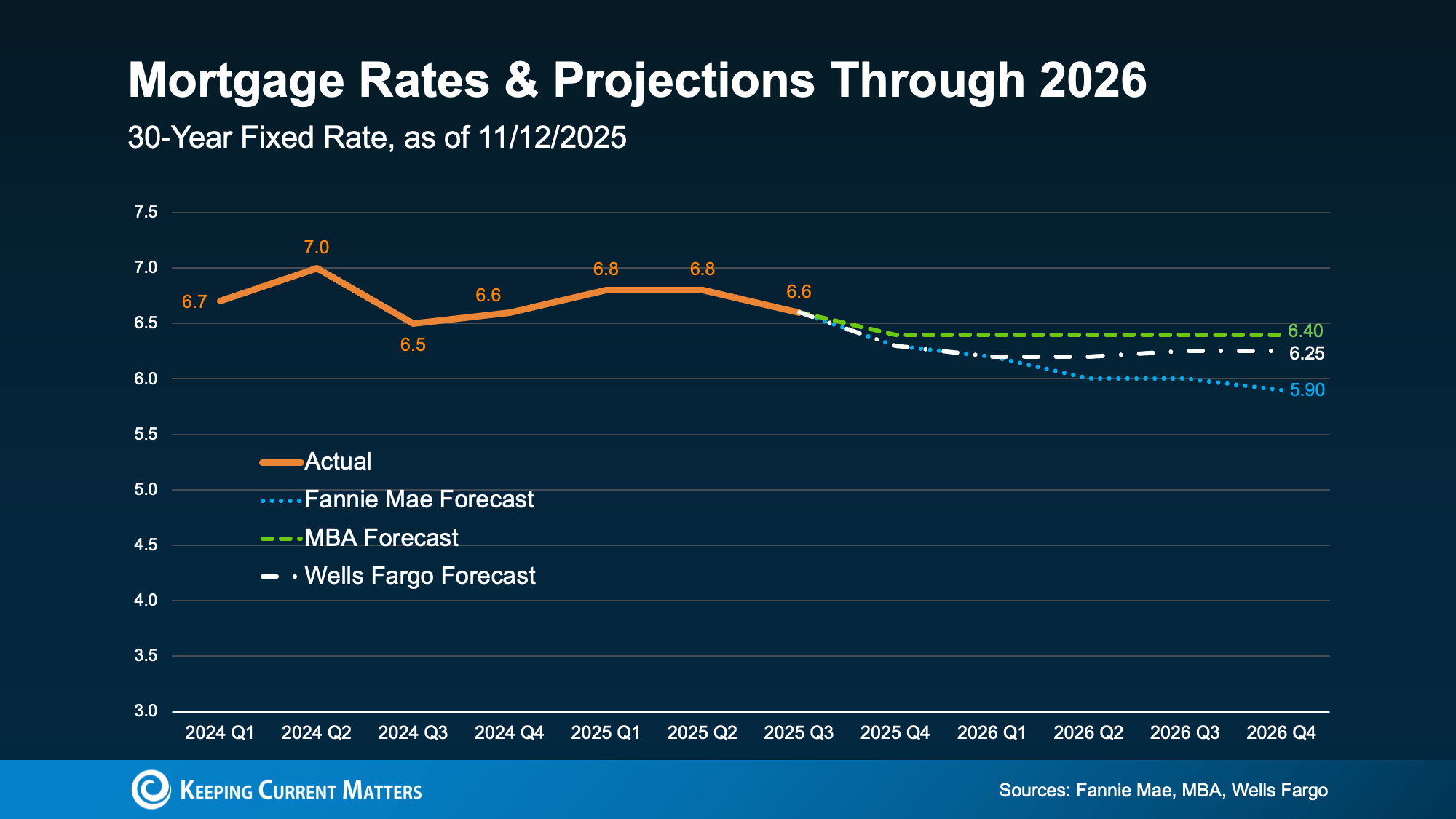

Where Experts Say Rates Are Headed

For starters, most experts say mortgage rates are likely to stay pretty much where we are today throughout 2026. So, there’s no guarantee we’ll see a rate much lower than what we have now. Only one expert forecaster is saying rates could fall into the upper 5s next year (see graph below):

And even if rates do dip below 6%, the extra savings you’re holding out for won’t move the needle as much as you might expect.

And even if rates do dip below 6%, the extra savings you’re holding out for won’t move the needle as much as you might expect.

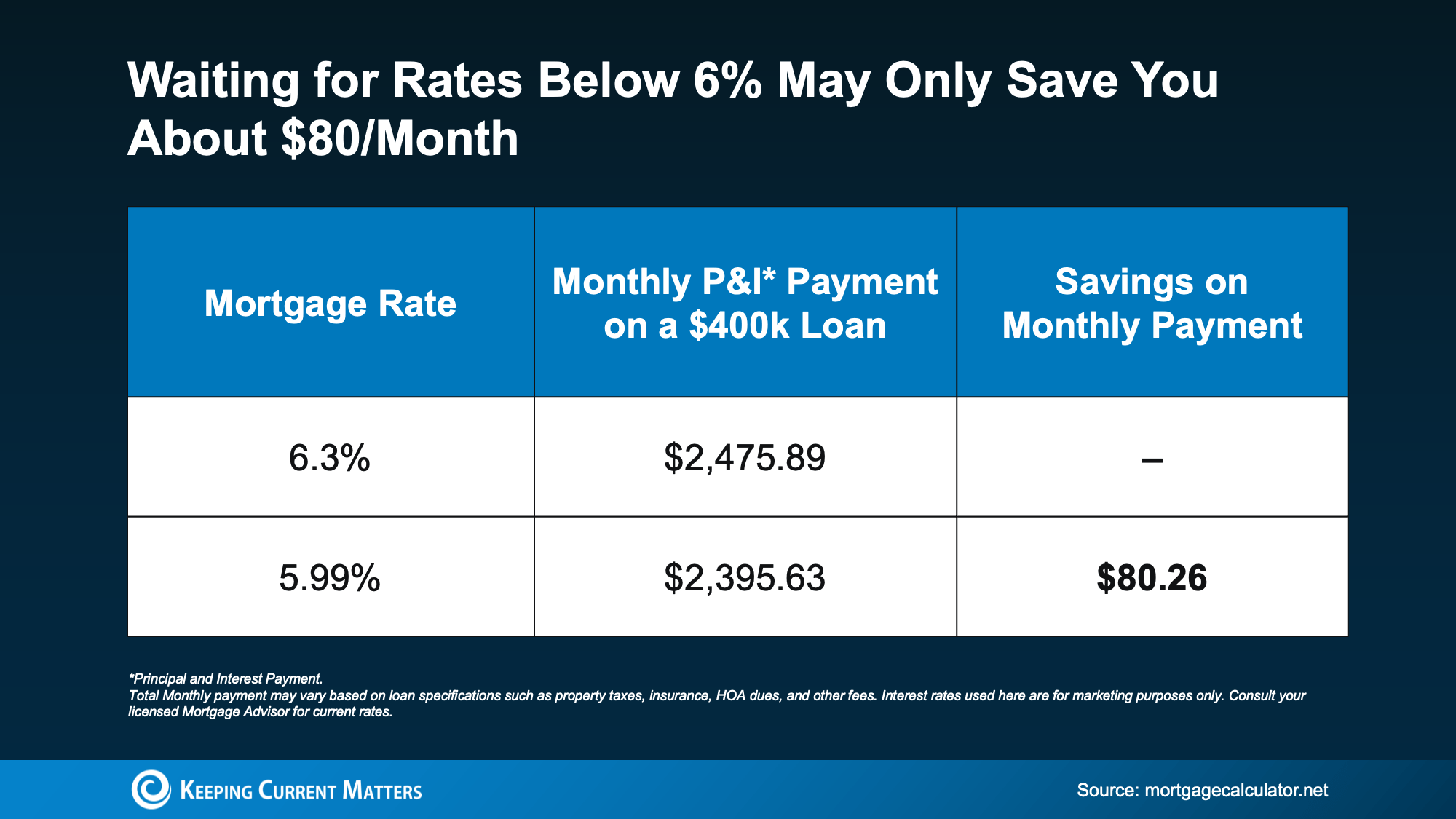

The Real Math Behind a 5.99% Rate

Let’s break it down. If rates come down to 5.99% from where they’ve been lately that’s a difference of only about $80 a month on an average priced home – give or take a bit based on your price point and the rate your lender quotes you (see chart below):

Eighty dollars. That’s it. And for the typical family, that’s about one dinner out (or one dinner in, if you have it delivered). That’s not enough to change the game for most buyers. But the savings of nearly $400 we already have compared to when you paused your search in the spring? That might be.

Eighty dollars. That’s it. And for the typical family, that’s about one dinner out (or one dinner in, if you have it delivered). That’s not enough to change the game for most buyers. But the savings of nearly $400 we already have compared to when you paused your search in the spring? That might be.

So, the question to ask yourself is this:

Is an extra $80 savings really worth the wait?

Because while you’re holding out for that small dip, the bigger opportunity might be slipping away.

When Rates Fall, Competition Follows

Right now, you have more homes to choose from, sellers who are ready to negotiate to get a deal done, and fewer buyers to compete with. But once rates fall below 6%, buyer mindsets will shift and all of that will change.

The National Association of Realtors (NAR) reports that if rates hit 6%, about 5.5 million more households will be able to afford the median-priced home. Even if only a small fraction of them decide to buy, that could mean hundreds of thousands of buyers getting back into the market.

That creates more competition for you, which would push home prices even higher – maybe high enough to cancel out the extra savings you waited for.

So, if you’re waiting for rates below 6%, just keep in mind… that extra $80 may not be worth it in the grand scheme of things.

Bottom Line

You don’t have to wait for 5.99%. You have the chance to move (and save) right now. So, ask yourself: Would you let $80 hold you back from buying a home?

If you find a home you love and the math makes sense, getting ahead may be the best strategy. Connect with an agent or lender to run your numbers. That way you can see what you’re working with in your market.