Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

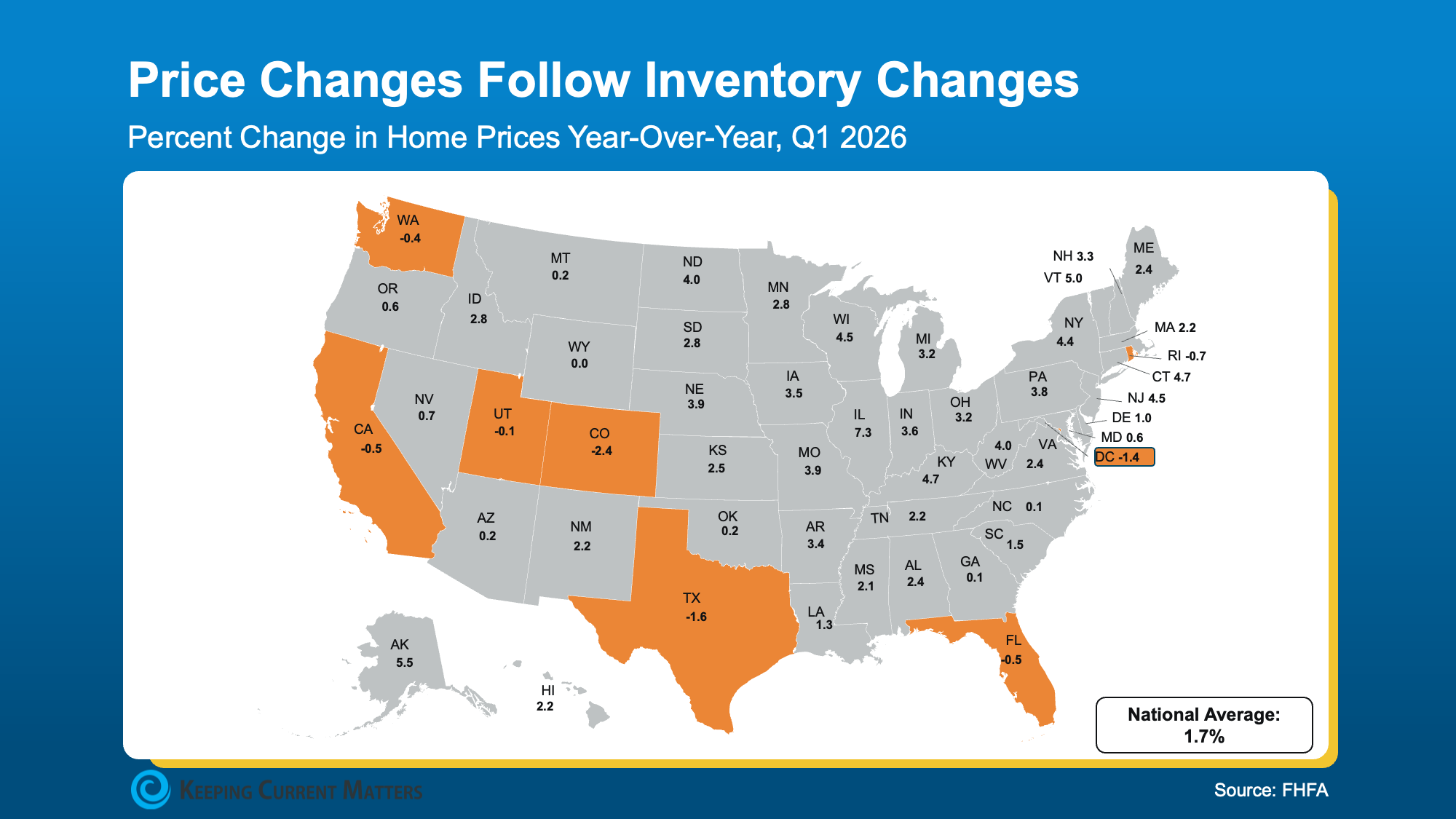

Now, let’s look at the latest Federal Housing Finance Agency (FHFA)

Now, let’s look at the latest Federal Housing Finance Agency (FHFA)

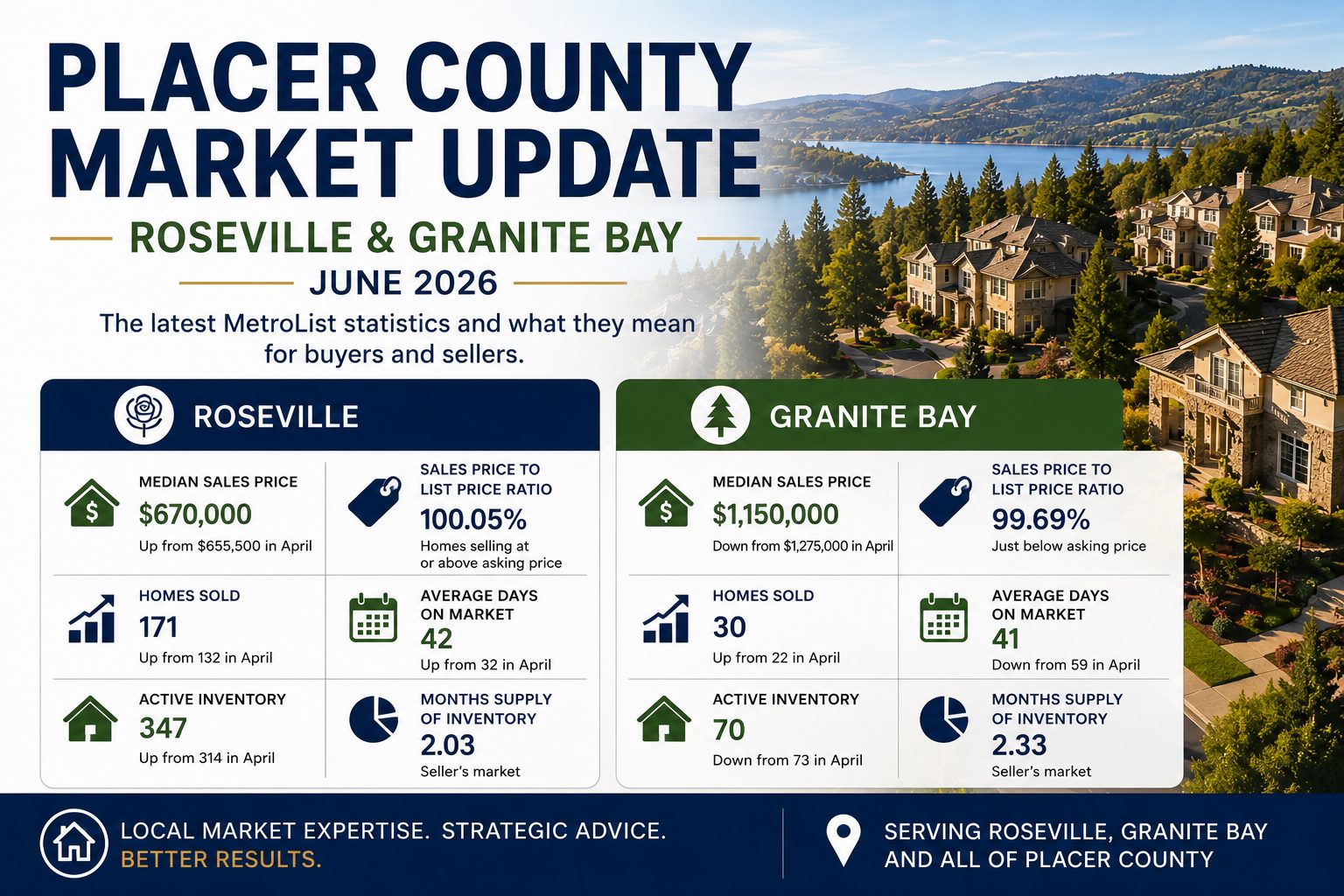

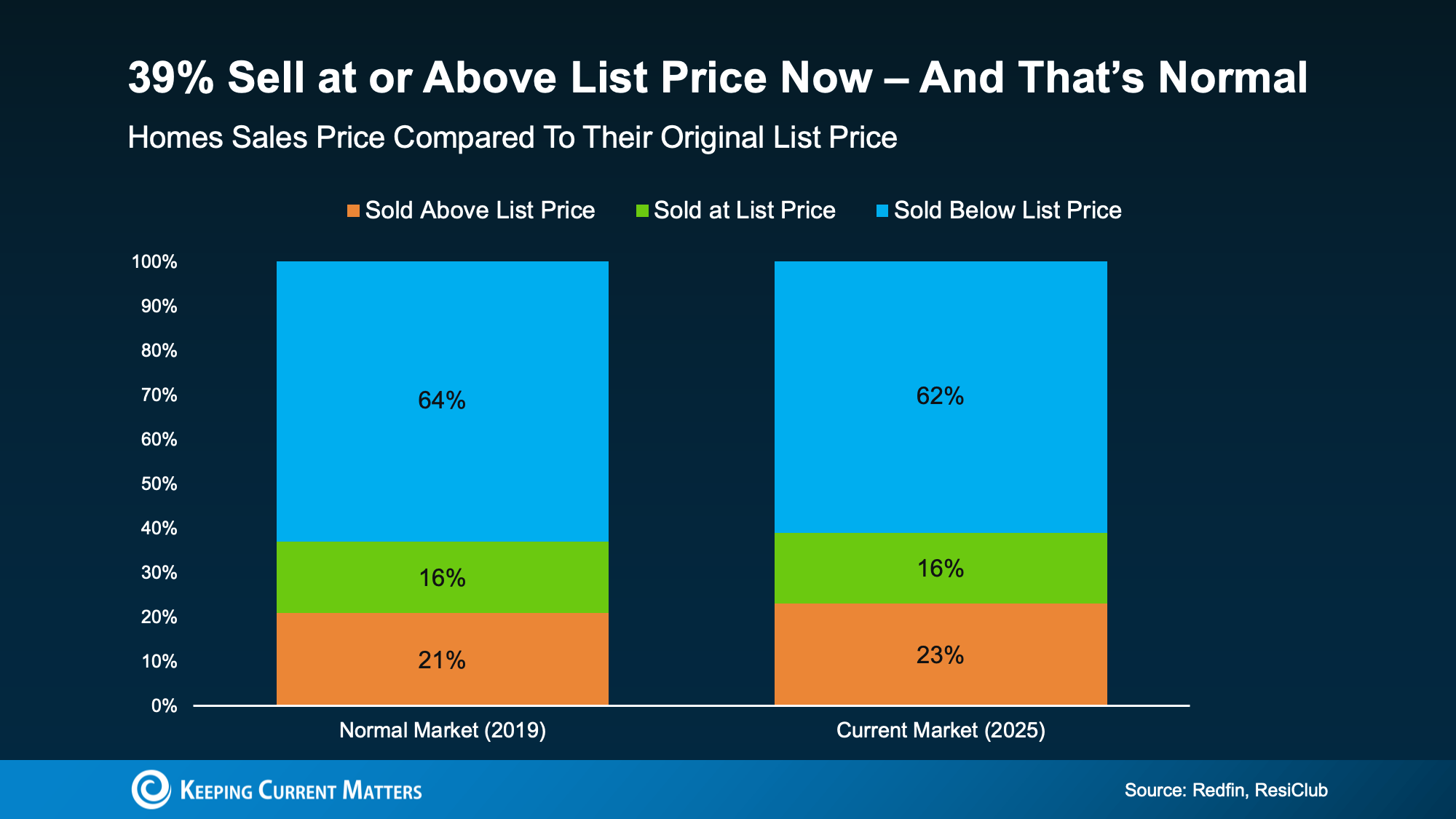

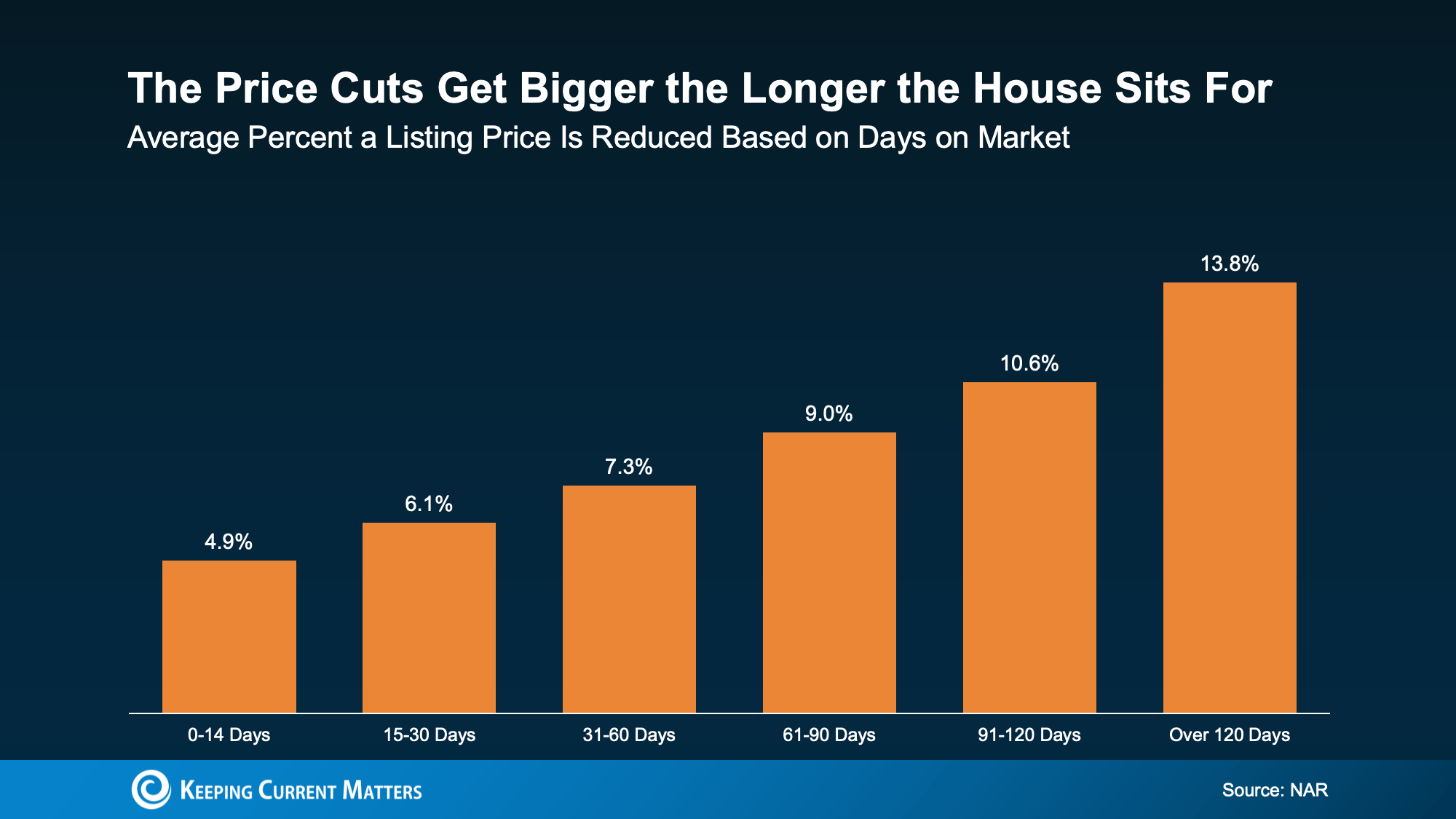

The Price Cut Trap (And How To Avoid It)

The Price Cut Trap (And How To Avoid It) So, what starts as a strategy to “leave room” for negotiate can end up costing you more in the long run.

So, what starts as a strategy to “leave room” for negotiate can end up costing you more in the long run.

Our persistent advocacy team at the National Association of REALTORS® worked to help secure tax policies that protect homeowners, expand affordability and recognize the essential role of real estate in American prosperity.

In some cases, NAR had been working for years on legislative priorities included in the final package, such as:

- A permanent extension of lower individual tax rates that were due to expire at the end of last year, adding financial stability to millions of households;

- An enhanced and permanent extension of the expiring qualified business income deduction, supporting independent contractors and small businesses;

- A five-year quadrupling of the SALT deduction cap, delivering relief to homeowners, especially in higher-tax states;

- The continued viability of business SALT deductions and 1031 like-kind exchanges, vital tools for real estate investment;

- A permanent mortgage interest deduction (MID), a key incentive for homeownership.

As homeowners filed their taxes this year, many learned that there are new rules regarding state and local tax deductions. NAR played an important role in increasing the limit on state and local taxes from $10,000 to $40,000, which can provide big relief to families who own a home. For tax years 2026 through 2029, the SALT deduction limit and income threshold increase by 1% annually. So, in 2026 the limit is $40,400 and the income threshold is $505,000; in 2027 the limit is $40,804 and the income threshold is $510,050, and so on.

Additionally, our team successfully advocated for preserving the full mortgage interest deduction in the tax reform package. The MID allows qualifying taxpayers to deduct the interest paid on a home mortgage loan from their taxable income. Our 2025 research found that 91% of voters supported protecting the MID. This effectively reduces the amount of income subject to federal taxes, often resulting in meaningful savings.

Our research last year also found that:

- 61% support increasing or eliminating SALT deduction limits;

- 86% support lower individual income tax rates;

- 83% support the 20% deduction for independent contractors and small businesses.

NAR made a strong advocacy push to ensure that small businesses, including real estate professionals and other independent contractors, can operate at a lower cost by making the 20% pass-through deduction permanent.

Throughout the process, NAR remained at the forefront of tax policy advocacy, ensuring Congress recognizes homeownership as a cornerstone of the American dream.

“We appreciate the leadership of the president, administration and Congress in advancing policies that strengthen homeownership and support the real estate economy,” says Shannon McGahn, NAR executive vice president and chief advocacy officer. “The provisions in this tax legislation highlight the value of long-standing incentives like the mortgage interest deduction and capital gains treatment, which help families build wealth and keep housing within reach.

“Should another tax bill come to fruition before the midterm election, NAR will have a seat at the table to advocate for policies that will support REALTORS® and homeowners alike,” McGahn adds. “We look forward to continuing to work with the administration and Congress to ensure the tax code supports a healthy, accessible housing market for all Americans.”