Local Appraiser, Ryan Lundquist, has recently posted his thoughts on this matter. Read on to see what he thinks about the topic of assuming a loan in today’s real estate market climate.

“Assumable loans are eye candy in today’s housing market. The idea of taking over somebody’s 2.5% loan sounds amazing, right? It’s technically possible on paper for some loan types, but it’s challenging to pull off in the real world. Yet, if mortgage rates remain high, this is something we’re likely going to hear more about, so it’s important to know the process.

IT’S RARE TO ASSUME A LOAN (FHA, VA, & USDA)

I’m not a loan officer, so I won’t step out of bounds here, but it’s basically possible to assume an FHA, VA, or USDA loan from a current owner if the loan servicer is cooperative and everything else lines up between the buyer and seller. Conventional loans are NOT assumable, but I’ll defer to loan officers if there are rare cases where that can happen (seriously, talk to a loan officer). In short, it has to be the perfect storm of the right buyer, right seller, and right loan servicer to make an assumption happen.

UPDATED NOTE: A few people have said current FHA loans are not assumable, but everything I’m reading online from lenders and HUD directly seems to show FHA loans are assumable. My advice? Talk to a loan professional and the loan servicer. I defer to them.

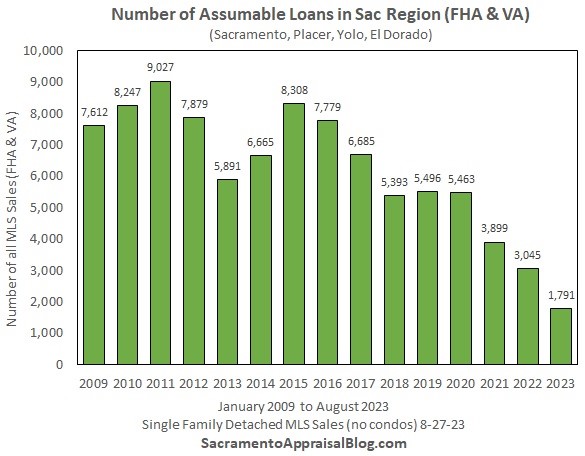

HOW MANY LOCAL LOANS CAN BE ASSUMED?

Here’s a snapshot of FHA & VA transactions since 2009 in the Sacramento region. Of course, some of these properties have sold again already, but this is a general picture of how many potential assumable loans are out there. The real prize for a buyer would be purchasing from a seller who bought during the past few years when rates were really low (though many of those owners are sitting instead of selling).

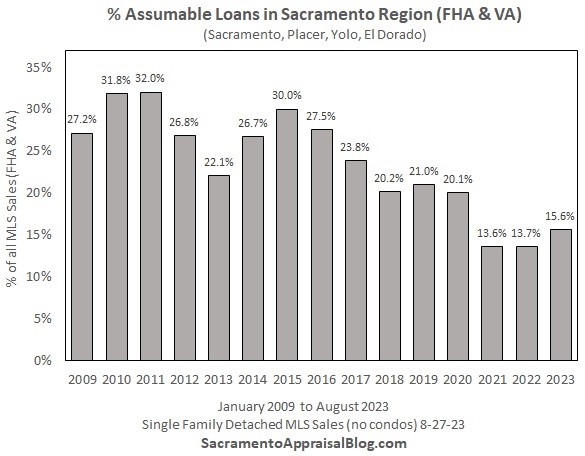

WHAT PERCENTAGE OF THE MARKET IS ASSUMABLE?

Okay, but what percentage of the market has sold in recent years with loans that could theoretically be assumed in the future? In 2020 nearly one out of every five homes sold with FHA or VA, and since then it’s been about 15% of loans.

A LOCAL LISTING EXAMPLE

Here’s a property in West Sacramento that was purchased in 2020 with FHA financing, and the listing advertises, “Seller offering a possible loan assumption at 2.75% as part of purchase price.”

BIGGEST HURDLES TO ASSUMING A LOAN:

1) Paying the difference: The buyer has to pay the difference between the loan amount and the equity the owner has. This means if a property has a $400,000 loan, but it’s worth $525,000, there is a big chunk of change for the buyer to bring to the table. Some loan officers tell me it’s possible to get a HELOC (Home Equity Line of Credit) to pay the difference, but I’ll defer to lenders on that. All that said, it seems like buyers putting 20% down are often decent candidates to assume a loan because they can absorb the difference between the loan and value in many cases.

2) It can take a long time: I mentioned loan assumptions in a Facebook thread a few days ago. I heard about one local loan assumption taking FIVE MONTHS, another taking three months, or a quick one at 30 days. Look, maybe this process can be seamless once in a while, but can you imagine being in contract for five months without a guarantee of success? That is going to take a very particular seller and buyer, right? Moreover, if there are multiple offers, the seller is unlikely to choose the buyer wanting to assume the loan. This reminds us market conditions can either foster more or less loan assumptions.

3) The loan servicer isn’t always cooperative:

There are situations where the loan servicer simply denies the loan assumption. One real estate agent told me loan assumptions are basically a buzzword because they’re difficult to pull off. Sounds about right.

THIS MARKET REQUIRES CREATIVITY:

There is no sugarcoating assuming a loan as an easy process, but I think this market requires creativity. My advice is to understand the process, advertise the idea of an assumption if the seller is on board, talk to the loan servicer prior to listing, and help educate everyone on the process. Oh, and realize this is still a unicorn event that requires the perfect storm of everything coming together. This isn’t for the faint of heart, but it will work in some situations.

CLOSING ADVICE:

My advice? Don’t put much hope in loan assumptions, but know how it all works so you can at least be aware of options. Like I said, it’s going to take the right buyer, right seller, informed real estate professionals, and a cooperative lender. When loan assumptions do happen locally, try to find out how the deal came together. The truth is buyers are starving to afford the market, and assuming a seller’s loan is going to help a small sliver of buyers out there. Ultimately, if rates remain high, this is going to be something more people are thinking about, and it’s possible we could see more loan assumptions ahead for that reason. If the market gets more competitive though, loan assumptions are the last thing sellers are going to target.

I hope this was helpful. Thanks for being here.”

Follow Ryan for more information about the Sacramento Valley Real Estate Market. He can be found across all social media platforms, as well as at his blog: https://sacramentoappraisalblog.com/

Are you among those feeling frustrated due to the limited housing options available in the current market? If so, you might be eyeing the prospect of buying a new home directly from a builder. The appeal is clear: a brand-new, tailored-to-you home without the complications of bidding wars and costly renovations. However, as enticing as it might seem, there are important factors to weigh before taking the plunge into this new home venture.

**1. The Shift Towards New Homes**

In neighborhoods where homeowners are reluctant to give up their low-interest-rate mortgages and put their homes on the market, new homes have gained popularity. Recent trends show that new-home sales account for about 15% to 20% of all home sales, and in some markets, this number could even reach 30%, according to Lawrence Yun, chief economist at the National Association of Realtors. The gap in prices between new and existing homes has been narrowing, with the median sales price of new homes sold in June 2023 at $415,400, slightly above the $410,200 for existing homes. This makes the choice between new and existing homes less financially daunting than it has been in two decades.

**2. Incentives and Customization**

Builders, buoyed by the gains made during the pandemic, are now offering buyers incentives to sweeten the deal. These incentives can range from reduced mortgage rates to covering closing costs. Additionally, brand-new homes often come with customization options, allowing you to tailor certain aspects to your preferences. For example, Hayley and Tyler Dupee found their dream home in Ladson, S.C., enticed by incentives like a smart-home security system and window blinds. This level of personalization can be a deciding factor for many buyers.

**3. Consideration for Upgrades**

While moving into an existing home might seem faster, it’s crucial to weigh the potential expensive repairs and upgrades you could face. New homes often come with a higher price tag and the possibility of move-in delays due to construction timelines. However, this delay might be worth it for the added customization and potential future resale value. When considering upgrades, focus on essential systems like plumbing and electrical, as well as high-return areas such as the kitchen. Small choices, like opting for a slightly smaller kitchen cabinet, can add up to substantial savings without compromising quality.

**4. Making Informed Choices**

Navigating the world of new home construction requires careful reading and understanding of contracts. Builders often have the flexibility to substitute materials if needed, so be sure to read the fine print and understand where you have a say. Don’t assume that everything in the model home is included – ask about the appliances and finishes that come with your home. It’s also important to have extra funds set aside, as builders may adjust prices based on material costs. A contingency budget of around 10% to 15% is advisable.

**5. Preparing for Imperfections**

Despite the allure of a brand-new home, it’s wise not to expect perfection. While many new homes come with warranties that cover various issues, it’s crucial to conduct inspections at multiple stages of the building process. Pre-drywall inspections can catch problems that might not be apparent after the home is finished. Consider hiring an independent inspector to thoroughly assess the property. Investing between $280 and $400 for inspections can save you from dealing with issues like humidity, improperly installed features, or structural defects down the line.

Let’s work together to turn your dream of a new home into a reality. Reach out to me before your next visit to a new home builder, and let’s embark on this exciting journey with confidence. Your ideal new home is just around the corner, and I’m here to help you find it.

Are you on the hunt for your dream home? The real estate landscape is evolving, and it seems like today’s buyers have a clear preference – they’re looking for homes that are move-in ready. I’m going to dive into the latest trends in the housing market, exploring why more and more buyers are leaning towards fully renovated properties rather than tackling major renovation projects. Let’s break it down:

**1. Buyers’ New Mindset: Turnkey Over Renovation**

Picture this: you’re eager to buy a house, but the thought of hiring a contractor and dealing with additional costs and headaches makes you think twice. Well, you’re not alone. Real estate agents have noticed a shift in buyer preferences. Many buyers are now prioritizing homes that don’t require major renovations. They want to move in without the stress of fixing up the place.

**2. The Numbers Game: Offers and Sales**

Numbers never lie. A year ago, sellers were receiving around six offers on average. But now, that number has dropped to about three offers. Why the change? Well, one major factor is the rise in mortgage rates. High mortgage rates are making buyers cautious about investing in homes that need renovations.

**3. The Cost Equation: Rates and Property Prices**

Let’s talk dollars and cents. Renovations have always been a bit of a gamble. But now, they’re becoming even costlier. Home loan and construction loan rates have increased, adding to the high property prices. This combination is creating a wider gap in how quickly renovated and non-renovated homes sell.

**4. Slow and Steady: The Market Impact**

Properties in need of repair are spending more time on the market. This means sellers who want a quick sale might need to invest in some improvements before listing their homes. Buyers are becoming pickier, and homes that need upgrades are taking longer to sell.

**5. The Desire for Simplicity: Renovation Appetite Decreases**

Whether it’s a main property or a second home, buyers are less interested in renovation projects. Take Tommy Byrd, for example. He’s looking for a vacation house but prefers one that’s already renovated. Managing renovations from another state isn’t something he’s excited about.

**6. Picky Buyers: More Choices for Upgrades**

Buyers have more power to choose. If a home needs upgrades like new floors, kitchens, bathrooms, or a fresh coat of paint, buyers can afford to be choosy. They’re not as willing to overlook these details as they might have been in the past.

**7. The Changing Market Landscape**

Market dynamics are shifting. Homes are staying on the market longer, signaling that they might be overpriced or in need of significant repairs. Most buyers simply can’t afford major renovations right now, given the current economic climate. (If you are in this boat, let’s talk.. I have an amazing suggestion to get you the repairs/upgrades your home needs to get it sold for a higher price!)

**8. The Remodeling Market Booms**

Interestingly, the desire for move-in ready homes hasn’t put a damper on the remodeling market. Home improvement and repair projects are on the rise, projected to hit $484 billion in 2023. Existing homeowners are keen on upgrading without giving up their low mortgage rates.

**9. Market Variances: The Bid Wars and Scarcity**

Different markets have different stories to tell. In some areas, there are so few homes for sale that buyers might have to settle for a fixer-upper. In other regions, bidding wars are still happening, and unrenovated homes can fetch top dollar – it just might take a bit longer.

The real estate landscape is changing, and buyers are steering towards turnkey properties that spare them from major renovations. From rising mortgage rates to a desire for simplicity, these factors are shaping the way people view their future homes. Whether you’re planning to buy or sell, understanding these trends can make all the difference in your real estate journey. Let me help you navigate this market whether you are looking to buy or sell. I am here to assist you in making your real estate dreams come true.

Thinking about buying a home can be tough right now. Some people want to wait for lower interest rates, but here’s the problem – if you wait too long, home prices might go up. That’s where Barbara Corcoran, a real estate expert and “Shark Tank” star, comes in. She recently shared her thoughts on what’s coming up in the housing market.

What Barbara Corcoran Thinks: What You Need to Know

The housing market is facing a tricky situation, which Corcoran calls a “bottleneck.” This means sellers are worried about higher interest rates, so they’re not moving. On the other side, buyers are being careful because they think they’re not getting enough value for their money. “Sellers don’t want to move from their apartment or their home because they don’t want to take on higher interest rates,” she said, “and buyers are too afraid [to buy] because they are getting less house [for the price]. So you’ve got a standoff going on. But things are changing.”

Corcoran believes there will be a major swing in the real estate market as soon as interest rates drop.

“The minute those interest rates come down, all hell’s going to break loose and the prices are going to go through the roof,” she said. “[Right now sellers are] staying put. But they’re not going to stay put if interest rates go down by two points.

“It’s going to be a signal for everybody to come back out and buy like crazy, and the house prices [will likely] go up by 20%,” she said. “We could have COVID [market] all over again.”

Different Places, Different Prices

Corcoran also talks about how home prices are changing in different parts of the country. A recent report said that home prices dropped for the first time in 11 years. But it’s not the same everywhere. In places near the coast, prices are going down because homes are really expensive. But in the Southwest, prices are actually going up. Some cities there saw prices go up by a lot – around 20% – in just half a year. Then there’s South Florida, where prices are still going up. Corcoran says this is because people really like Florida and are willing to pay more.

No Big Crash Coming

Corcoran is pretty sure that we won’t have a big crash like we did in 2008. Back then, things went bad because of problems with mortgages. But this time, people are being smarter with their money and not borrowing too much. So, even though the market might be uncertain, Corcoran doesn’t think it’ll be as bad as before. “People [have] their hard-earned cash in the market — people aren’t overleveraged,” she said. “There’s really no comparison to now compared to what came before.”

Homes vs. Businesses

Corcoran also looks at homes and commercial buildings (like offices) as two separate things. She says that just because one is doing well doesn’t mean the other is. Right now, homes are doing okay, but commercial spaces are struggling. Many people don’t want to buy commercial properties because they’re not sure if they’ll make money. This might take a long time to get better.

Bold Prediction: Home Prices Going Up

Corcoran stands by her idea that home prices won’t go down. She even thinks they could go up by 15% when interest rates on loans go down. She’s feeling positive because there aren’t many homes for sale, loan rates are low, and lots of people want to buy.

As things keep changing in the real estate world, Barbara Corcoran’s ideas can help both buyers and sellers. Her experience helps us understand how the market works and what we can expect.

In 2023, the housing market is undergoing a peculiar phenomenon — a reverse crash. The rise in mortgage rates, surprisingly, hasn’t instigated a significant decrease in home prices. This perplexing trend can be attributed to a complex interplay of economic, demographic, and market determinants.

Today, a significant proportion of homeowners — 92% of those with mortgages — enjoy rates below 6%, with a lucky 62% relishing rates under 4%. As mortgage rates climb, these homeowners are opting to hold onto their properties, rather than sell and risk locking in a higher mortgage rate.

Consequently, this shift in homeowner behavior has reduced the volume of home sales. This is corroborated by a recent study, revealing that approximately 27% of homeowners would be motivated to sell if rates descend to 5% or lower.

Furthermore, nearly half of the homeowners surveyed would consider listing their properties if rates were to plunge to 4%.

Despite these evolving dynamics, home prices have seen only a nominal drop. The manager of the S&P Case Shiller Index predicted a peak-to-trough decline of around 5%, leaving 2% yet to be recuperated.

This forecast is supported by Goldman Sachs, who foresee a 2.2% dip in 2023 and do not anticipate any substantial recovery until interest rates start their downward journey.

In contrast, Fannie Mae, the mortgage giant, revised their outlook last week, projecting a 1.2% deflation in national home prices in 2023, which is predicted to be followed by an extra 2.2% contraction in 2024.

However, Zillow challenges this prediction, suggesting that 2023 will wrap up with home prices 5% greater than their starting point.

This projection was revised upwards from their original forecast of a 3.9% increment, thanks to the rapid pace of sales — a staggering 15% decrease in pending home sales implies a faster rate of purchase than listing.

Analysts have identified five crucial elements contributing to the unexpected tenacity of housing prices:

Limited Inventory: The enticingly low interest rates have convinced many homeowners to retain their properties unless selling becomes indispensable.

Construction Lag: Challenges like regulatory hurdles, disrupted supply chains, and heightened costs are stifling builders from catching up with the soaring demand.

New Buyer Demographics: Millennials, representing 43% of the housing market, are influencing the market with their specific preferences – affordability, roomier homes, opportunities for DIY renovations, and cost-effective locations, according to BankRate.

Banks’ Conservative Lending: If financial institutions decide to relax their lending standards, a surge of buyers could push home values even higher.

Scarcity of Foreclosures: Presently, foreclosure is usually an option only when a homeowner’s debt surpasses the home’s value, which is currently not a widespread issue.

These forces, collectively, are driving the peculiar ‘reverse crash’ of the 2023 housing market. Rather than witnessing the conventional collapse in home values, we’re experiencing an intriguing resilience in prices. As we continue to observe these trends, the longevity and broader implications of this housing market anomaly remain to be seen.

The pandemic led to a shift away from expensive cities as people sought financial relief in more affordable suburbs. However, this migration trend has seen a reversal. Many individuals who moved for cost savings have returned after realizing that cheaper living comes with its own challenges.

Economic Opportunity vs. Affordable Living: While relocating to save on living costs seems appealing, the economic trade-off is complex. Moving to a cheaper city often means fewer opportunities for financial growth due to limited economic diversity. Economic diversity fosters various industries and a thriving job market, impacting long-term career prospects.

Potential Price Escalation in Emerging Cities: Some budget-friendly cities offer a high quality of life and strong economies. However, their popularity can lead to rising costs. What starts as a financial win may not remain consistently affordable as a city’s cost of living evolves.

Fluctuations in Property Values: Choosing a cheaper city may result in slower property value appreciation. Property values in these areas might not increase as much over time compared to pricier urban centers, affecting long-term investments.

Considerations with Low Taxes: Lower taxes in cheaper cities often mean fewer services. It’s important to evaluate the impact of property taxes and the quality of services, especially for families. Limited educational resources can impact children’s academic development.

Healthcare Considerations: Cheaper cities might offer limited healthcare options and lower-quality medical facilities. Access to quality healthcare should be a priority, particularly for those with significant healthcare needs.

Balancing Culture and Quality of Life: Relocating might mean sacrificing access to cultural events and entertainment enjoyed in pricier cities. A lack of diverse amenities can impact overall satisfaction and make forming new social networks challenging.

The Importance of Social Networks: Moving to a cheaper city often involves leaving behind established relationships. Social connections contribute to well-being, and rebuilding these networks can be difficult in a new location.

Relocating to a cheaper city offers potential cost savings, but it’s essential to consider the broader implications. As a real estate agent, I’m here to help you navigate these considerations and make an informed decision that aligns with your long-term goals. Contact mefor expert guidance in your relocation journey.

In the world of mortgages, misconceptions abound, but it’s essential to separate fact from fiction. Here are some common mortgage myths debunked:

Myth #1: A 20% Down Payment is Mandatory

While the 20% down payment rule is widely known, it’s not an absolute requirement for buying a home. While making a larger down payment can have advantages, like lower monthly payments and interest rates, there are many programs available for first-time homebuyers that allow for smaller or even no down payment. Options like FHA loans, USDA loans, and VA loans cater to various financial situations. Additionally, you can always refinance later to secure better rates and terms.

Myth #2: Perfect Credit is a Must for Mortgage Approval

Credit score is crucial, but it’s not the sole factor lenders consider when approving a mortgage application. Lenders also assess your debt-to-income ratio, employment history, and income. A lower credit score may not necessarily disqualify you if the rest of your application is strong. Some lenders even offer programs for borrowers with credit scores as low as 500. Just be aware that a lower credit score may result in a higher interest rate.

Myth #3: Renting is Always Cheaper than Buying

Renting might seem cheaper in the short term, depending on the housing market. However, homeownership often proves to be a more sound financial decision in the long run. With each mortgage payment, you build equity in your home, which can be used later for various expenses or as a source of profit when you sell the property. Unlike renting, where your money goes to the landlord with no return on investment, homeownership offers numerous benefits, including potential tax advantages and a hedge against rising rents.

Myth #4: The Lowest Interest Rate is Always the Best

While a favorable interest rate is vital, it’s not the sole factor to consider when choosing a mortgage. There are other costs to consider, such as closing costs, property taxes, homeowners insurance, maintenance expenses, and possibly private mortgage insurance (PMI). Take all these costs into account to determine the overall affordability of the mortgage.

Myth #5: Adjustable-Rate Mortgages (ARMs) are Always Risky

Fixed-rate mortgages are popular for their stability and predictability. However, that doesn’t mean adjustable-rate mortgages (ARMs) should be dismissed outright. ARMs can offer lower interest rates during the initial years, making them a viable option for those planning to sell or relocate in the near future or expecting an increase in income. The decision to opt for an ARM should be based on individual circumstances, risk tolerance, and future plans.

In conclusion, navigating the world of mortgages can be overwhelming, especially with so many myths circulating. By educating yourself and dispelling common misconceptions, you can confidently explore your mortgage options and find the one that best suits your needs.

Are you on the verge of closing on your dream home? It’s crucial to be mindful of certain financial decisions that could potentially jeopardize the closing process or even prevent you from obtaining a mortgage altogether. To ensure a smooth closing, here are five common mistakes you should steer clear of:

1. Refrain from Major Purchases

As you approach the closing date, avoid making significant purchases like a new car, boat, or any other expensive item. Even purchasing furniture or appliances on installment plans is best postponed until after your mortgage is finalized. Such transactions may impact your credit score and history, potentially leading to higher interest rates or requiring a larger down payment. Delaying major purchases until the closing is complete will safeguard your qualification for the loan.

2. Be Cautious with New Credit

Opening a new credit card or closing an existing one can also affect your credit score. During the lead-up to the mortgage closing, lenders meticulously assess the credit risk for each applicant. Any changes to your credit score during this critical period could work against you and might even impede the loan finalization. Be especially cautious if you’re on the borderline of qualifying for a mortgage due to a low credit score.

3. Steer Clear of Job Changes

Changing jobs just before closing on your new home is a mistake you should avoid. Mortgage lenders scrutinize employment history for consistency, and making job switches can delay the closing process. If possible, hold off on any job changes until after the closing to ensure a smoother transaction.

4. Respect the Timeline

Closing on a mortgage is time-sensitive, even if you’ve locked in your rate. It’s essential to stay organized and ensure all required paperwork is submitted on time. Failure to do so could lead to the loss of your agreed-upon terms, necessitating the restarting of the entire process.

5. Think Twice about Personal Loans

Obtaining a personal loan or co-signing for someone else’s loan can present challenges before reaching the closing table. Lenders take into account your debt-to-income (DTI) ratio, a crucial factor in mortgage approvals. Depending on the loan amount and how it affects your DTI, lenders may reject your loan application, even if you were preapproved. A hard inquiry resulting from applying for a personal loan could also impact your credit score, potentially making you ineligible for the mortgage.

By avoiding these five common mistakes, you can safeguard a successful mortgage closing and move into your new home with peace of mind. Remember, being financially responsible during this crucial time is key to securing your dream home and the loan you need.

At least three people in Jose Medina’s Sacramento neighborhood have moved there from the Bay Area in recent years. And those are just the ones he knows of. Medina, too, is a transplant — and since relocating from Oakland in 2021, he said he’s had an additional seven friends move to the city or its surrounding areas.

The Bay Area exodus may be mostly a myth, but the trend of people moving inland, leaving coastal metros in search of more space at better prices, is growing. There are more people moving to Sacramento from the Bay Area than anywhere else in the country, according to Redfin data. People moving from the Bay Area to Sacramento isn’t a new phenomenon, but COVID-19 sped up a process that experts say was inevitable, and it could have long-lasting effects on the state.

In 2020 alone, migration between San Francisco County and Sacramento County grew 70% from the previous year, a CBRE report concluded. The Sacramento region is projected to grow another 4% in the next 5 years, largely buoyed by this continued migration.

A home in the ‘city of trees’

Medina and his girlfriend were living in a one-bedroom condo in Oakland when the city shut down, forcing them to start working from home. They quickly realized they needed a larger home if they would be working remotely for the foreseeable future. “We started looking in the East Bay for spots and were met with everybody trying to do the same thing we were doing,” he said. “It was a very competitive market and everything was going well over asking — sometimes 50% over.”

A friend who had just moved to Sacramento invited them to visit and take a break from the hunt. “We quickly fell in love with Sacramento,” he said. “The culture, the city of trees, it is exactly what it is. It’s a town, but a city at the same time.”

While Medina said the real estate market still felt competitive, it wasn’t nearly as ruthless as it had been in the Bay Area. The couple soon put an offer in on a new-construction home. He said they now have “way more space than we ever imagined.” They’re both still working remotely for tech companies, happy they moved and planning to stay in Sacramento for the long haul.

Creating a ‘megaregion’

They’re far from the only ones who have made the move, and all the new transplants are having a significant impact on Sacramento’s population, which grew 26% between 2000 and 2019, according to census data. The Bay Area’s grew just 14.6% during the same period. A recent study conducted through a collaboration between the University of Southern California, Occidental College, and UC Davis suggests increased migration could even be creating a “megaregion,” breaking down barriers that traditionally separated the coastal cities of the Bay Area from the inland region around Sacramento.

The “megaregion” and the resulting demographic shifts will have an outsized impact on traffic and infrastructure, creating new needs for California’s future. While the study showed there was a small dip in the proportion of people commuting to the Bay Area from Sacramento County, the percentage of people “supercommuting” — defined as a commute of more than 50 miles — had grown from 17% in 2008 to 20% in 2018. That percentage grew in every Central Valley county studied and is likely to continue as high-wage earners with jobs centered in the coastal metros seek larger homes inland.

Seva Rodnyansky, a research specialist on the project, said if this increased migration continues, it could present problems for state agencies, which will be forced to work together to provide the necessary infrastructure. “The more seats at the table, the harder it is to deal with specific concerns,” he said.

The issues are not limited to Sacramento and the surrounding suburbs, according to Rodnyansky, and his research suggests the megaregion could stretch all the way to Fresno. Past Sacramento, people are also spreading out to surrounding El Dorado and Amador counties, where they will likely face challenges they’re not prepared for, like managing their land for increasing wildfire risk.

The trickle-down effect

There’s also the trickle-down effect of rising housing costs. Demand for housing far surpasses supply, both near Sacramento and in outlying areas, where decades of home-building shortfalls have compounded while the job market has remained concentrated in the city centers.

The Sacramento median home price is $475,000, according to Redfin, up 38% from 2019. The average San Francisco home sells for nearly triple that. The average home in Placerville jumped 27% since 2019.

Even if you’re on a budget, make sure to purchase specialty boxes. Just one wardrobe box per bedroom will help tremendously. Your clothes will not arrive at your new home wrinkled and you won’t have to worry about packing your hangers.

TV and art boxes are also worth the cost. Don’t chance your expensive art or electronics getting damaged.

Other boxes can be found at your local grocery store. We recommend the produce boxes. You can also find deals on Craigslist and Freecycle.

2 – Allow Enough Time

As a rule, allocate one day of packing per room. Double that if you have a lot of belongings or unusual sized things to pack.

Budget 3-5 full days to pack a three-bedroom home. A studio should take 1-2 days. A one-bedroom should take 2-3 days and plan on 5-8 days for a five-bedroom. Of course, it will take less time if you have help!

3 – Color Code The Boxes

Instead of writing room names on your boxes, color code them! This will keep you from having to direct your helpers all day long, freeing you up to do other things.

Our Moving Game Plans ELITE and Downsizing Magic offer unique visual systems that organizes and simplifies the packing, unloading, and unpacking process, saving you and your move team hours (if not days) of precious time.

4 – Pack One Room at a Time

Wandering from one room to another will waste your precious time so begin with the least used room and complete it before moving to the next. This will help you stay organized and focused AND you’ll feel a great sense of accomplishment when it is done!

Your least used room could be your guest bedroom, the attic, garage, or storage closets.

Note: Make sure to put the heavier items on the bottom and don’t leave any extra space in the boxes.

5 – Room by Room Tips

For detailed recommendations, visit our BLOG for these nifty packing tips:

1.

Kitchen

2.

Dining Room

3.

Bathrooms

4.

Garage & Outdoor Furniture

5.

Bedrooms

6.

Living Room & Office

6 – Things to set aside

Create an Essentials Box. This is the first box you will open, and it should have what you need for your first night and morning in your new home. It should have medications, snacks, toilet paper, paper towels, phone chargers, coffee, and a set of clothes. Make sure to include a first aid kit too!

If you have small children and pets, consider packing their own essentials bag.

7 – Develop a Moving Timeline

Having a calendar is very helpful. It’ll help reduce your stress and keep you motivated. You’ll feel less rushed knowing that you are on task.

Break big rooms and projects into small, easy to accomplish tasks. It will keep your spirits up knowing you are accomplishing things!

Stick to the schedule and you’ll have everything ready when the moving truck arrives!

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Even if you’re on a budget, make sure to purchase specialty boxes. Just one wardrobe box per bedroom will help tremendously. Your clothes will not arrive at your new home wrinkled and you won’t have to worry about packing your hangers.

Even if you’re on a budget, make sure to purchase specialty boxes. Just one wardrobe box per bedroom will help tremendously. Your clothes will not arrive at your new home wrinkled and you won’t have to worry about packing your hangers. 2 – Allow Enough Time

2 – Allow Enough Time

5 – Room by Room Tips

5 – Room by Room Tips