Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Five Ways NOT to Use Your HELOC

One of the benefits of owning a home is the chance to build equity. Equity is the difference between what you owe on your mortgage and what your home is worth. If your home is worth $300,000 and you owe $100,000 on your mortgage, you have $200,000 of equity.

You can then borrow against that equity in the form of a home equity loan, or HELOC. A HELOC is a bit like a credit card with your home’s equity serving as your credit limit. Say you have $200,000 of equity. You might qualify for a HELOC of $150,000. You can then borrow up to that limit to spend the funds on whatever you want. And you only pay back what you borrow.

Say you need to spend $50,000 on a major kitchen renovation. You can borrow that $50,000 from your HELOC. You’ll then pay back what you borrowed in regular monthly payments, with interest.

HELOCs tend to come with lower interest rates than credit card s or personal loans do, which makes them a more affordable option when financing home repairs or renovations.

s or personal loans do, which makes them a more affordable option when financing home repairs or renovations.

Using your HELOC to fund improvements that will increase the value of your home is the best use of your HELOC dollars. You’ll even gain a tax benefit: You can write off the interest you pay on your HELOC if you use the funds for renovations or improvements that boost the value of your home.

What should NOT be financed with a HELOC

A dream vacation: You might want to fly to Europe or take that Alaskan cruise. But save up money to pay for it; don’t use your HELOC to fund it. If you fall behind on your HELOC payments, your lender can foreclose on you, eventually evicting you from your home and taking possession of it. Taking that risk to fund a vacation isn’t worth it.

Your or your children’s college education: Because the interest rates with HELOCs can be lower than what you’d get with private student loans, you might consider funding all or part of your or your children’s college tuition with a HELOC. Again, this is risky. If you stop making student loan payments, your credit score will tumble. But your lenders can’t take possession of your home. The same can’t be said if you stop making payments on a HELOC.

A big wedding: We get it: Weddings can be expensive. But again, funding a wedding — yours or one of your children’s — with a HELOC can put your home at risk. It’s not worth it for what is essentially a one-day event.

Stock market investments: You can make a lot of money by investing in the stock market. You can lose a lot, too. And if you use your HELOC to pay for your stock market investments? You might even lose your home if you fall behind on your payments. Again, the potential gain isn’t worth the risk. If you want to invest in the stock market, use your own funds that you’ve saved.

Credit card debt: This is a little trickier. Credit card debt comes with sky-high interest rates. It might make financial sense, then, to use a HELOC to pay off your credit card debt, as the interest rate attached to the money you’ve borrowed against your HELOC will be far lower. Again, though, there is risk. If you’re worried that you won’t be able to afford your HELOC payments, don’t borrow against your line of credit to pay off your credit card debt. Your credit card provider can’t foreclose on your home if you fall behind on your payments.

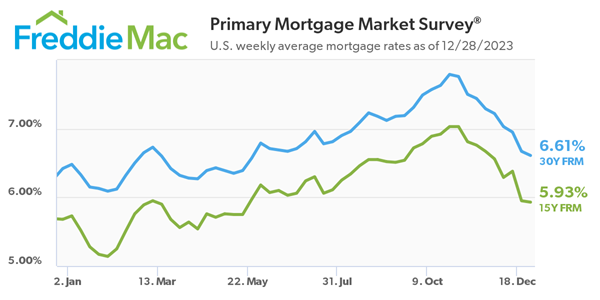

Heading into the New Year, Mortgage Rates Remain on a Downward Trend

Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®), showing the 30-year fixed-rate mortgage (FRM) averaged 6.61 percent.

“The rapid descent of mortgage rates over the last two months stabilized a bit this week, but rates continue to trend down,” said Sam Khater, Freddie Mac’s Chief Economist. “Heading into the new year, the economy remains on firm ground with solid growth, a tight labor market, decelerating inflation, and a nascent rebound in the housing market.”

News Facts

- The 30-year FRM averaged 6.61 percent as of December 28, 2023, down from last week when it averaged 6.67 percent. A year ago at this time, the 30-year FRM averaged 6.42 percent.

- The 15-year FRM averaged 5.93 percent, down from last week when it averaged 5.95 percent. A year ago at this time, the 15-year FRM averaged 5.68 percent.

The PMMS® is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20 percent down and have excellent credit. For more information, view our Frequently Asked Questions.

Freddie Mac’s mission is to make home possible for families across the nation. We promote liquidity, stability, affordability and equity in the housing market throughout all economic cycles. Since 1970, we have helped tens of millions of families buy, rent or keep their home.

Home sales are expected to soar in these California cities next year

With mortgage rates finally easing, many California cities are expected to see home sales rebound significantly next year, according to a new forecast from Realtor.com.

Five metro areas are predicted to see double-digit, year-over-year sales growth in 2024.

They are Oxnard-Thousand Oaks (18%), Riverside-San Bernardino-Ontario (13.8%), Bakersfield (13.4%), San Diego-Chula Vista-Carlsbad (11%) and Sacramento (10.3%).

Home sales in the Los Angeles-Long Beach area are predicted to climb 9.2% after seeing declining sales for two years, analysts at Realtor are forecasting.

The online real estate listing service, which is certainly hoping for a turnaround, ranked the top 100 metro areas on two factors: expected single-family home sales growth and anticipated growth in median home prices.

In all six of those California markets, prices are expected to climb to more than 40% of the 2017-19 average, according to Realtor.

“Among California metros, an interesting split emerges. Five California metros entered our top 10 list of housing markets but none were Bay Area or Northern Californian metros,” Realtor notes in its report.

In 2024, Realtor’s analysts are expecting sales to decline in San Jose-Sunnyvale-Santa Clara by 18.5%, six-percent in Fresno, and be largely flat in the San Francisco-Oakland-Berkeley area.

Realtor also points out that California’s top markets tend to be more sensitive to mortgage rates than many other parts of the nation because less than a third of “homeowners” actually own their homes outright and, instead, owe money to a bank or lender.

Oxnard has the lowest share of homeowners who own their homes outright among the top 10 markets at 30.0%, followed by San Diego at 30.5% and Riverside at 38.4%.

by: Marc Sternfield

Private Mortgage Insurance: Is It as Bad as You Think?

Private mortgage insurance, better known as PMI, provides a type of financial safety net to your lender if you should stop paying your mortgage on time. How much you pay will vary, but PMI typically costs 0.1% to 2% of your loan amount.

That can add up. If you are taking out a mortgage of $300,000 and your PMI runs 1% a year, you’ll spend $3,000 a year on PMI. That comes out to $250 a month.

How to avoid PMI

You don’t always have to pay for PMI. Your lender won’t charge you for this insurance if you come up with a down payment equal to or higher than 20% of your home’s final purchase price.

Say you are buying a home for $300,000. If you come up with a down payment of $60,000 — equal to 20% of $300,000 — you won’t have to pay for PMI.

Is it worth it?

Here’s where the possible benefit of PMI comes in. Coming up with a down payment of 20% can be difficult, especially if you are buying a more expensive home. Consider that $300,000 home example: Can you come up with $60,000 to avoid PMI?

Today, you don’t have to come up with such a large down payment. You might qualify for a conventional loan — one not insured by a government agency — with a required down payment of just 3% of your home’s final purchase price.

For a $300,000 home, a 3% down payment comes out to $9,000. That’s not a small amount of money, but it’s far more doable than $60,000.

PMI is what allows mortgage lenders to accept smaller down payments. The extra financial protection provided by this insurance gives lenders the confidence to take on more risk when originating mortgage loans.

When considering your down payment options, you’ll have to decide whether you want to come up with more money to avoid paying PMI or whether you’d rather save that money to cover your loan’s closing costs or pay for other expenses.

PMI doesn’t last forever

Another piece of good news regarding PMI is that it doesn’t last forever.

Once you build equity in your home of at least 22%, your mortgage lender is required to drop your PMI payments automatically. Equity is the difference between what you owe on your mortgage and how much your home is worth. Once you hit that 22% equity level, you don’t have to do anything: Your lender will simply drop PMI and send you a notice of the resulting change in your mortgage payment.

You can also request that your lender drop PMI after you’ve built up 20% equity in your home. If you request this, your lender will usually order an appraisal to determine the current value of your home.

Writte by Don Amalfitano

Stretch It Out: Is a 40-Year Mortgage Right for You?

Like all fixed-rate mortgages, your interest rate will never change with a 40-year, fixed-rate mortgage. Your rate will remain the same until you pay off your loan, refinance your 40-year mortgage into a new loan or sell your home.

The difference between a 40-year mortgage and other fixed-rate loans comes in the term. The 40-year mortgage comes with a longer term than other loans, one that stretches four decades.

As with other mortgages, you’ll pay this loan back with interest in regular monthly payments. If you hold your loan for its full term, you’ll make 480 payments — 40 years of 12 monthly payments.

What is the benefit of a 40-year mortgage?

The biggest benefit of a 40-year, fixed-rate mortgage is the low monthly payment. Because the repayment period of this loan is stretched out over so many years, your monthly payment will be lower than if you took out a 15-year or 30-year, fixed-rate loan.

This could provide financial relief if you are worried about paying your other bills: Refinancing from a 15-year into a 40-year loan could save you hundreds of dollars a month.

What are the drawbacks?

There are some drawbacks to such a long-term loan. First, you’ll pay far more in interest with a 40-year, fixed-rate mortgage than you would with a shorter-term loan, sometimes tens of thousands of dollars more. That makes a 40-year loan one of the most expensive mortgages you can take out.

Second, it can be difficult to find lenders who provide these loans. These longer-term loans are nonconforming loans. They are also riskier for lenders because with a longer term, there is a greater chance that borrowers will miss payments. Because of this, fewer lenders provide these loans. You can also expect a higher interest rate when you do find a lender that originates 40-year, fixed-rate loans.

A look at the numbers

So, what is the difference in monthly payments and interest between 15-year, 30-year and 40-year, fixed-rate loans? Here’s a look at the differences:

Monthly payment:

- If you take out a 15-year, fixed-rate mortgage for $300,000 at an interest rate of 5.51%, your monthly payment will be $2,452, not including the money you pay for property taxes and homeowners’ insurance.

- If you take out a 30-year, fixed-rate mortgage for $300,000 at an interest rate of 6.32%, your monthly payment, again not including taxes and insurance, will be $1,860.

- With a 40-year, fixed-rate mortgage for the same amount at an interest rate of 6.85%, your monthly payment, not including insurance and taxes, will be $1,831.70.

As you can see, there is a big difference in terms of the monthly payment when you compare 15-year and 40-year mortgages. But this difference isn’t quite as substantial when going from a 30-year to a 40-year mortgage.

Interest:

- With the 15-year mortgage above, you’ll pay a total of $141,595 in interest over the life of your loan.

- With the 30-year mortgage referenced above, you’ll pay a total of $370,488 in interest over the life of your loan.

- With the 40-year loan above, you’ll pay $579,215.50 in interest over the life of your loan.

As you can see, you’ll pay much more interest when paying off a 40-year, fixed-rate loan. You’ll have to determine whether the lower monthly payment is more important than the higher overall costs of this type of loan.

| Don Amalfitano |

| Managing Broker |

| Coldwell Banker Weir Manuel |

The Latest 2024 Housing Market Forecast

The new year is right around the corner, and you might be wondering if 2024 will be the right time to buy or sell a home. If you want to make the most informed decision possible, it’s important to know what the experts have to say about what’s ahead for the housing market. Spoiler alert: the projections may be better than you think. Here’s why.

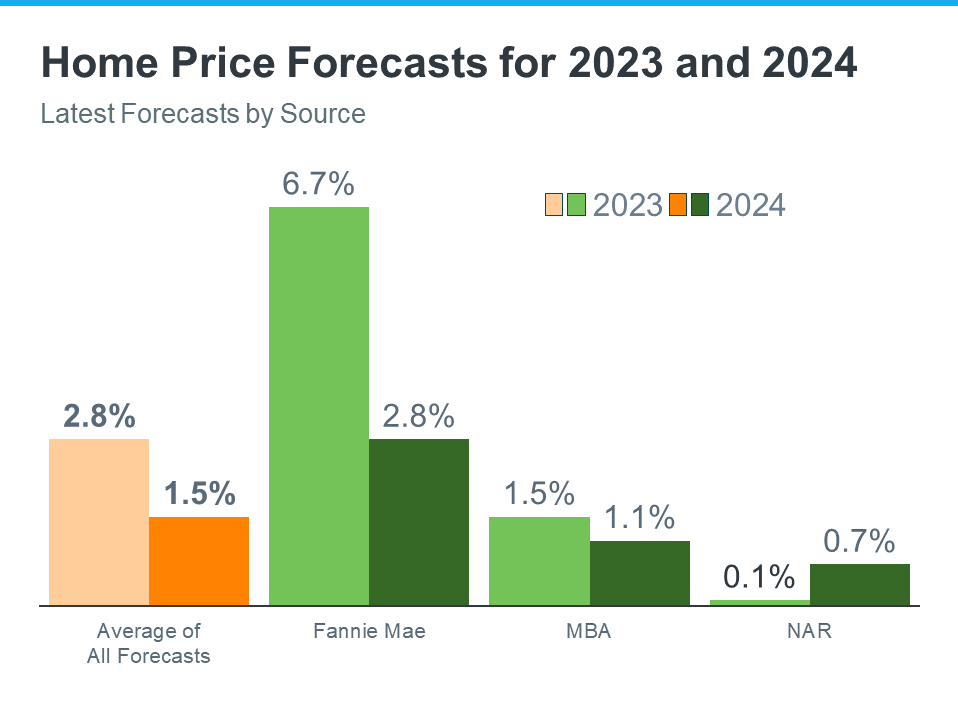

Experts Forecast Ongoing Home Price Appreciation

Take a look at the latest home price forecasts from Fannie Mae, the Mortgage Bankers Association (MBA), and the National Association of Realtors (NAR):

As you can see in the orange bars on the left, on average, experts forecast prices will end this year up about 2.8% overall, and increase by another 1.5% by the end of 2024. That’s big news, considering so many people thought prices would crash this year. The truth is, prices didn’t come tumbling way down in 2023, and that’s because there just weren’t enough homes for sale compared to the number of people who wanted or needed to buy them, and that inventory crunch is still very real. This is the general rule of supply and demand, and it continues to put upward pressure on prices as we move into the new year.

Looking forward, experts project home prices will continue to rise next year, but not quite as much as they did this year. Even though the expected rise in 2024 isn’t as big as in 2023, it’s important to understand home price appreciation is cumulative. In simpler terms, this means if the experts are right, according to the national average, after your home’s value goes up by 2.8% this year, it should go up by another 1.5% next year. That ongoing price growth is a big part of why owning a home can be a smart decision in the long run.

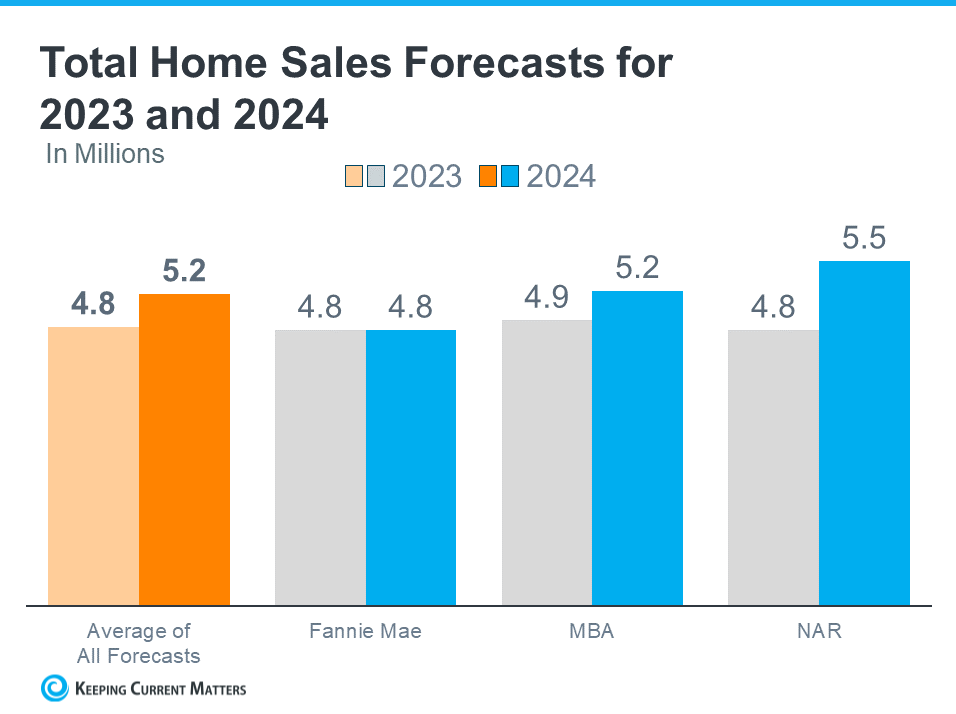

Projections Show Sales Should Increase Slightly Next Year

While 2023 hasn’t seen a lot of home sales relative to more normal years in the housing market, experts are forecasting a bit more activity next year. Here’s what those same three organizations project for the rest of this year, and in 2024 (see graph below):

While expectations are for just a slight uptick in total sales, improved activity next year is a good thing for the housing market, and for buyers and sellers like you. As people continue to move, that opens up options for hopeful buyers who are looking for a home.

So, what do these forecasts show? The housing market is expected to be more active in 2024. That may be in part because there will always be people who need to move. People will get new jobs, have children, get married or divorced – these and other major life changes lead people to move regardless of housing market conditions. That will remain true next year, and for years to come. And if mortgage rates come down, we’ll see even more activity in the housing market.

Bottom Line

If you’re thinking about buying or selling, it’s important to know what the experts are forecasting for the future of the housing market. When you’re in the know about what’s ahead, you can make the most informed decision possible. Connect me to chat about the latest forecasts, and craft a plan for your next move.

Congrats, Your House Made You Rich. Now Sell It.

Lots of baby boomers are going to sell their homes in the years ahead. The trick is to beat the crowd.

Forget the old slogan about there never being a better time to buy a home. For baby boomers, there might never be a better time to sell.

The kids are gone, the stairs aren’t going to get easier to climb, and downsizing with home prices up so sharply since the pandemic could pad out those retirement savings. Many boomers have little or no debt on their current homes and, as an added bonus, it is easy to find ready buyers with so few homes on the market.

The key is beating the crowd. If boomers decided to sell en masse, the prices they would get would be a lot lower than what their home appears to be worth on paper today. Even if they can avoid it now, most are going to have to sell in the years ahead. That could put downward pressure on the prices of the types of homes they live in. Then it might not be a good time to sell anymore.

Ever since they began buying homes in the 1970s, boomers’ effect on the U.S. housing market has been profound. Because it was much more populous than the so-called silent generation that preceded it, the baby-boom generation — typically defined as those Americans born from 1946 to 1964 — drastically increased the country’s need for homes. Construction ramped up, suburbs spread and home prices rose. Many boomers didn’t stop with their first home, either, opting to move into ever larger, more expensive homes as their families, and wealth, grew. Helping the process along: Through much of their prime earnings years, mortgage rates went lower and lower.

In the years before the pandemic, this dynamic appeared to be shifting. An analysis from International Monetary Fund economist Marijn Bolhuis and Harvard University lecturer in economics Judd Cramer conducted just before Covid-19 hit, showed that the larger homes that many boomers owned, and for homes in neighborhoods with more boomers in them, price growth and sales were underperforming other types of homes.

Then everything changed. A newfound desire for living space among younger generations, sub 3% mortgages and the boost to household balance sheets from government relief pushed demand and prices for homes — particularly those in the suburbs — skyward. And even as the pandemic faded, those price gains stuck: As of August, the S&P CoreLogic Case-Shiller national home price index was 46% above its February 2020 level.

Time marches on, though, and the desire and ability of the Generation-X and millennial cohorts to ladder up into the homes the boomers will eventually vacate might be constrained.

The apparent preference many millennials, in particular, had for more urban lifestyles might have gone by the wayside. But they aren’t having as many children as boomers did, reducing the need for those extra bedrooms. Moreover, millennials and Gen Xers who are already homeowners typically still owe money on their homes at mortgage rates that are much lower than what is on offer today. Moving into a more expensive home and having to pay even more interest each month won’t work for them. Meanwhile, younger millennials and other first-time buyers are typically looking for less expensive, starter homes.

A boomer selling wave won’t happen all at once, though. People are healthier in their old age than they used to be, and relative to the generations that both preceded and succeeded them, boomer balance sheets are in good shape. Having spare bedrooms for when the grandchildren and the grandchildren’s parents come to visit ain’t a bad thing.

“They don’t feel the pressure to move at this point,” says Cramer.

The idea of “aging in place” is easy to like, but accomplishing it might not prove so easy. For some boomers, the reasons to sell, either for financial or health reasons, will come sooner rather than later. When that happens, they will need to not only find someone to buy their old house, they will need to find someplace to move into.

Jennifer Molinsky, who directs the Housing an Aging Society Program at Harvard’s Joint Center for Housing Studies, thinks there won’t be a “great senior selloff” in the housing market, but she worries about where aging boomers are going to live. Many people over 75 don’t have the financial wherewithal to move into assisted living, and the supply of age-appropriate homes is limited. Even now, rather than aging in place, many older boomers might be more accurately described as stuck in place. “Smaller, accessible stuff is hard to find,” she says.

Housing bottlenecks could ensue as more big homes come on the market, and the supply of smaller, accessible ones strains to meet demand. Boomers who are able to make the move now could be happier for it.

Nov. 16, 2023 9:00 pm ET

https://www.wsj.com/economy/housing/baby-boomer-home-ownership-3ef78dfa

How does owning a home affect your taxes?

Owning a home can be a smart financial investment and a great way to build your equity. But another substantial benefit can involve a bigger break on Tax Day.

Whether you own now or you’re thinking about buying, tax season is the best time to become familiar with the financial benefits of owning a home.

Fire and comprehensive insurance coverage, title insurance, depreciation, and the cost of utilities such as gas, electric and water are among the items you can’t deduct. But don’t worry—there are plenty of other ways to reduce the amount you owe Uncle Sam.

For homeowners to reduce the amount owed at tax time, start by saying goodbye to the standard deduction and hello to itemizing.

Home mortgage interest

The most significant tax break for many homeowners is the ability to deduct mortgage interest. Assuming you took out a loan to buy your primary home, this applies to you. The entire portion of your payment for mortgage interest can be deducted by itemizing on Form 1040’s Schedule A.

Don’t worry about calculating this amount yourself—your lender will send you a Form 1098 in January that lists the mortgage interest you paid the previous year.

Since the passage of the Tax Cuts and Jobs Act in 2018, the maximum mortgage principal eligible for deductible interest is $750,000. It had been $1 million. That law also made it easier for taxpayers to save more money on their returns by raising the standard deduction amount. That’s why the vast majority of taxpayers now take the standard deduction.

If you took out home loans before December 15, 2017, you are grandfathered into pre-reform limits:

- $1,000,000 for single or married taxpayers filing jointly

- $500,000 for married taxpayers filing separately

If you took out home loans on or after December 15, 2017, your total home loan limits:

- $750,000 for single or married taxpayers filing jointly

- $375,000 for married taxpayers filing separately

The more you pay in mortgage interest payments in a year, the more it makes sense to itemize your deduction. You’ll likely be able to save more that way than with a standard deduction, but you should probably run the numbers to find out.

Real estate taxes

Most state and local governments charge an annual tax on the value of real property, often called property taxes. These funds, though annoying to pay, are used by local and state governments for many positive initiatives in your area. Fortunately, this amount, which varies from state to state, can be deducted. The higher rate your state charges in property taxes, the more you can recoup when filing.

In addition to the property taxes you pay on your home, you may be able to deduct the taxes you pay on a vacation home, car, RV or boat. There are certain restrictions, however, such as the part of your tax bill that goes toward water or trash services. Also, since the implementation of the Tax Cuts and Jobs Act, foreign property taxes can no longer be deducted, and a $10,000 cap ($5,000 if married filing separately)3 has been put in place.

Home Improvement

If you’ve taken on a big home improvement project, and took out a loan to help you finance the project, you’re likely able to deduct interest on it. This includes cash out refinance loans as well as home equity loans and HELOCs. Funds from the loan or cash-out refinance must be used to build or improve your home, or the interest is not deductible.

Home Offices

If you are self-employed as a small business owner, freelancer or contract worker, and you work primarily from a dedicated office in your house or apartment, you can probably claim the valuable home office deduction come tax time.

If you own or rent your dwelling and use part of your home for your business, you may be able to deduct business expenses tied to that use. Your home office has to be used “regularly and exclusively” as your “principal place of business.” So, no claiming the deduction while typing from your pillow-strewn bed or dining room table where you eat.

If you work from multiple locations but claim your home office as your principal place of business, that probably won’t fly, either. The IRS’s rules on this are very prickly, and not following them can raise a red flag.

Ideally, your home office is a separate room. Obviously, that’s not always possible, particularly in small apartments in big cities like New York or Chicago. You need to have what the IRS calls a “separately identifiable space.” It doesn’t have to be sectioned off by a wall or Ikea-style cubicle structure. Many accountants say that installing a folding screen or curtain will do the trick. If you have a separate, free-standing structure, like a studio, garage, workshop or barn, and you use it exclusively and regularly for your business, that can also qualify for the deduction.

What can you deduct, and how do you calculate the amount?

You can deduct from your taxable income certain expenses that are directly and proportionally related to the cost of your home office, like rent, mortgage interest, utilities, painting and repairs. You can also deduct the cost of supplies like computers and desks.

There are two ways to compute the deduction. The first is the regular method: You tally up your entire home’s total expenses and then compute a percentage of them for your home office, as measured in square feet. You also calculate depreciation of eligible property in your home office. In general, if your apartment is 1,600 square feet and your home office is 200 square feet, you would claim 12.5% of your total eligible expenses as your home office deduction.

The second, simpler, method lets you monthly deduct $5 per square foot of the portion of your home that is used for business, up to 300 square feet. For the example above, that would yield a deduction of $1,000.

It may seem obvious, but it’s important not to deduct expenses for any part of your home that is not regularly and exclusively used for business purposes.

Always trust the professionals

While these cover the basics, there are additional ways that savvy homeowners can take advantage of various provisions, from energy credits to penalty-free IRA payouts for first-time buyers.

If you’re looking for more specifics as you prepare to file, check out Publication 530, Tax Information for Homeowners, courtesy of the IRS. You can also talk to a tax advisor, who should be able to help you demystify the tax laws. Complex financial situations like this are why it’s so important to talk to a trusted loan officer when making decisions about your mortgage.

DISCLAIMER:

Coldwell Banker Realty and Guaranteed Rate does not provide tax advice. Please contact your tax advisor for any tax related questions.

https://www.grarate.com/article/exploring-the-tax-benefits-of-homeownership

6 money-saving tips homebuyers should know

Buying a house is always expensive, but recently it has been even tougher for many Americans to afford to buy a home. As of August 2023, the median home price sits at $407,100, according to data from the National Association of Realtors. That’s an increase of nearly 4% year-over-year

To make matters worse, mortgage rates are high right now as well. The national average mortgage rate as of October 17, 2023 is 7.92%. Mortgage rates have gone up over the past 18 months as a reaction to the Federal Reserve enacting a series of rate hikes designed to fight back against inflation.

All of this can leave prospective homeowners struggling to figure out how to afford to buy a home, forcing many to keep renting long after they may have thought they’d be a in a place of their own. Luckily, there are some ways you can save money when buying a home.

6 money-saving tips homebuyers should know

Here are six effective ways homebuyers can save money now.

Find an experienced real estate agent

No matter how much research you do, you’re likely never going to be an expert when it comes to home buying. Just like an athlete needs a great coach or a musician a great producer, you need to make sure you find a good real estate agent.

They will act as your representative, negotiating to get you the best deal possible. A good real estate agent will also steer you away from bad deals and towards deals that make more sense for you.

Make as big a down payment as possible

When you buy a house, you normally put down a chunk of money and take out a mortgage on the rest. The more you put down up front, the less you have to borrow – and the less you have to pay in interest.

Most mortgages require at least 3.5% to 5% as a down payment, but strive to put down even more. Putting down up to 20% on your mortgage could end up saving you big in the long run. And if you put down at least 20%, you probably won’t have to pay private mortgage insurance, which will save you a bit of cash.

Shop around for a lender

There are a lot of companies out there offering mortgages. It might be tempting to just use the bank you do your normal personal banking with, but they might not have the best rate available to you. There are myriad tools out there to compare rates. Just make sure you take your time and do your due diligence to get the best possible deal.

Improve your credit score

The better your credit score is, the better rate you’re going to get on your mortgage. Improve your credit score by paying down debt and making sure you make all payments on time. It might take a little while, but eventually you can improve your credit score and potentially get yourself a better rate on your mortgage.

Negotiate closing costs

Closings costs include things like attorney fees, lender fees and appraisals. Sometimes, you can get the seller to cover some of these costs for you. There is no guarantee that it will work, but it can’t hurt to ask.

Refinance, eventually

As noted above, mortgage rates are high right now. Eventually, they’ll go back down. While you could wait and buy a home when rates are more manageable, you don’t have to delay your dream of homeownership. You can buy a home right now – and refinance your loan when prices go down. You’ll just have to pay attention to refinancing rates and jump on your opportunity when the time is right.

You can get ready to buy a home now by shopping for a mortgage online.

The bottom line

Buying a house is expensive, especially right now. Home prices are high and so are mortgage rates. When combined, that makes buying a place to live even more of a financial adventure than it normally is. Luckily, there are steps you can take to save yourself money, from getting the help of a top-notch real estate agent to shopping around for your loan.

https://www.cbsnews.com/news/money-saving-tips-homebuyers-should-know/

Is a Home Equity Line of Credit Right for You?

You know that you can borrow against the equity that you’ve built in your home, using the funds from home equity loans to pay for whatever you want, whether you’re ready to remodel your aging kitchen or pay off high-interest-rate credit card debt. What you don’t know, though, is whether it makes more sense to take out a standard home equity loan or a home equity line of credit, better known as a HELOC. Which loan product is the better choice?

What are equity loans?

Building equity is one of the main benefits of owning a home. Equity is the difference between the value of your home and the amount you still owe on your mortgage. If you owe $250,000 on your mortgage and your home is worth $375,000, you’ve built $125,000 in equity.

Why does equity matter? If you have it, you can take out either a home equity loan or HELOC that is based on the amount of equity you have. If you have that $125,000 in equity, you might be able to take out a loan or HELOC for up to $90,000, for example. You can then use those funds for anything, though many homeowners will use them to cover major home-improvement projects, to help cover a child’s college tuition or to pay off credit card debt.

But what‘s the difference between a home equity loan and a HELOC?

Home equity loans are typically fixed-rate loans that come with a set repayment term. The money from these loans come in a single lump sum that you pay back with regular monthly payments, with interest, until the loan is paid off.

A HELOC is a bit different; it operates like a credit card with a credit limit based on the amount of equity in your home. A HELOC gives homeowners access to a revolving line of credit that they can draw from when needed.

With a HELOC, you’ll only pay back what you borrowed. For example, if you have access to a line of credit of $90,000 and you then borrow $25,000 to remodel your kitchen, you’ll only pay back that $25,000 that you borrowed.

A HELOC typically comes with two phases. First, there’s your draw period, which usually lasts 10 years. During this period, you can borrow funds up to your HELOC’s credit limit and make interest-only payments. You can also make principal payments on what you’ve borrowed if you choose.

Then there’s the repayment period, which usually lasts 20 years. During this period, you can’t borrow any more money, but instead you must make monthly payments to pay off whatever you borrowed during the draw period.

So, what‘s the smarter choice?

Unfortunately, there is no simple answer to that question. Whether a HELOC is the right choice for you depends largely on what you need money for.

If you need a specific amount of funds for an individual project or goal, such as a home renovation or paying off your credit card debt, a home equity loan might be a better choice. That’s because you receive one lump sum of money that you can use to fund these expenses.

But if you want access to a source of cash that you can use whenever expenses pop up, then a HELOC might be the better choice. Maybe you plan on renovating your home, but you want to tackle a series of projects one at a time. With a HELOC, you can borrow what you need to, say, renovate your kitchen before moving on to borrow more to add a master bathroom.

The best move is to speak with your mortgage lender about whether a home equity loan or HELOC is the better choice for you.

https://newsletter.homeactions.net/archive/full_article/12129/603040/5041928/181218