Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Let Your Home Equity Fund Your Retirement

Struggling with Money? Learn about Home Equity Conversion Mortgages (HECMs)

If you’re low on cash, you might consider a Home Equity Conversion Mortgage (HECM). It’s like a reverse mortgage backed by the government. This means if you meet certain requirements, you can borrow money against the value of your home. The Federal Housing Administration (FHA) guarantees repayment to the lender, so it’s secure. In recent years, HECMs have become more popular, especially among older folks who need extra cash and plan to stay in their homes forever.

Understanding HECM Rules

To qualify for an HECM, you need to be at least 62 years old. Also, you’ll have to pay back the loan when you move out, sell your house, or pass away. You must own your home or have a significant portion paid off, and it must be your primary residence. Plus, you’ll need to have a session with a counselor approved by the Department of Housing and Urban Development (HUD).

Limits and Considerations

The amount you can borrow depends on factors like your age, current interest rates, and the value of your home. Typically, older homeowners with more valuable properties can borrow more.

HECM vs. Regular Mortgages

Unlike traditional mortgages, with HECMs, the amount you owe increases over time. You’ll still need to cover property taxes, insurance, and upkeep costs. Also, the interest you pay isn’t tax-deductible until you pay off the loan.

How You Get Paid

You can choose to receive HECM funds as a lump sum or in monthly payments or a line of credit. You’re free to use the money as you wish, whether for essential expenses, paying off debts, or enjoying life.

HECMs offer a flexible way to access cash when you need it, especially for retirees looking to boost their income.

Attractive features

An HECM offers some compelling advantages if your circumstances fit:

- You can plan on staying in your “forever” home, where you are settled, and can perhaps renovate it, allowing you to age in place.

- You can enjoy a reliable cash flow in order to provide more comfortable senior years.

- You need not make monthly payments on the loan balance.

- Your spouse can usually remain in the home even if you die or move to another accommodation.

- You can pay off debt balances, such as medical bills.

- You can use the proceeds to pay off existing mortgages and thereby prevent foreclosures.

- You can avoid paying withdrawal penalties on other retirement accounts.

- You can fund a grandchild’s education or any other meaningful purpose.

- Integrated protections limit your heirs’ responsibilities.

But is it right for you?

There are several significant drawbacks, so seniors must take extra care with such an important decision:

- Fees tend to be high, including upfront financed origination charges of about 2% and around .5% for annual review of mortgage insurance premiums.

- You could compromise your benefits from needs-based programs, such as Medicaid.

- You could inadvertently default by failing to meet loan requirements, including by living outside the home most of the year, neglecting property taxes or home insurance, or not making maintenance repairs. An unresolved default might lead to eviction and foreclosure.

Alternative loans may be more appropriate. For example, those under age 62 could use home equity loans (HELOCs). More expensive properties may require a jumbo reverse mortgage, with higher interest rates but no mortgage insurance. By contrast, single-purpose reverse mortgages are cheapest and can be used for specified expenses such as taxes or repairs.

Your financial advisor can help you compare different types of reverse mortgages, payment options and other considerations.

Why 90% of Homebuyers Will Continue to Choose Working with Real Estate Agents: Insights from the National Association of Realtors

Members of the National Association of Realtors will continue to be the most reliable partner for the millions of Americans striving to realize the American dream through homeownership.

Specifically, the settlement will prohibit offers of compensation from being shared on multiple listing services (MLSs), the databases that show real estate brokers the properties for sale, and it will require MLS participants to enter into written agreements with their buyers.

These changes will go into effect in mid-late July 2024.

It’s important to note that the National Association of Realtors does not set commissions, and nothing in this proposed settlement would change that. Commissions would continue to be negotiable among buyers, sellers, and their brokers.

The “cooperative compensation” rule that has been subject to litigation says that selling brokers have to specify on each listing an offer of compensation to buyers’ brokers. That offer could be any amount, even zero.

Cooperative compensation, where the compensation a seller pays to their broker is shared, covering the cost of a buyer broker’s services, will continue to be an important option for consumers in all transactions and especially those involving lower and middle-income homebuyers, who may already have a difficult-enough time saving for a down payment.

The bottom line is that consumers will continue to be able to choose what kind of professional real estate advice they’d like–and how much, and how, they will pay for the work of a real estate professional.

Historically, nearly 90% of homebuyers have opted to work with a real estate agent or broker. That figure is unlikely to change.

Even in an era where seemingly everything can be researched and purchased electronically, the clear value added by realtors remains evident. Nine in 10 home buyers would use their agent again or recommend their agent to others.

Seasoned agents and brokers also offer insights into property values, taxes, regulations, and zoning laws while overseeing thorough due diligence processes. And we connect buyers and sellers with other reputable real estate-related professionals such as lawyers, lenders, contractors, and inspectors–any of which can make or break a transaction.

When it comes time to make or evaluate offers, real estate professionals have a decades-long track record as skilled negotiators, ensuring that their clients submit the most competitive bids for their dream home–or hold out for what their home is really worth. And at the settlement table, we help our clients confidently close on what is likely the most significant financial transaction of their lives.

Even post-sale, real estate agents and brokers are crucial advisors for their clients, providing ongoing support, answering queries, and offering guidance as people confront the challenges and delights of homeownership.

NAR’s proposed settlement agreement and the associated practice changes will not change what makes realtors valuable: specialized knowledge, diligence, and a commitment to our clients’ best interests. And it does not change the fact that millions of people will continue to rely on us to help them fulfill their dream of homeownership.

Find the original article here

4 Tips To Make Your Strongest Offer on a Home

Are you thinking about buying a home soon? If so, you should know today’s market is competitive in many areas because the number of homes for sale is still low – and that’s leading to multiple-offer scenarios. And moving into the peak homebuying season this spring, this is only expected to ramp up more.

Remember these four tips to make your best offer.

1. Partner with a Real Estate Agent

Agents are local market experts. They know what’s worked for other buyers in your area and what sellers may be looking for. That advice can be game changing when you’re deciding what offer to bring to the table.

2. Understand Your Budget

Knowing your numbers is even more important right now. The best way to understand your budget is to work with a lender so you can get pre-approved for a home loan. Doing so helps you be more financially confident and shows sellers you’re serious. That gives you a competitive edge. As Investopedia says:

“. . . sellers have an advantage because of intense buyer demand and a limited number of homes for sale; they may be less likely to consider offers without pre-approval letters.”

3. Make a Strong, but Fair Offer

It’s only natural to want the best deal you can get on a home, especially when affordability is tight. However, submitting an offer that’s too low does have some risks. You don’t want to make an offer that’ll be tossed out as soon as it’s received just to see if it sticks. As Realtor.com explains:

“. . . an offer price that’s significantly lower than the listing price, is often rejected by sellers who feel insulted . . . Most listing agents try to get their sellers to at least enter negotiations with buyers, to counteroffer with a number a little closer to the list price. However, if a seller is offended by a buyer or isn’t taking the buyer seriously, there’s not much you, or the real estate agent, can do.”

The expertise your agent brings to this part of the process will help you stay competitive and find a price that’s fair to you and the seller.

4. Trust Your Agent During Negotiations

After you submit your offer, the seller may decide to counter it. When negotiating, it’s smart to understand what matters to the seller. Once you do, being as flexible as you can on things like moving dates or the condition of the house can make your offer more attractive.

Your real estate agent is your partner in navigating these details. Trust them to lead you through negotiations and help you figure out the best plan. As an article from the National Association of Realtors (NAR) explains:

“There are many factors up for discussion in any real estate transaction—from price to repairs to possession date. A real estate professional who’s representing you will look at the transaction from your perspective, helping you negotiate a purchase agreement that meets your needs . . .”

Bottom Line

In today’s competitive market, be sure to work with a local real estate agent to find you a home you love and craft a strong offer that stands out.

Finding Your Perfect Home in a Fixer Upper

If you’re trying to buy a home and are having a hard time finding one you can afford, it may be time to consider a fixer-upper. That’s a house that needs a little elbow grease or some updates, but has good bones. Fixer-uppers can be a really great option if you’re looking to break into the housing market or want to stretch your budget further.

Basically, since the number of homes for sale is still so low, if you’re only willing to tour homes that have all your dream features, you may be cutting down your options too much and making it harder on yourself than necessary. It may be time to cast a wider net.

Sometimes the perfect home is the one you perfect after buying it.

Here’s some information that can help you pinpoint what you truly need so you can be strategic in your home search. First, make a list of all the features you want in a home. From there, work to break those features into categories like this:

- Must-Haves – If a house doesn’t have these features, it won’t work for you and your lifestyle.

- Nice-To-Haves – These are features you’d love to have but can live without. Nice-to-haves aren’t dealbreakers, but if you find a home that hits all the must-haves and some of these, it’s a contender.

- Dream State – This is where you can really think big. Again, these aren’t features you’ll need, but if you find a home in your budget that has all the must-haves, most of the nice-to-haves, and any of these, it’s a clear winner.

Once you’ve sorted your list in a way that works for you, share it with your real estate agent. We can help you find homes that deliver on your top needs right now and have the potential to be your dream home with a little bit of sweat equity. Lean on our expertise as you think through what’s possible, what features are easy to change or add, and how to make it happen.

Your agent can also offer advice on which upgrades and renovations will set you up to get the greatest return on your investment if you ever decide to sell down the line.

Bottom Line

If you haven’t found a home you love that’s in your budget, it may be worth thinking through all your options, including fixer-uppers. Sometimes the perfect home for you is the one you perfect after buying it. To see what’s available in your area, you can search here!

Why We Aren’t Headed for a Housing Crash

If you’re holding out hope that the housing market is going to crash and bring home prices back down, here’s a look at what the data shows. And spoiler alert: that’s not in the cards. Instead, experts say home prices are going to keep going up.

Today’s market is very different than it was before the housing crash in 2008. Here’s why.

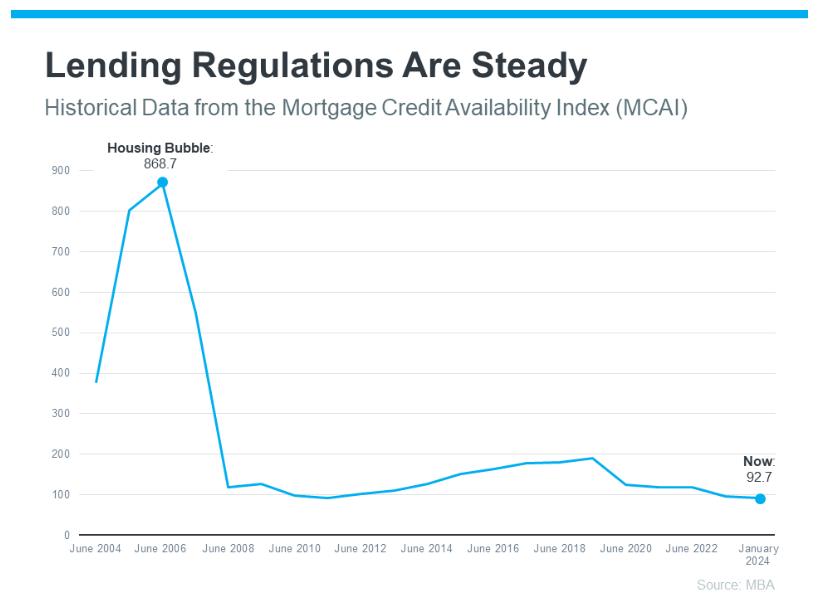

It’s Harder To Get a Loan Now – and That’s Actually a Good Thing

It was much easier to get a home loan during the lead-up to the 2008 housing crisis than it is today. Back then, banks had different lending standards, making it easy for just about anyone to qualify for a home loan or refinance an existing one.

Things are different today. Homebuyers face increasingly higher standards from mortgage companies. The graph below uses data from the Mortgage Bankers Association (MBA) to show this difference. The lower the number, the harder it is to get a mortgage. The higher the number, the easier it is:

The peak in the graph shows that, back then, lending standards weren’t as strict as they are now. That means lending institutions took on much greater risk in both the person and the mortgage products offered around the crash. That led to mass defaults and a flood of foreclosures coming onto the market.

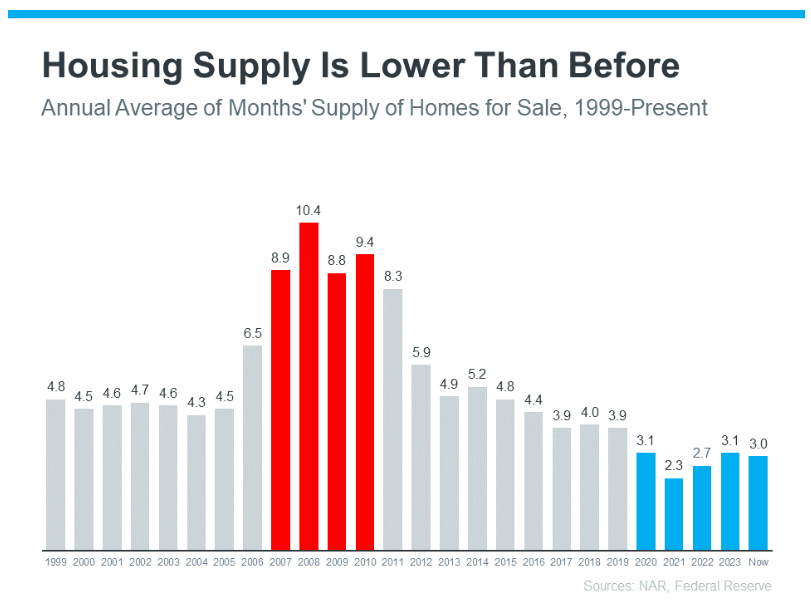

There Are Far Fewer Homes for Sale Today, so Prices Won’t Crash

Because there were too many homes for sale during the housing crisis (many of which were short sales and foreclosures), that caused home prices to fall dramatically. But today, there’s an inventory shortage – not a surplus.

The graph below uses data from the National Association of Realtors (NAR) and the Federal Reserve to show how the months’ supply of homes available now (shown in blue) compares to the crash (shown in red):

Today, unsold inventory sits at just a 3.0-months’ supply. That’s compared to the peak of 10.4 month’s supply back in 2008. That means there’s nowhere near enough inventory on the market for home prices to come crashing down like they did back then.

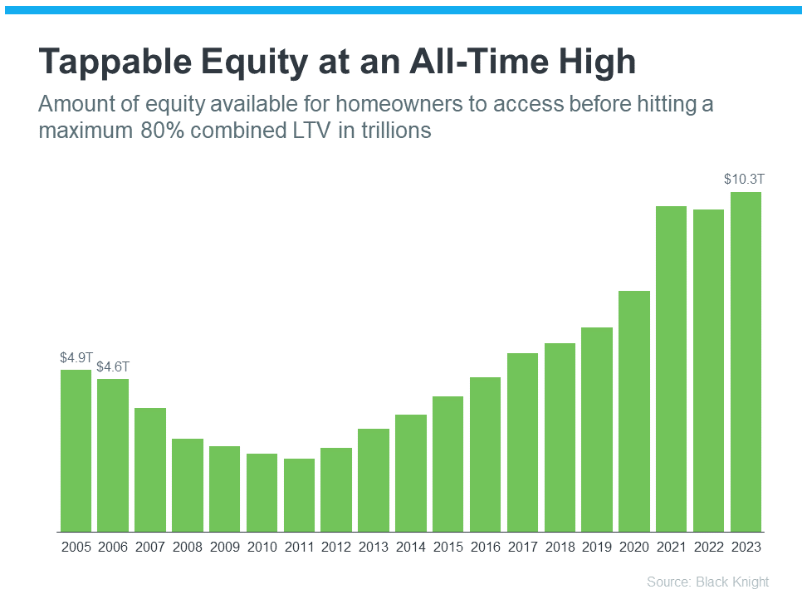

People Are Not Using Their Homes as ATMs Like They Did in the Early 2000s

Back in the lead up to the housing crash, many homeowners were borrowing against the equity in their homes to finance new cars, boats, and vacations. So, when prices started to fall, as inventory rose too high, many of those homeowners found themselves underwater.

But today, homeowners are a lot more cautious. Even though prices have skyrocketed in the past few years, homeowners aren’t tapping into their equity the way they did back then.

Black Knight reports that tappable equity (the amount of equity available for homeowners to access before hitting a maximum 80% loan-to-value ratio, or LTV) has actually reached an all-time high:

That means, as a whole, homeowners have more equity available than ever before. And that’s great. Homeowners are in a much stronger position today than in the early 2000s. That same report from Black Knight goes on to explain:

“Only 1.1% of mortgage holders (582K) ended the year underwater, down from 1.5% (807K) at this time last year.”

And since homeowners are on more solid footing today, they’ll have options to avoid foreclosure. That limits the number of distressed properties coming onto the market. And without a flood of inventory, prices won’t come tumbling down.

Bottom Line

While you may be hoping for something that brings prices down, that’s not what the data tells us is going to happen. The most current research clearly shows that today’s market is nothing like it was last time.

Should you wait for rates to fall before purchasing a home?

According to this article, if you’re in the market for a new home, today’s mortgage rates can hinder your efforts. After all, the higher your mortgage rate, the higher your monthly payments will typically be. So, it can be difficult to find affordable housing options in today’s high-rate environment.

But the good news is that there are still good housing options available. And, while waiting for a lower interest rate might seem like a smart move, some experts say doing so would be a mistake. But why wouldn’t you want to wait for lower mortgage rates before you purchase a new home?

Why some experts say you shouldn’t wait for mortgage rates to fall

Interest rates are a common consideration among home buyers — but should you wait until mortgage rates fall to buy? Many experts say no. Here’s why.

Lower rates could lead to lower inventories and higher prices

“Buying a home is a big decision that needs careful consideration,” says John Dustman, SVP, head of consumer lending and advisor banking at Axos Bank.

“One common concern among buyers relates to market conditions and how changes in interest rates impact home prices and inventory levels,” says Dustman. “As most house hunters know, inventory levels in just about every community in the U.S. are very low and have been since the COVID-19 pandemic and historically low mortgage rates available in 2020 and 2021.”

“Active inventory fell to levels that were a third or less than inventory levels in 2019 during the 2021 peak in demand,” says Dustman. “Since then, inventory levels have increased but are still at levels equal to about 50-60% of available inventory in 2019.”

Considering the low inventory levels, home prices would typically rise. However, with rates as high as they are right now, it may be keeping home values from increasing further, according to Dustman. But that may change.

“Many buyers have been waiting on the sidelines due to high rates and challenges they are facing qualifying for mortgages with high rates and home prices,” says Dustman. As rates fall and these buyers on the sidelines flood the market, inventory could fall further and home prices could rise.

That’s why, generally speaking, the best time to buy a home is when rates are higher and demand is lower, according to Dustman.

You could miss out on your dream home if you wait too long

It can be difficult to find your dream home with inventories low across most housing markets nationwide. However, if you wait too long, you could miss out entirely.

“People are always going to need to buy homes — whether they are upsizing with a growing family, downsizing as empty nesters, moving for a job or are simply ready to take the next step in their life’s journey and become a homeowner for the first time,” says Austin Niemiec, chief revenue officer for Rocket Mortgage.

“Maybe someone’s dream home becomes available and it doesn’t coincide with the most favorable rate environment, but waiting for rates to drop could mean missing out on that perfect opportunity,” says Niemiec. “As long as they can comfortably afford the payment now, the homebuyer always has the chance to refinance if rates drop in the future to get a better monthly payment.”

It’s hard to time the market

“Trying to time the homebuying market and rates is difficult because no one has a 100% accurate crystal ball to predict what conditions will look like even in a few months from now,” says Bob Driscoll, SVP and director of residential lending at Rockland Trust Bank. “The ‘perfect time’ to buy a home is a myth.”

“Instead, prospective homebuyers should buy a home on a timeline that works best for their life and future plans,” says Driscoll. “Aligning your home purchase with your goals and values will certainly have a better return on your investment than waiting around for rates to fall.”

Learn more about your mortgage options now.

The bottom line

Interest rates could drop in the future, but you may not want to wait for that to happen to buy a home. If you wait for rates to fall, you could face higher home prices or miss out on your dream home. Rather than waiting for rates to fall, it may be a wise choice to purchase your home now and consider refinancing later.

Should I Buy a House Now or Wait for Mortgage Rates to Go Down?

Contemplating the purchase of a home or diligently saving for a down payment? The recent surge in mortgage rates may have prompted a crucial question in your mind: Is now the best moment to invest in a home, or should you bide your time until mortgage rates go down?

In order to assist you in making an informed decision that aligns with your family’s best interests, let’s dive into the financial aspects—without any intimidating mathematical complexities. Together, we’ll explore whether the current circumstances favor your home-buying endeavors or if it might be prudent to defer this decision for a more favorable period.

Let’s take a look at what financial Guru Dave Ramsey had to say about this question:

Should I Buy a House Now or Wait?

Yes, you should buy a house now if you’re financially ready to do so. Here are the biggest reasons why that’s the best move:

- If interest rates continue to drop, then house prices will start going up. Lots of folks haven’t been able to afford a house because of high interest rates, so they’ve been sitting and waiting. As rates keep getting lower, more and more of those people will start buying homes—and sellers will be able to raise their prices because of that increase in demand.

- You can always refinance down the road. If you buy now and interest rates continue dropping over the next year or two, you can still take advantage of the lower rates by refinancing your mortgage. On the other hand, if you wait to buy and home prices go up, you’re stuck with the higher prices.

- Mortgage interest rates may be high right now, but they’ve already begun to drop. That means, if you buy now, you’ll already be getting a better deal than you would have in 2023.

- The Federal Reserve (also known as the Fed) is unpredictable. We never know exactly what the Fed will decide to do with the federal funds rate, which directly impacts mortgage rates across the country (more on that later).

Here’s the deal, though: You should only buy a house if you’re prepared financially. How do you know if you’re financially ready to buy a house? Let’s break it down.

Am I Prepared Financially to Buy a House?

If you’ve checked these four boxes, you’re in the clear to buy a house!

- You’ve paid off your debt. Focus on paying off all your consumer debt before you buy a house. Getting rid of student loans, credit card payments and car notes will give you more margin in your budget—and that’s super important as a homeowner.

- You have a full emergency fund. Saving up an emergency fund of 3–6 months of your typical expenses before you buy will be the difference in whether a broken HVAC unit, fridge or washing machine is a catastrophe or merely an inconvenience.

- You’ve saved a strong down payment. If you’re a first-time home buyer, you need a down payment of at least 5–10%. But if you can swing a 20% down payment, that’s even better. Why? Putting 20% down will keep you from having to pay for private mortgage insurance (PMI), an extra monthly fee that could add hundreds to your house payment.

- You can afford the house payment. Don’t buy a house if the monthly payment (including principal, interest, homeowners insurance and HOA fees) on a 15-year fixed-rate mortgage would be more than 25% of your take-home pay. Any more than that, and you run the risk of not having enough money left in your budget each month to put toward other important financial goals—aka, you’ll be house poor.

If you haven’t checked one or more of those boxes, that’s where you need to direct your focus for now. We know how badly you want to be a homeowner and start building equity. But we talk to people every day who bought a house before taking those steps and wound up regretting it because they got stuck with a giant, expensive burden.

Will Mortgage Rates Go Down in 2024?

Yes, mortgage rates are expected go down in 2024. Average U.S. rates for both 30-year and 15-year fixed-rate mortgages began steadily dropping in November 2023, and that trend continued into January 2024.2 Rates will likely keep going down throughout the rest of the year, especially since the Fed projected that it will lower the federal funds rate three times in 2024.3

But even as mortgage rates continue to go down in 2024, odds are the drop won’t be drastic—it’s not like rates are going to quickly return to the 2–3% range we saw at the end of 2021. The bottom’s not about to fall out here.

For example, even though the National Association of REALTORS® believes rates will go down in 2024, they’re only predicting a 1.2% drop (from 7.5% to 6.3% for 30-year mortgages) by the end of the year.4 A lower rate is definitely nice, but that small of a drop would only save you a couple hundred bucks on your monthly payment, if that.

It’s a discount, sure, but it’s not worth waiting around for—especially since, like we talked about earlier, you can refinance down the road.

How Do Federal Interest Rate Hikes Affect Mortgages for Home Buyers?

When interest rates go up in the real estate world, so do monthly payments and the total amount of interest you’ll pay on a mortgage. How much? Here’s an example.

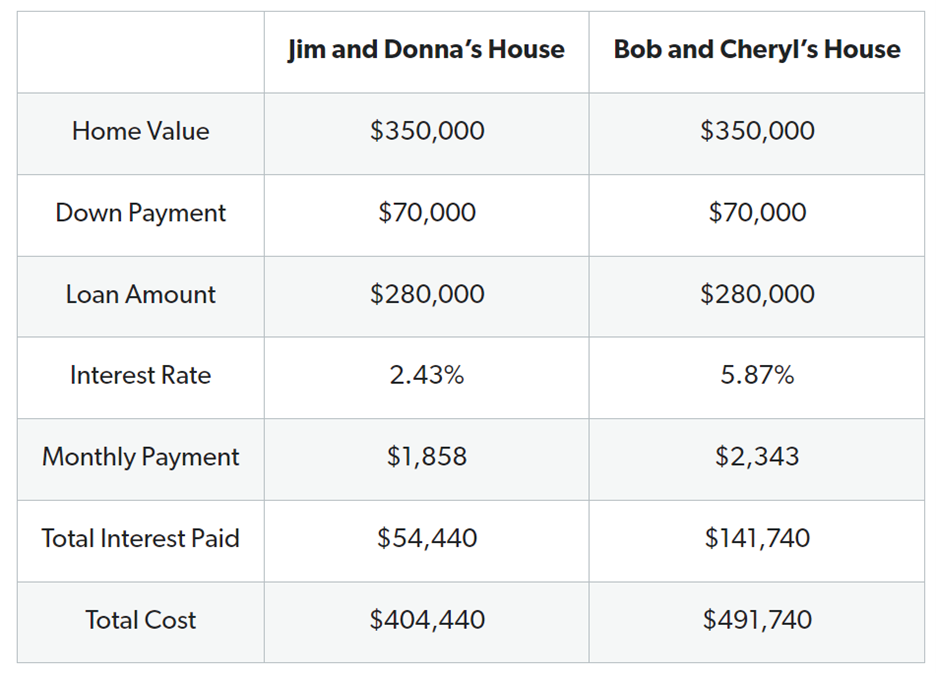

Let’s say we have two couples who each bought $350,000 houses with 20% down and 15-year fixed-rate mortgages. Couple #1, Jim and Donna, bought their house in January 2022 when the typical interest rate was around 2.4%. Couple #2, Bob and Cheryl, bought their house less than two years later in January 2024—when the average rate was nearly 5.9%.5

We used our Mortgage Calculator to see what both couples will pay for their houses. To keep things simple, we left out costs for property taxes, homeowners insurance, and homeowners association (HOA) fees.

Bob and Cheryl will pay over $90,000 more in interest than Jim and Donna—even though their home value and loan terms are the same. Plus, Bob and Cheryl’s house payment is over $500 more per month. Ouch!

What Is the Federal Reserve?

Okay, we’ve mentioned the Fed a couple of times and talked about how interest rate hikes can affect you. But what is the Fed anyway?

Well, the Federal Reserve is the U.S. central bank that creates money and sets interest rates. Its main goal is to keep the economy running smoothly by having low unemployment and low inflation.

The Fed is kind of like a mechanic who tinkers around with a car to make it purr like a kitten, and one of its favorite tools is (shocker) interest rates.

Why Does the Fed Raise Interest Rates?

The Fed raises interest rates to encourage people to borrow less, spend less and save more—which should slow down inflation.

Now, the Fed doesn’t tell commercial banks what interest rates to charge on loans, but they do influence the banks’ rates by setting their federal funds rate. The fed funds rate is the interest rate banks charge to each other for overnight loans, and it influences most other interest rates.

So, even though the Federal Reserve doesn’t actually set mortgage interest rates, its decisions can still affect your mortgage. For example, mortgage rates went up in early 2022—even before the Fed started raising rates. That’s because banks saw what was coming and started upping interest rates to protect their profits.

The Bottom Line

No one likes it when interest rates go up, but it’s not the end of the world. This is still a great time to buy a house—you’ll just pay more than you would’ve a couple years ago. It’s also a good time to sell a house. And if you already have a fixed-rate mortgage locked in, you’re in good shape too.

While it’s smart to get the lowest possible interest rate on your mortgage, that doesn’t mean you have to wait years to buy or sell a house—or to refinance if your current loan just isn’t working for you. You get to decide when to buy a house based on what’s right for you and your family, not what the Fed is doing.

Frequently Asked Questions

Will the Fed raise interest rates again?

Is 2024 a good time to buy a house?

Will my mortgage payment go up if rates increase?

Should I lock in my mortgage now?

350,000 Californians are now on the FAIR Plan, the last resort for fire insurance. Now what?

The fire-insurance premium for Bill King’s home has risen 145% since 2017 — from $399 to $979 — under the California FAIR Plan, the state’s last option for homeowners seeking fire insurance.

Add that to the increase in his auto-insurance premium, and King, who lives in Running Springs in the San Bernardino Mountains, is worried.

“What do I do?” asked King, a retiree who will turn 70 years old this summer. “Do I move out of California? At some point I’m going to have to look at things… Will I be able to face future increases depending on how long I’ll live?”

A former Orange County employee, he said he’s having a tough time wrapping his head around the situation: “It’s hard when you’ve planned your retirement and your insurance company comes along and threatens your economic well-being.”

King’s story is similar to that of other property owners who have turned to the FAIR Plan as many insurers have stopped issuing fire insurance in the state, citing climate risks and inflation. As the FAIR Plan has exploded in size — from 126,709 policies in 2018 to more than 350,000 today — homeowners and insurance brokers say they are now facing problems such as delays in mortgage closings, or homeowners losing their coverage.

Recently, King found he was unable to pay for his policy renewal online, as he usually does. He couldn’t email the FAIR Plan because the plan’s website does not provide an email address. Instead, the website tells homeowners to contact their insurance brokers. King’s broker found out that he had been assigned a new policy number without his knowledge. He barely had time to send a payment via his broker, putting him dangerously close to cancellation. Based on his individual experience, King has concluded that the FAIR Plan “is doing everything it can to help policies lapse.”

The FAIR Plan Association, a pool of insurers required by state statute to provide fire-insurance policies when property owners can’t find them elsewhere, is experiencing major growing pains.

The California Insurance Department, which under state law has oversight over the FAIR Plan — including approving its requested rate changes — in 2020 investigated consumer complaints about non-renewals and cancellations. But even after an agreement late last year that included the FAIR Plan vowing to change some of its practices, there continue to be fresh signs of turmoil.

The plan is supposed to be a temporary solution as well as a last resort for property owners, but many people, like King, have been buying insurance through the association for years.

Hilary McLean, a FAIR Plan spokesperson, said the number of policy-holders who stay on the plan has increased over the years; 90% of current FAIR Plan customers are renewing their policies for another year.

The Insurance Department has proposed new regulations, expected to be finalized at the end of the year, to try to get insurers to resume writing fire policies in the state again. But it could be a couple of years until that happens, so the FAIR Plan is likely to continue growing, which could threaten its solvency because it is taking on additional high-risk policies.

“It’s clear that a growing FAIR Plan is a problem for all Californians because of the solvency risks from a major wildfire,” said Michael Soller, spokesperson for the Insurance Department, in an email. “The commissioner’s strategy is focused on returning people to the normal market from the FAIR Plan.”

Last year, lawmakers concerned about the solvency of the FAIR Plan tried to find a legislative solution to address it and other concerns about the state’s insurance market, but no lawmaker sponsored a bill to do so.

A copy of the proposed bill language, seen by CalMatters last week, shows it would have allowed the FAIR Plan to pay for claims by issuing bonds through the California Infrastructure and Economic Development Bank, which provides low-cost financing to state and local government entities. Although the FAIR Plan is not a state entity, the bill would have deemed it “in the public interest” for the FAIR Plan to qualify for financing through the bank.

FAIR Plan President Victoria Roach refused to speak on the record for this story. Spokesperson McLean said the association is dealing with an onslaught of new applications — about 900 a day, down from 1,000 a day last November but up from 350 a day in December 2022. Incoming phone calls nearly doubled over the last half of 2023, to more than 50,000 phone calls a month. The association has hired more people, bringing the number of staff to more than 200 employees plus 80 temporary workers, to help handle the additional workload.

Making matters worse, at the end of last year the FAIR Plan went ahead with long-planned changes to its software system, leading to confusion. McLean acknowledged that led to some homeowners getting kicked off the plan — or as King describes his case, almost getting kicked off — for payment issues.

Georgia, a Placer County homeowner who requested that her last name not be used for privacy reasons, said that in mid-December, her insurance broker informed her the day her premium was due that her payment had not been received, even though the money was in escrow and she later found out that her mortgage company had already paid it. The result: She, her husband and their three kids had to part with $2,380 right before Christmas to pay their premium because they didn’t want to risk losing fire insurance.

“That was my car payment, Christmas, everything we had,” she said. Her broker, mortgage company and the FAIR Plan told her she would get her money back on Jan. 5, she said, but added that she has yet to receive it.

Meanwhile, insurance broker Tyler Nelson said the new system caused delays that led to his clients losing out on loans for homes in escrow. Nelson said he would call the FAIR Plan, wait on hold for three hours and get no help. The new system, called Duck Creek, is “the most awful thing I’ve literally ever dealt with,” he said in an email.

The FAIR Plan would not discuss individual cases and complaints. McLean said the association notified brokers that they were adopting a new system, and offered them training and help. She also said the plan has made changes that “have greatly reduced delays and otherwise improved service levels.”

“In the very rare instance of a policy being canceled in error, the FAIR Plan works diligently to resolve the issue and restore coverage per the customer’s original policy agreement,” she added.

Soller, the spokesman for the Insurance Department, said consumers should contact the department if they have trouble getting coverage from the FAIR Plan.

Even before the FAIR Plan’s software transition, Ann Avalos lost her Auburn home’s fire-insurance policy in 2021 because of a payment issue after her mortgage was sold to another company.

The FAIR Plan “didn’t contact anyone until days before they dropped me,” she said, and refused to give her a grace period or reinstate her. “No communication, customer service, compassion,” she added. Her only recourse was to reapply for another policy, and she said her $2,257 annual premium increased to $3,481. Last year, she said it rose again, to $3,686. And because she can’t get fire insurance anywhere else, she has no choice but to accept the price increases.

Asked to respond, McLean said: “FAIR Plan policy agreements detail customer responsibilities… these responsibilities are consistent with industry standards, such as on-time payments and maintaining the structural integrity of the dwelling.”

“Why wouldn’t they drop you?” Avalos asked, noting that the association’s members are the insurers themselves. “Now they have the opportunity to double what they charge you.”

“We disagree with this characterization,” McLean said. “FAIR Plan rates are approved by the California Department of Insurance and rates are the same for new policyholders and renewing customers.”

The agreement reached by the Insurance Department and the FAIR Plan in November over complaints of non-renewals and cancellations between 2016 and 2019 has led the plan to make changes. One of them is to allow policy-holders to pay a surcharge if there’s a fixable issue on their property, instead of citing it as a reason to cancel their plan. Once the issue is taken care of, the surcharge is canceled. Soller, speaking for the state Insurance Department, said that because of the agreement, the FAIR Plan “should be making it easier, not harder,” for homeowners to renew their plans.

As King thinks about his own insurance worries and his future in California, he has also had to contend with FAIR Plan premium increases for his local church, where he is an associate pastor. A couple of years ago, he said, the fire-insurance premium for the church’s main building doubled from $4,000 to $8,000.

“That’s a lot of money for our little church,” he said, noting that the church’s annual budget was less than $70,000. So instead he shopped around and found a business policy that included fire insurance, which is costing the church about $6,000. “Insurance at times seems like a great evil perpetrated upon us,” he said.

Top 5 Home Renovations with the Best Return on Investment

Well-planned home renovations can really enhance your home’s appeal and amp up its price when it’s time to sell. But not all improvements bring a hefty return on investment (ROI). Knowing the most promising updates can help strategize your revamping efforts for an attractive sale. Read on for a rundown of the top five home improvements likely to supercharge your property’s resale value.

Kitchen Upgrades

A modern, functional kitchen can impress prospective buyers and significantly boost your resale value. But a complete remodel isn’t always necessary when you’re looking for a sizable ROI. If your kitchen already has a good layout, work with what you have and make strategic changes. Key renovations to consider include new countertops, an updated backsplash, a fresh coat of paint, and high-end appliances. Need some swoon-worthy inspiration to get you in the mood? These kitchen updates will make you want to start taking notes and making plans.

Bathroom Remodels

Bathroom updates are next on the list of top ROI home renovations. Your efforts here can range from replacing dated fixtures to a more comprehensive refresh, including a new soaking tub or a sleek walk-in shower. But before you pencil in a new skylight and heated floor tiles, consider every tweak’s necessity and potential upside, as bathroom work – like kitchen updates – can quickly become expensive. But if you can invest more in this space, you’ll likely see significant returns.

Hardwood Flooring

There’s no question about it – adding or refinishing lackluster hardwood flooring can significantly enhance the value of your home. This type of flooring offers a timeless look that harmoniously blends with various design styles, from boho chic to classic elegance. Besides their aesthetic charm, hardwood floors are sturdy, easy to clean and healthier due to the absence of trapped allergens often found in carpets. Buyers are consistently willing to pay more for a house with hardwood, making this upgrade a wise choice if you can swing it. How much will wood floors cost you? It all depends on the size of your rooms, the style you choose and the tree species.

There’s no question about it – adding or refinishing lackluster hardwood flooring can significantly enhance the value of your home. This type of flooring offers a timeless look that harmoniously blends with various design styles, from boho chic to classic elegance. Besides their aesthetic charm, hardwood floors are sturdy, easy to clean and healthier due to the absence of trapped allergens often found in carpets. Buyers are consistently willing to pay more for a house with hardwood, making this upgrade a wise choice if you can swing it. How much will wood floors cost you? It all depends on the size of your rooms, the style you choose and the tree species.

Eco-Friendly Improvements

Energy-conscious renovations have been in vogue for a while now. An energy-efficient home attracts a broad range of buyers and contributes to a greener, healthier environment for everyone. Energy-saving windows, LED lighting, Energy Star-certified appliances, higher-rated insulation, an updated HVAC system and solar panels can offer a higher selling price point and significant cost savings for the homeowner.

Adding an extra room or an outdoor living space

Expanding your total livable space can add considerable worth to your home, whether it’s a finished basement, attic or flex space. An additional bedroom or an office are always in demand, especially in this work-from-home era. If expanding indoors isn’t feasible, transform your outdoor area into a relaxing second living room. A deck or patio can be an enticing bonus for buyers looking for more usable square footage at the property. Swanky garage conversions can also provide extra room year-round with unique appeal.

The right home upgrades can substantially increase your property’s value. However, balancing your renovation budget with the prospective benefits is crucial. In addition to this list, research your market and pay attention to what features the top-selling homes in your area offer. Give me a call and I can help you make informed decisions and optimize your home renovations for the best ROI.

Want to Add a Granny Flat or Rental ADU? Here’s How to Finance It

Are you dreaming of adding an accessory dwelling unit (ADU) to your property? Whether it’s a granny flat, carriage house, or backyard cottage, ADUs are gaining popularity as an innovative solution to the shortage of affordable housing in the United States. In this guide, we’ll explore the financing options and trends that make realizing your ADU dream easier than ever.

Why ADUs Are in Demand

The demand for ADUs is on the rise, driven by a shortage of affordable housing in the US. Local and state laws are evolving to make it easier for homeowners to build ADUs, with some areas adopting “by-right approval,” reducing barriers to construction. Homeowners are exploring ADUs not only as a rental income source but also as a way to keep loved ones close by, offering an alternative to expensive nursing homes.

Types of Accessory Dwelling Units

Before diving into financing, it’s crucial to understand the types of ADUs available. From additions to existing structures to stand-alone constructions in the backyard, ADUs can take various forms. Fannie Mae sets basic requirements, such as a separate entrance, kitchen, sleeping space, and bathroom. Local regulations may dictate specifics like parking and utility hookups.

Varieties of ADU Loans

Considering financing options is a key step in turning your ADU dream into reality. Two main approaches exist: borrowing equity or opting for a construction/renovation loan.

1. Borrowing from Equity:

– Ideal for those with sufficient equity and a desire to maintain a low-rate primary mortgage.

– Potential drawbacks include higher interest rates on equity products and borrowing limitations (up to 80% of the home’s current value).

2. Construction or Renovation Loans:

– Suitable when borrowing from equity falls short.

– Allows you to borrow more based on the projected value of your property after ADU construction.

– Drawback includes accepting a potentially higher mortgage rate.

Renting Out Your ADU

If you plan to rent out your ADU, some loan programs may consider a portion of the tenant’s rent as income during the loan application process. This varies by program and may depend on factors like your previous experience as a landlord.

Finding the Right Lender

Whether you decide to borrow equity or opt for a construction/renovation loan, finding the right lender is crucial. Contractors can be valuable sources of lender referrals, helping you assess your financing needs early in the process. Alternatively, you can start by reaching out to a trusted mortgage lender for guidance and potential contractor referrals.

Unlock the potential of your property with an ADU and explore the financing options that align with your goals. From keeping family close to generating rental income, ADUs offer a versatile solution to the evolving housing landscape. Start your journey towards an enhanced living space today!