You want to sell your home, but the kids have scuffed up the floors and chipped the paint. The kitchen could use a face-lift and the lawn has seen better days.

The consensus among the dozen real-estate agents interviewed by The Wall Street Journal: Don’t go overboard.

Shelling out small sums to punch up highly-visible parts of the property, particularly outside, increases the curb appeal. Spending large amounts to turn the place into your dream home doesn’t make it someone else’s dream home. (Below is a bang-for-your buck guide.)

“Sellers should avoid trying to become a general contractor,” said Scott Harris, a real-estate agent at Brown Harris Stevens in New York.

What to fix

Replacing a garage door cost $4,513 on average in 2024, but added $8,751 to the resale value, recouping 194% of the cost, according to Zonda, a residential construction-focused research company. That project provided the most value in the firm’s annual cost-value comparison.

Replacing an entry door cost $2,355 on average and added $4,430 to resale value, recouping 188% of the cost.

“They will recoup all of that with very low risk, and it’s a low outlay,” says Todd Tomalak, principal at Zonda, about exterior doors.

Minor exterior work is some of the most likely to pay off. It makes the house look nicer in listing photos and brings potential buyers through the door, real-estate agents say.

A National Association of Realtors survey from 2023 found that sellers would recoup 217% of the cost of lawn care, 104% of the cost of landscape maintenance, and 100% of the cost of overall landscape upgrades.

Small-ticket items inside the house are worthwhile, too. Refinishing hardwood floors on a roughly 2,500 square foot home costs an estimated $3,400, but adds roughly $5,000 to the value of the house, according to a 2022 NAR survey.

What to skip

There is a high bar for doing costly work, like remodeling a kitchen or adding a new bathroom. Your tastes aren’t guaranteed to appeal to potential buyers, meaning they won’t necessarily be willing to pay lots more.

“Unless you have objectively excellent taste or can remove your personal preferences from the process and focus only on timeless, enduring style, I do not advise sellers to invest in a major renovation,” said Kate Wollman-Mahan, a real-estate agent at Coldwell Banker Warburg in New York.

Adding an upscale primary suite to a house costs $339,513 on average, but only adds $81,042 to the resale value, recouping 24% of the cost, according to Zonda. Remodeling an upscale kitchen costs $158,530 on average, but adds $60,176 to the resale value, recovering 38% of the cost.

Instead, think smaller. Refresh an old room with new cabinet pulls or more modern light fixtures. Reglaze a bathtub. Replace old toilet seats and shower rods.

Jennifer Roberts, a real-estate broker at Coldwell Banker Warburg in New York, said she once had trouble selling an apartment with red kitchen cabinets. After she had the seller paint them white, the home went quickly.

It is also tough to make the math work on major exterior projects. A metal roof replacement costs $49,928 on average, but adds $24,034 to the resale value, recovering 48% of the cost, according to Zonda.

Low-cost, big payoff

Painting the walls and pulling up old carpets can freshen the house, even if the finishes are dated. Decluttering the spaces, washing windows and treating lingering smells all help the house to show better.

“I watched a home priced under a million languish on the market with another agent,” said Benjamin Dixon, a real-estate broker at Douglas Elliman in New York. “We came in and decluttered, painted, cleaned and staged, investing a total of under $20,000 and had multiple offers and sold the home for $1,050,000 in just a few weeks.”

In today’s digital age, it’s tempting to rely on automated tools for everything — including figuring out how much your house is worth. But be careful. The automated estimates you’re seeing online often miss key details that affect the true market value of your home.

Before you toss a for sale sign in your yard and expect to bring in the number you saw for your house online, you need to understand why these tools generally aren’t spot-on and why working with an expert real estate agent is the best way to get an accurate picture of what your house is really worth.

The Myth: Online Home Value Estimates Are Accurate

Online home valuation tools give you an approximate value for your house based on the data that’s publicly available for your home. While this can give you a rough starting point, the keyword here is rough. As an article from Ramsey Solutions says:

“Online Home Value Estimators Aren’t 100% Accurate . . . The estimates are only as reliable as the amount of public record data the real estate websites can access. The less data gathered for your particular neighborhood, county and state, the less you can depend on this number.”

The Reality: Online Estimates Miss Key Factors

Here’s the biggest issue with online estimates: they don’t take into account the unique aspects of your home or your local market. And that’s why an agent’s expertise can make such a difference when figuring out what your house is really worth. Here’s an example. A real estate agent will also factor in:

The Home’s Condition: Online tools can’t tell whether your home has been well-maintained or if it needs significant repairs. The condition of your house plays a huge role in its value, and only an in-person walk-through can account for that.

The Latest Neighborhood Trends: Is your neighborhood up-and-coming? Are there new developments or amenities nearby that make your home more desirable? Automated tools often overlook local trends that can significantly affect the value of your home.

Accurate Comparable Sales: While online estimates may use past sales data as a baseline, they don’t always reflect the most recent or most relevant comparable sales, or comps. Real estate agents, on the other hand, have access to up-to-date market data and can give you a much more accurate estimate based on real-time sales in your area.

Agents have a deep understanding of the local market, and they can provide insights that automated tools simply can’t match. As Bankrate explains:

“Online estimation tools determine pricing using algorithms that rely on publicly available information. These algorithms can vary widely from one tool to the next and typically don’t account for a home’s current condition or any upgrades or renovations that are not reflected in public records. So they are not as accurate as in-person methods, like a real estate agent’s comparative market analysis . . .”

Bottom Line

While online home value estimates can be a helpful tool to get a rough idea of what your home is worth, they aren’t foolproof. The true value of your home depends on a range of factors that automated tools just can’t account for.

To get the most accurate estimate, give me a call. That way you have expert guidance and up-to-date market insights to set the best possible price for your home.

Thinking about upgrading your property in the new year? Since the housing market is expected to remain competitive, it’s more important than ever to consider improvements.

Read on for tips to elevate your quality of living and your home’s desirability.

1. Revamp Your Kitchen

A well-designed kitchen remains a surefire way to add value. Kitchen improvements can yield a 70 to 80% return on investment when it’s time to sell. Consider replacing old countertops with quartz or granite, updating appliances and refacing cabinetry. Even smaller upgrades like a modern backsplash can deliver great visual impact.

2. Renovate Bathrooms

Remodeled bathrooms are another biggie on a buyer’s wish list. If you go the total renovation route, think about incorporating the latest trends, such as luxurious finishes and spa-like walk-in showers. More affordable options include replacing faucet fixtures, retiling the shower or upgrading lighting.

3. Update Flooring

Outdated flooring is an eyesore for potential buyers. Replace older carpeting or tile with hardwood, engineered wood or luxury vinyl planks. Look for durable, low-maintenance options in neutral tones that will hold their value for many years to come.

4. Extend Living Space With Outdoor Amenities

Outdoor living continues to be a popular choice for increasing your property’s appeal. Whether you take on a DIY project or hire a contractor, adding a patio or deck will extend your living space. Other sought-after amenities include built-in grills, fire pits, pergolas – and for the ultimate upgrade, an outdoor kitchen.

5. Get Smart With New Technology

It’s never been easier or more affordable to incorporate smart technology into your home. Choose from a variety of upgrades that include tech-advanced thermostats, lighting, video doorbells and security systems. These devices provide comfort, peace of mind and can be easily controlled remotely through apps.

6. Invest in Energy Efficiency

Make your home more energy efficient, which not only boosts your property’s appeal but also reduces your bills over the long haul. Consider updating appliances like refrigerators, washers and HVAC systems that meet Energy Star® standards. Other ideas include improving insulation, adding solar panels or replacing old drafty windows.

7. Modernize Your Lighting

Well-placed lighting enhances your property’s ambiance and functionality. Replace outdated fixtures like fluorescent box-style lights or those that don’t provide adequate lighting. Other updates include recessed lighting, dimmers on switches, pendant lights and wall sconces. As a statement piece, consider adding a high-quality fixture above your island or in your main living space.

Enhancing your home’s worth doesn’t require dramatic changes. Whether you’re selling soon or simply want to enjoy a more modern and efficient dwelling, these practical tips will ensure your property remains marketable. Connect with a local real estate professional to learn more.

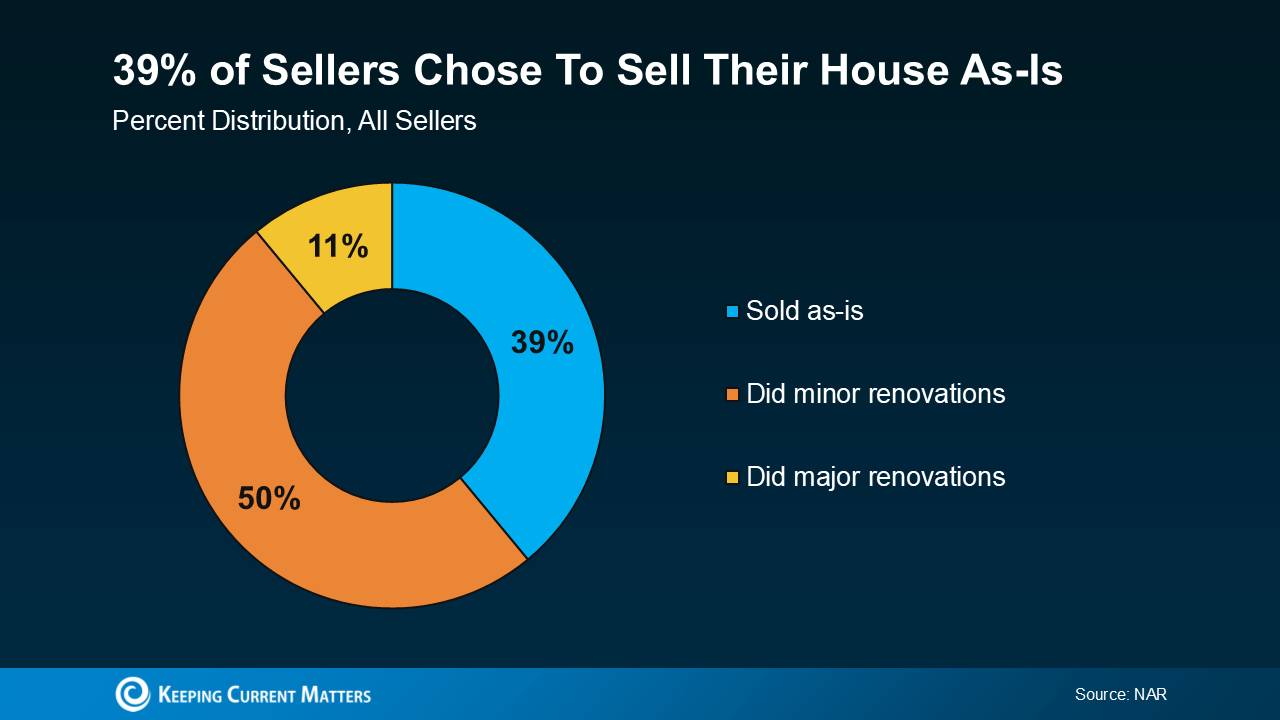

A recent study from the National Association of Realtors (NAR) shows most sellers (61%) completed at least minor repairs when selling their house. But sometimes life gets in the way and that’s just not possible. Maybe that’s why, 39% of sellers chose to sell as-is instead (see chart below):

If you’re feeling stressed because you don’t have the time, budget, or resources to tackle any repairs or updates, you may be tempted to sell your house as-is, too. But before you decide to go this route, here’s what you need to know.

What Does Selling As-Is Really Mean?

Selling as-is means you won’t make any repairs before the sale, and you won’t negotiate fixes after a buyer’s inspection. And this sends a signal to potential buyers that what they see is what they get.

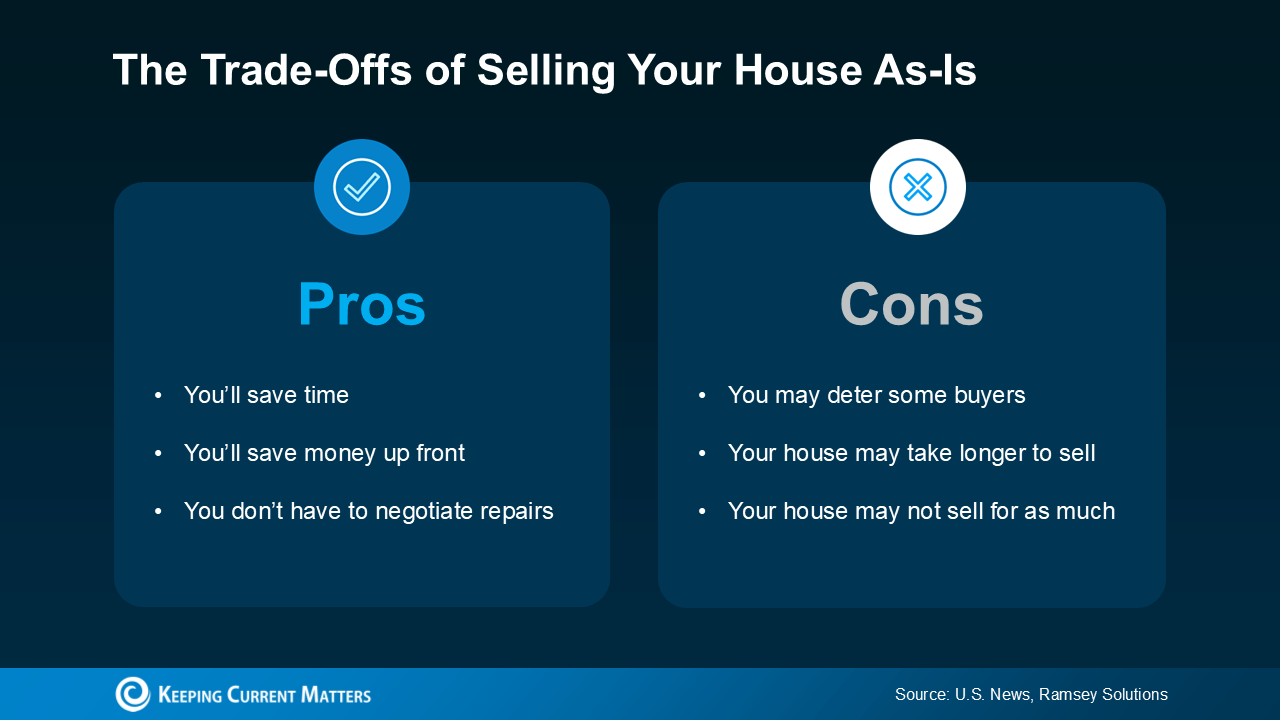

If you’re eager to sell but money or time is tight, this can be a relief because it’s that much less you’ll have to worry about. But there are a few trade-offs you’ll have to be willing to make. This visual breaks down some of the pros and cons:

Typically, a home that’s updated sells for more because buyers are often willing to pay a premium for something that’s move-in ready. That’s why you may find not as many buyers will look at your house if you sell it in its current condition. And less interest from buyers could mean fewer offers, taking longer to sell, and ultimately, a lower price. Basically, while it’s easier for you, the final sale price might be less than you’d get if you invested in repairs and upgrades.

That doesn’t mean your house won’t sell – it just means it may not sell for as much as it would in top condition.

Here’s the good news though. In today’s market, as many as 56% of buyers surveyed would be willing to buy a home that needs some work. That’s because affordability is still a challenge, and while there are more homes for sale right now, inventory is lower than the norm. So, you might find there are a few more buyers who may be willing to take on the work themselves.

How an Agent Can Help

So, how do you make sure you’re making the right decision for your move? The key is working with a pro.

A good agent will help you weigh your options by showing you what comparable homes in your area have sold for, what updates your neighbors are making, and guide you in setting a fair price no matter what you decide. That helps you anticipate what your house may sell for either way – and that can be a key factor in your final decision.

Once you’ve picked which route you’re going to go and the asking price is set, your agent will market your house to maximize its appeal. And if you decide to sell as-is, they’ll call attention to the best features, like the location, size, and more, so it’s easy for buyers to see the potential, not just projects.

Bottom Line

Selling a home without making any repairs is possible in today’s market, but it does have some trade-offs. To make sure you’re considering all your options and making the best choice possible, have a conversation with a local agent.

California is a coveted place to live due to its temperate climate and variety of geography, from mountains to deserts and a mix of big cities and suburbs.

The consequence of being a desirable place to live is that housing prices are often higher here than in other parts of the country.

While California’s notoriously high-priced real estate market has faced challenges recently, 2025 is shaping up as a promising year for buyers, especially in high-demand areas, Clarke said.

She pointed to the California Association of Realtors’ (CAR) 2025 California Housing Market Forecast, which suggests that single-family home sales are expected to increase by 10.5% to 304,400 units.

As mortgage rates are anticipated to ease, potential buyers previously priced out could find a more favorable environment, Clarke said.

Improving Interest Rates and Market Access

In 2025, the anticipated decrease in interest rates is expected to enhance the housing market by creating a more favorable borrowing environment, Clarke said. She noted that CAR projects that the average 30-year mortgage rate will decline from 6.6% in 2024 to 5.9% in 2025, which could help increase affordability and allow more buyers to enter the market.

“Lower interest rates are beneficial even for my discerning cash buyers who are generally less affected by financing costs as they tend to energize the overall housing market,” Clarke said.

With more buyers active, property values will strengthen, and appreciation can accelerate, supporting long-term equity growth for all buyers, including those purchasing without financing.

Stable Market Conditions With Modest Price Growth

While home prices will continue to rise, they are expected to do so at a slower pace than in the last few years, Clarke said, so getting in now will be better than waiting a few years. A projected 4.6% increase in median home prices reflects this steady but manageable growth, she shared.

Unlike the rapid price hikes of recent years, this gradual appreciation rate can offer buyers more predictable investment returns, she explained.

“The balance of stable price growth and increased inventory gives buyers an edge, especially in markets that are becoming less overheated,” she said.

Market Resilience in Luxury Segments Is Good for Everyone

While the average buyer is not looking to buy luxury homes, when these markets improve, this can be good for the housing market as a whole, she said.

“Santa Barbara and other coastal and affluent areas like nearby Newport Beach attract a high percentage of cash buyers who are less influenced by interest rate changes. This dynamic helps stabilize the luxury market in these areas, creating a more resilient investment environment,” she said.

Movement in High-Demand California Markets

While Santa Barbara is a strong market for its coastal appeal and high-quality amenities, other California regions also show promising investment potential in 2025, Clarke shared.

Bay Area suburbs: Markets like Walnut Creek, Orinda and Mill Valley are seeing an uptick in interest from buyers seeking more space while remaining close to Silicon Valley and San Francisco, Clarke said.

Sacramento region: As a more affordable alternative to the Bay Area, Sacramento continues to attract families and professionals who value proximity to Northern California’s job centers. Clarke said increased inventory here may allow for greater flexibility and pricing opportunities.

Southern California inland markets: Inland Empire cities such as Riverside and Rancho Cucamonga have become popular among buyers priced out of Los Angeles, offering a suburban lifestyle at a lower price point. This region is forecast to benefit from moderate price appreciation and increasing demand.

A Buyer-Friendly Inventory Landscape

Clarke feels confident that 2025 will see a healthier inventory, as lower rates will likely push more homeowners to list their properties, easing the lock-in effect.

“With CAR predicting an increase of active listings by over 10%, prospective buyers will encounter a more balanced market where they can negotiate more freely and potentially avoid the intense bidding wars of recent years,” Clarke said.

Long-Term Investment Potential and Equity Growth

For buyers looking at the long game, investing in California real estate remains a sound strategy, Clarke said. Even modest appreciation in high-demand areas can translate into significant equity gains over time.

“By purchasing in 2025, buyers have the potential to lock in properties at competitive prices and enjoy appreciation as demand remains strong, driven by limited inventory and continued desirability,” Clarke said.

While affordability challenges persist, particularly in regions with limited supply, inventory increases and stabilized interest rates make this a promising year for buyers ready to make their moves, Clarke said.

The average single-family home in America costs $420,000. If home prices had simply kept pace with inflation since 1963, that home would cost just $185,000.

Regulations and other costs buyers bear add more than $90,000 to the price of a new home.

And supply is not meeting nationwide demand. America must build as many as 7.2 million new homes just to meet that demand, and the vast majority of them must be priced below $400,000.

The question of housing affordability has recently centered on real estate commissions. This is not the foremost factor affecting affordability. As a community, we need to address the issue head-on, in a way that does not compromise consumer protections like the ability for buyers to have their own agents.

If policymakers want to improve housing affordability, they must start by focusing on solutions that increase the housing supply. Doing that means taking steps to ease restrictions on buildable land, cutting red tape, and providing incentives such as tax credits to help builders build more homes faster than ever.

America must build as many as 7.2 million new homes just to meet that demand, and the vast majority of them must be priced below $400,000.

(Realtor.com)

Realtor.com® will work with our communities, economists, business leaders, leaders of housing and building associations, and, of course, leaders of government, to highlight the housing supply shortages we have in every state, as well as pragmatic solutions to solve this problem.

On behalf of those buyers who are price-locked out of the market, the real estate professionals who support them, and the homebuilders building more affordable homes, help us restore homeownership for all.

At Realtor.com, we’re for real solutions.

We hope that you’ll be part of them.

With the 2024 Presidential election fast approaching, you might be wondering what impact, if any, it’s having on the housing market. Let’s break it down.

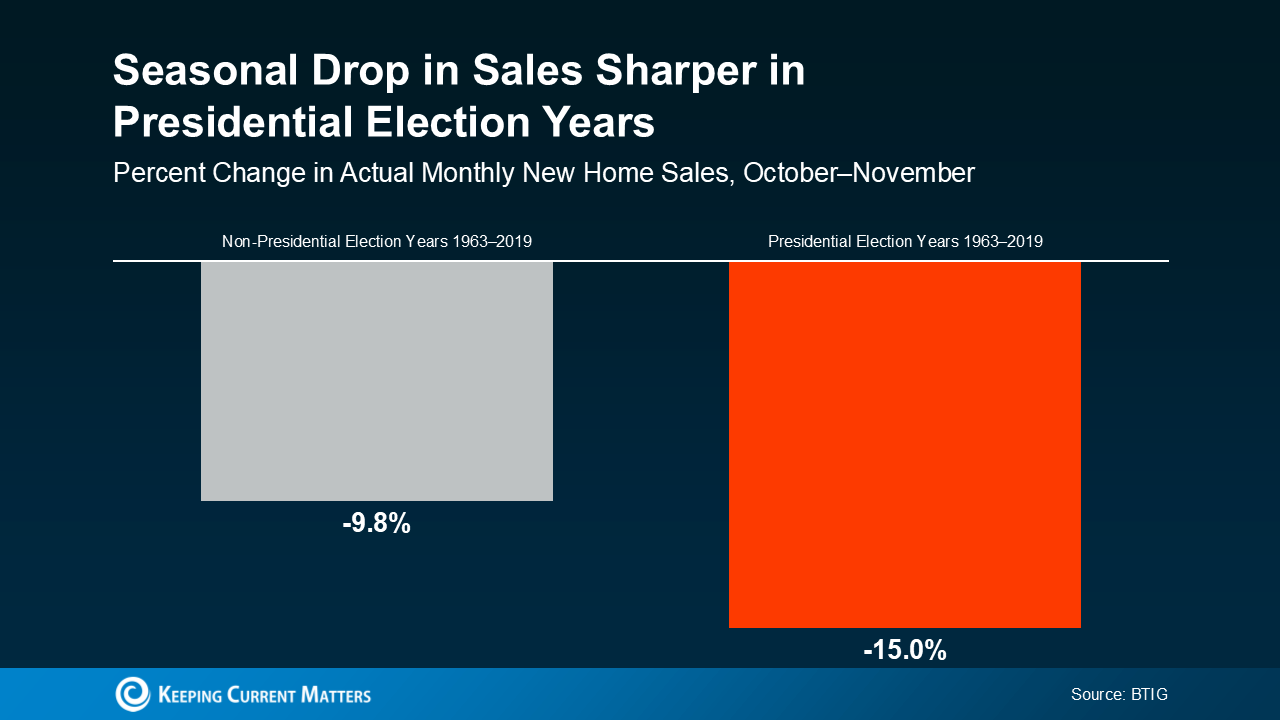

Election Years Bring a Temporary Slowdown

In any given year, home sales slow down slightly in the fall. It’s a typical, seasonal trend. However, according to data from BTIG, in election years there’s usually a slightly larger dip in home sales in the month leading up to Election Day (see graph below):

Why? Uncertainty. Many consumers hold off on making major decisions or purchases while they wait to see how the election will play out. It’s a pattern that’s shown up time and time again, and it’s particularly apparent for buyers and sellers in the housing market.

This year is no different. A recent survey from Redfin found that 23% of potential first-time homebuyers said they’re waiting until after the election to buy. That’s nearly a quarter of first-time buyers hitting the pause button, likely due to the same feelings of uncertainty.

Home Sales Bounce Back After the Election

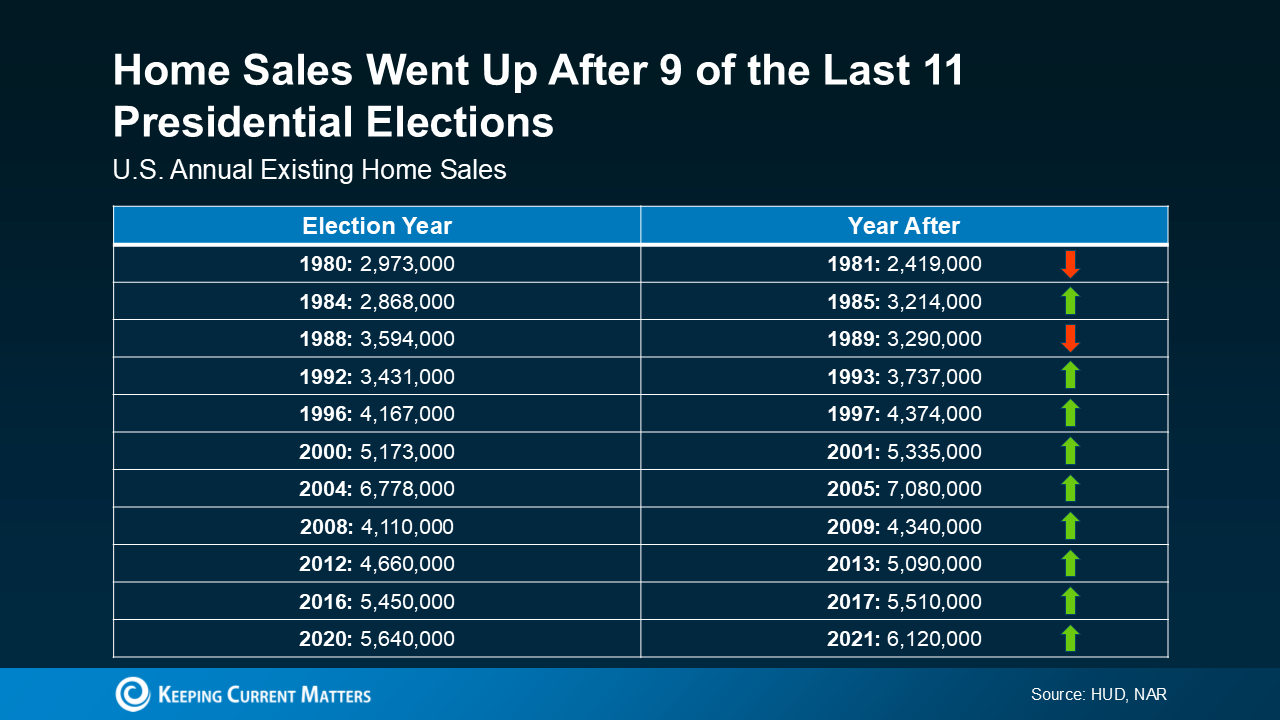

The good news is these delayed sales aren’t lost forever—they’re just postponed. History shows sales tend to rebound after the election is over. In fact, home sales have actually increased 82% of the time in the year after the election (see chart below):

That’s because once the election dust settles, buyers and sellers have a sense of what’s ahead and generally feel more confident moving forward with their decisions. And that leads to a boost in home sales.

What To Expect in 2025

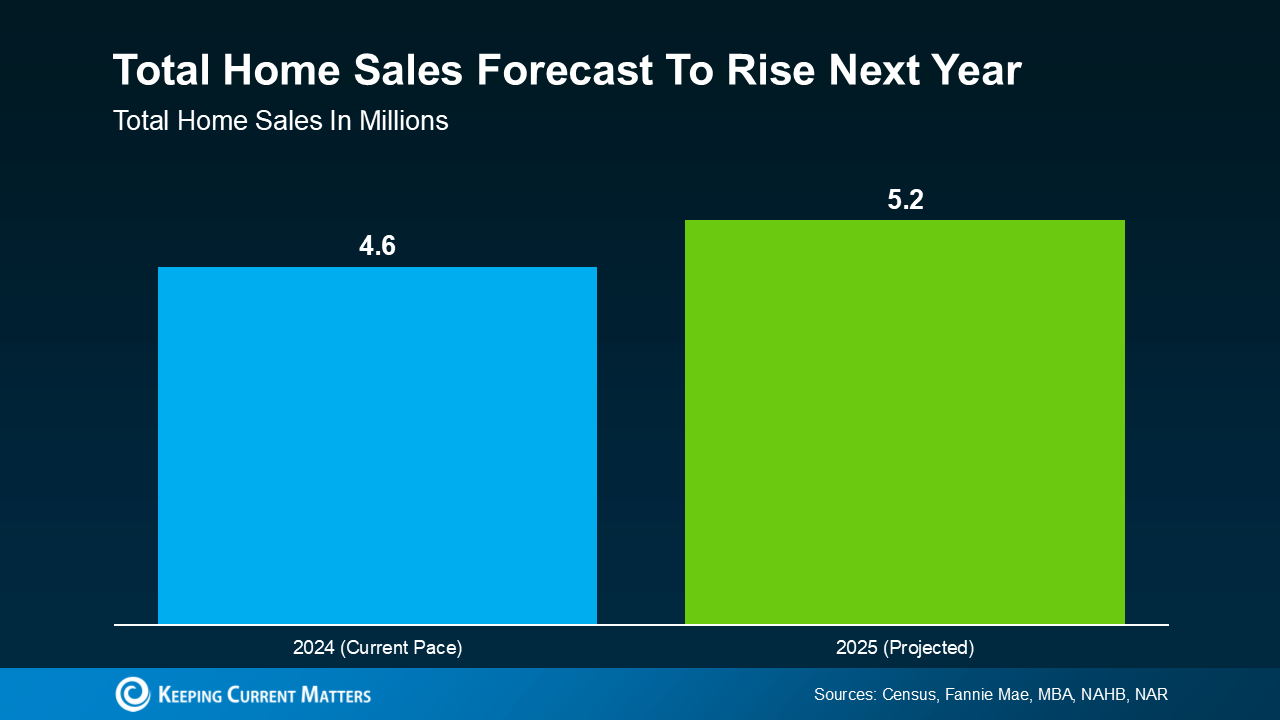

If history is any indicator, that means more homes will sell next year. And based on the latest forecasts, that’s exactly what you should expect. As the graph below shows, the housing market is on pace to sell a total of 4.6 million homes this year, and projections are for 5.2 million total sales next year (see graph below):

And that aligns with the typical pattern of post-election rebounds.

So, while it might feel like the market is slowing down right now, it’s more of a temporary dip rather than a long-term trend. As has been the case before, once the election uncertainty passes, buyers and sellers will return to the market.

Bottom Line

It’s important to remember that while election years often bring a short-term slowdown in the housing market, the pause is usually temporary. Those sales are not lost. Data shows home sales typically increase the year after a Presidential election, and current forecasts indicate 2025 will be no different. If you’re waiting for a clearer picture before making a move, just know that the market is expected to pick up speed in the months ahead.

You may have heard chatter recently about the economy and talk about a possible recession. It’s no surprise that kind of noise gets some people worried about a housing market crash. Maybe you’re one of them. But here’s the good news – there’s no need to panic. The housing market is not set up for a crash right now.

“A housing market crash happens when home values plummet due to a lack of demand for homes or an oversupply.”

With that definition in mind, here are two reasons why this just isn’t on the horizon.

1. Demand for Homes Is Higher than Supply

One of the biggest reasons the housing market crashed back in 2008 was an oversupply of homes. Today, though, it’s a very different story.

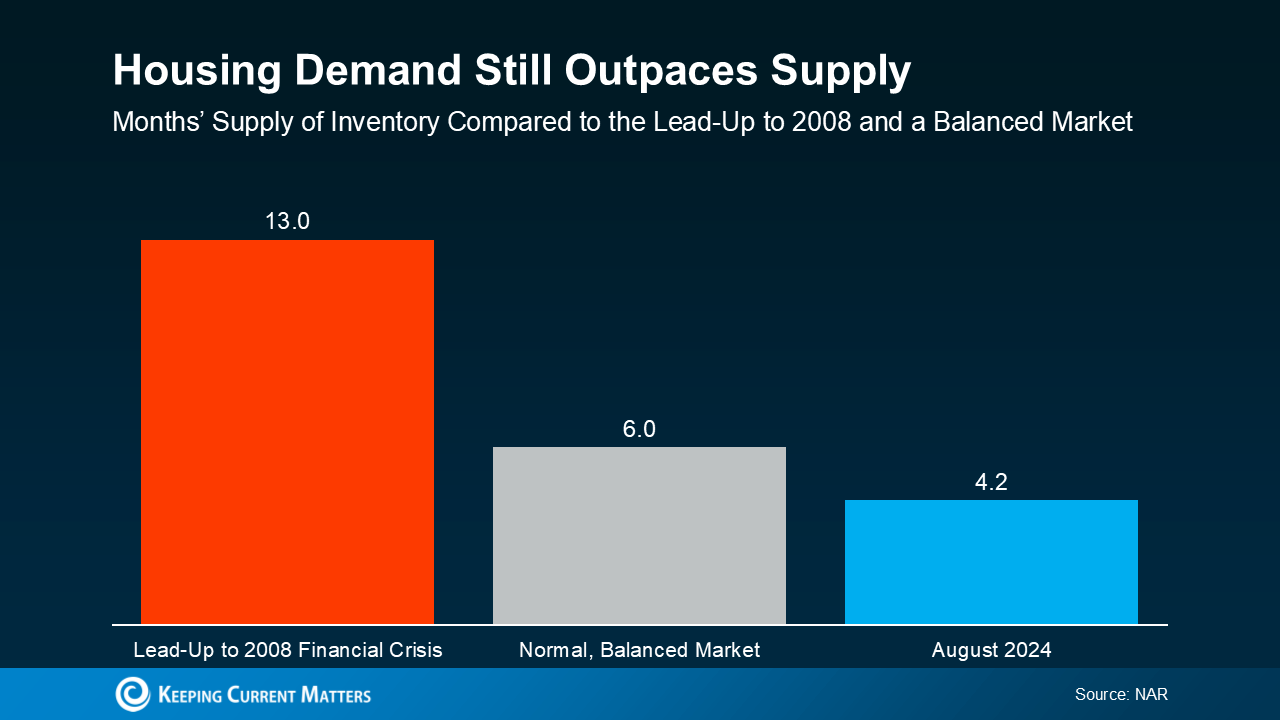

It’s a general rule of thumb that a market where supply and demand are balanced has a six-month supply of homes. A higher number means supply outpaces demand, and a lower number means demand outpaces supply. The graph below uses data from NAR to put today’s situation into context:

The graph compares housing supply during three different periods of time. The red bar shows there were 13 months of supply before the 2008 crisis, which was far too much. The gray bar shows a balanced market with six months of supply, for context. And the blue bar shows there are only 4.2 months of supply today.

Put simply, there are more people who want to buy homes than there are homes available to buy right now. So, demand is greater than supply. When that happens, home prices stay steady or rise – the opposite of a housing market crash.

It’s important to note that inventory levels differ from market to market. Some areas may be more balanced, while a few could have a slight oversupply, which can impact prices locally. However, most markets continue to experience a shortage of homes.

Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“We simply don’t have enough inventory. Will some markets see a price decline? Yes. [But] with the supply not being there, the repeat of a 30 percent price decline is highly, highly unlikely.”

2. Unemployment Is Still Low

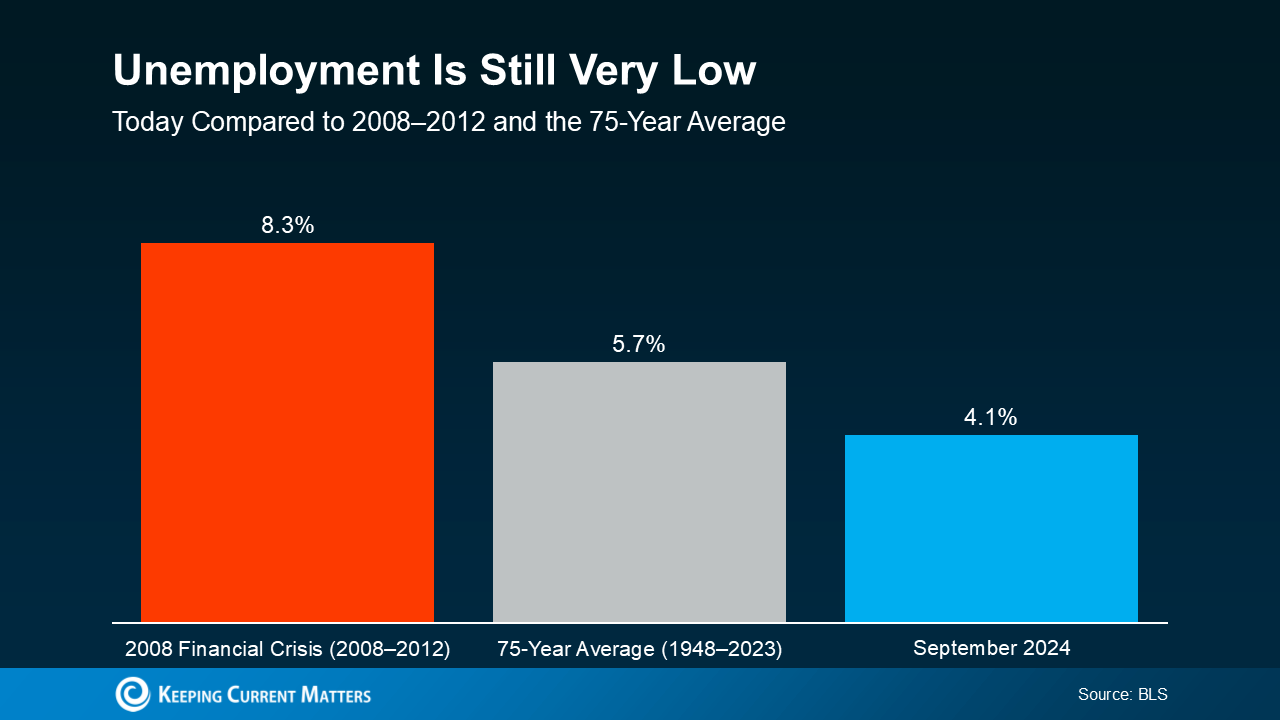

When people are unemployed, they’re more likely to have trouble making their mortgage payments and may be forced to sell or face foreclosure. That was a big problem during the 2008 financial crisis. Today, the employment situation is much more stable (see graph below):

Again, this graph shows three different periods of time, but this one is the unemployment rate. The red bar represents the 2008 financial crisis when unemployment was very high at 8.3%. The gray bar shows the 75-year average of 5.7%. And the blue bar shows the unemployment rate today, and it’s much lower at just 4.1%.

Right now, people are working, earning an income, and making their mortgage payments. That’s one reason why the wave of foreclosures that happened in 2008 isn’t going to happen again this time. Plus, since so many people are employed right now, many are actually in a position to buy a home, and this demand keeps upward pressure on prices.

Today’s Housing Market Is Stronger than in 2008

While it’s understandable to be concerned when you hear talk of a recession and economic uncertainty, but know this: the housing market is in a much better place than it was in 2008. According to Rick Sharga, Founder and CEO at CJ Patrick Company:

“Literally everything is different about today’s housing market dynamics than the conditions that led to the housing crisis.”

Demand for homes still outpaces supply, and unemployment remains low. And these are two key factors that will help prevent the housing market from crashing any time soon.

Bottom Line

The housing market is in a much better place than it was in 2008, but it’s important to remember that real estate is very local.

So, it’s always a good idea to stay informed about your specific market. If you have any questions or want to discuss how these factors are playing out in your area, reach out to a local real estate agent.