Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Contemplating the purchase of a home or diligently saving for a down payment? The recent surge in mortgage rates may have prompted a crucial question in your mind: Is now the best moment to invest in a home, or should you bide your time until mortgage rates go down?

In order to assist you in making an informed decision that aligns with your family’s best interests, let’s dive into the financial aspects—without any intimidating mathematical complexities. Together, we’ll explore whether the current circumstances favor your home-buying endeavors or if it might be prudent to defer this decision for a more favorable period.

Let’s take a look at what financial Guru Dave Ramsey had to say about this question:

Should I Buy a House Now or Wait?

Yes, you should buy a house now if you’re financially ready to do so. Here are the biggest reasons why that’s the best move:

- If interest rates continue to drop, then house prices will start going up. Lots of folks haven’t been able to afford a house because of high interest rates, so they’ve been sitting and waiting. As rates keep getting lower, more and more of those people will start buying homes—and sellers will be able to raise their prices because of that increase in demand.

- You can always refinance down the road. If you buy now and interest rates continue dropping over the next year or two, you can still take advantage of the lower rates by refinancing your mortgage. On the other hand, if you wait to buy and home prices go up, you’re stuck with the higher prices.

- Mortgage interest rates may be high right now, but they’ve already begun to drop. That means, if you buy now, you’ll already be getting a better deal than you would have in 2023.

- The Federal Reserve (also known as the Fed) is unpredictable. We never know exactly what the Fed will decide to do with the federal funds rate, which directly impacts mortgage rates across the country (more on that later).

Here’s the deal, though: You should only buy a house if you’re prepared financially. How do you know if you’re financially ready to buy a house? Let’s break it down.

Am I Prepared Financially to Buy a House?

If you’ve checked these four boxes, you’re in the clear to buy a house!

- You’ve paid off your debt. Focus on paying off all your consumer debt before you buy a house. Getting rid of student loans, credit card payments and car notes will give you more margin in your budget—and that’s super important as a homeowner.

- You have a full emergency fund. Saving up an emergency fund of 3–6 months of your typical expenses before you buy will be the difference in whether a broken HVAC unit, fridge or washing machine is a catastrophe or merely an inconvenience.

- You’ve saved a strong down payment. If you’re a first-time home buyer, you need a down payment of at least 5–10%. But if you can swing a 20% down payment, that’s even better. Why? Putting 20% down will keep you from having to pay for private mortgage insurance (PMI), an extra monthly fee that could add hundreds to your house payment.

- You can afford the house payment. Don’t buy a house if the monthly payment (including principal, interest, homeowners insurance and HOA fees) on a 15-year fixed-rate mortgage would be more than 25% of your take-home pay. Any more than that, and you run the risk of not having enough money left in your budget each month to put toward other important financial goals—aka, you’ll be house poor.

If you haven’t checked one or more of those boxes, that’s where you need to direct your focus for now. We know how badly you want to be a homeowner and start building equity. But we talk to people every day who bought a house before taking those steps and wound up regretting it because they got stuck with a giant, expensive burden.

Will Mortgage Rates Go Down in 2024?

Yes, mortgage rates are expected go down in 2024. Average U.S. rates for both 30-year and 15-year fixed-rate mortgages began steadily dropping in November 2023, and that trend continued into January 2024.2 Rates will likely keep going down throughout the rest of the year, especially since the Fed projected that it will lower the federal funds rate three times in 2024.3

But even as mortgage rates continue to go down in 2024, odds are the drop won’t be drastic—it’s not like rates are going to quickly return to the 2–3% range we saw at the end of 2021. The bottom’s not about to fall out here.

For example, even though the National Association of REALTORS® believes rates will go down in 2024, they’re only predicting a 1.2% drop (from 7.5% to 6.3% for 30-year mortgages) by the end of the year.4 A lower rate is definitely nice, but that small of a drop would only save you a couple hundred bucks on your monthly payment, if that.

It’s a discount, sure, but it’s not worth waiting around for—especially since, like we talked about earlier, you can refinance down the road.

How Do Federal Interest Rate Hikes Affect Mortgages for Home Buyers?

When interest rates go up in the real estate world, so do monthly payments and the total amount of interest you’ll pay on a mortgage. How much? Here’s an example.

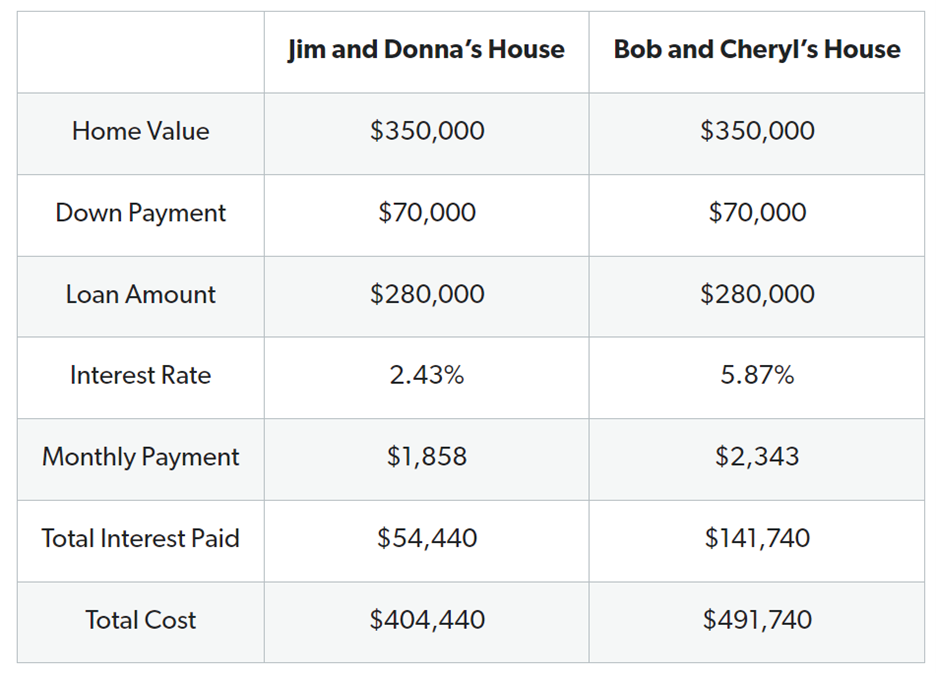

Let’s say we have two couples who each bought $350,000 houses with 20% down and 15-year fixed-rate mortgages. Couple #1, Jim and Donna, bought their house in January 2022 when the typical interest rate was around 2.4%. Couple #2, Bob and Cheryl, bought their house less than two years later in January 2024—when the average rate was nearly 5.9%.5

We used our Mortgage Calculator to see what both couples will pay for their houses. To keep things simple, we left out costs for property taxes, homeowners insurance, and homeowners association (HOA) fees.

Bob and Cheryl will pay over $90,000 more in interest than Jim and Donna—even though their home value and loan terms are the same. Plus, Bob and Cheryl’s house payment is over $500 more per month. Ouch!

What Is the Federal Reserve?

Okay, we’ve mentioned the Fed a couple of times and talked about how interest rate hikes can affect you. But what is the Fed anyway?

Well, the Federal Reserve is the U.S. central bank that creates money and sets interest rates. Its main goal is to keep the economy running smoothly by having low unemployment and low inflation.

The Fed is kind of like a mechanic who tinkers around with a car to make it purr like a kitten, and one of its favorite tools is (shocker) interest rates.

Why Does the Fed Raise Interest Rates?

The Fed raises interest rates to encourage people to borrow less, spend less and save more—which should slow down inflation.

Now, the Fed doesn’t tell commercial banks what interest rates to charge on loans, but they do influence the banks’ rates by setting their federal funds rate. The fed funds rate is the interest rate banks charge to each other for overnight loans, and it influences most other interest rates.

So, even though the Federal Reserve doesn’t actually set mortgage interest rates, its decisions can still affect your mortgage. For example, mortgage rates went up in early 2022—even before the Fed started raising rates. That’s because banks saw what was coming and started upping interest rates to protect their profits.

The Bottom Line

No one likes it when interest rates go up, but it’s not the end of the world. This is still a great time to buy a house—you’ll just pay more than you would’ve a couple years ago. It’s also a good time to sell a house. And if you already have a fixed-rate mortgage locked in, you’re in good shape too.

While it’s smart to get the lowest possible interest rate on your mortgage, that doesn’t mean you have to wait years to buy or sell a house—or to refinance if your current loan just isn’t working for you. You get to decide when to buy a house based on what’s right for you and your family, not what the Fed is doing.

Frequently Asked Questions

Will the Fed raise interest rates again?