Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Do You Think the Housing Market’s About To Crash? Read This First

Lately, it feels like a lot of people have been asking the same question: “Is the housing market about to crash?”

If you’ve been scrolling through social media or watching the news, you might have seen some pretty scary headlines yourself. That’s why it’s no surprise that, according to data from Clever Real Estate, 70% of Americans are worried about a housing crash in 2025.

But before you hit pause on your plans to buy or sell a home, take a deep breath. The truth is: the housing market isn’t about to crash – it’s just shifting. And that shift actually works in your favor.

Today’s Inventory Keeps the Housing Market from Crashing

Mark Fleming, Chief Economist at First American, says:

“There’s just generally not enough supply. There are more people than housing inventory. It’s Econ 101.”

Think about it. If there’s a shortage of something – like tickets to a popular concert – prices go up. That’s what’s been happening with homes. We still have a shortage of supply. Too many buyers and not enough homes push prices higher.

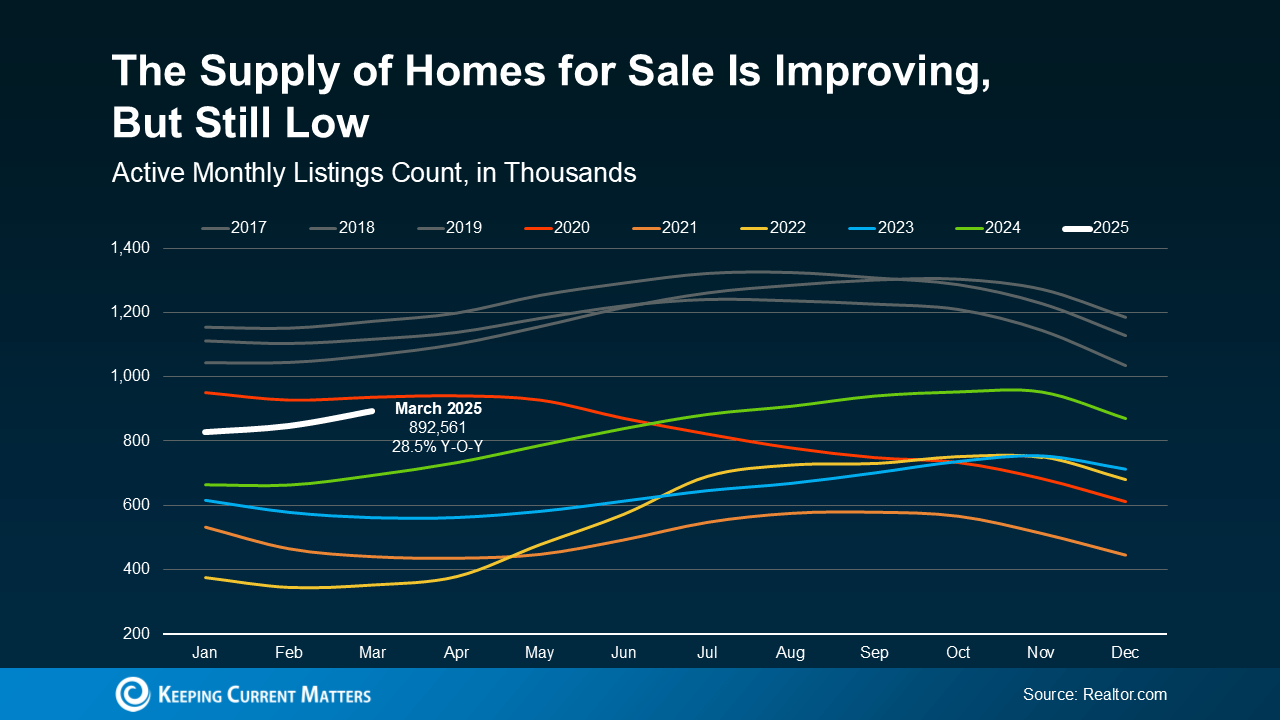

Check out the white line for 2025 in the graph below. Even though the number of homes for sale is climbing, data from Realtor.com shows we’re still well below normal levels (shown in gray):

That ongoing low supply is what’s stopping home prices from dropping at the national level. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“… if there’s a shortage, prices simply cannot crash.”

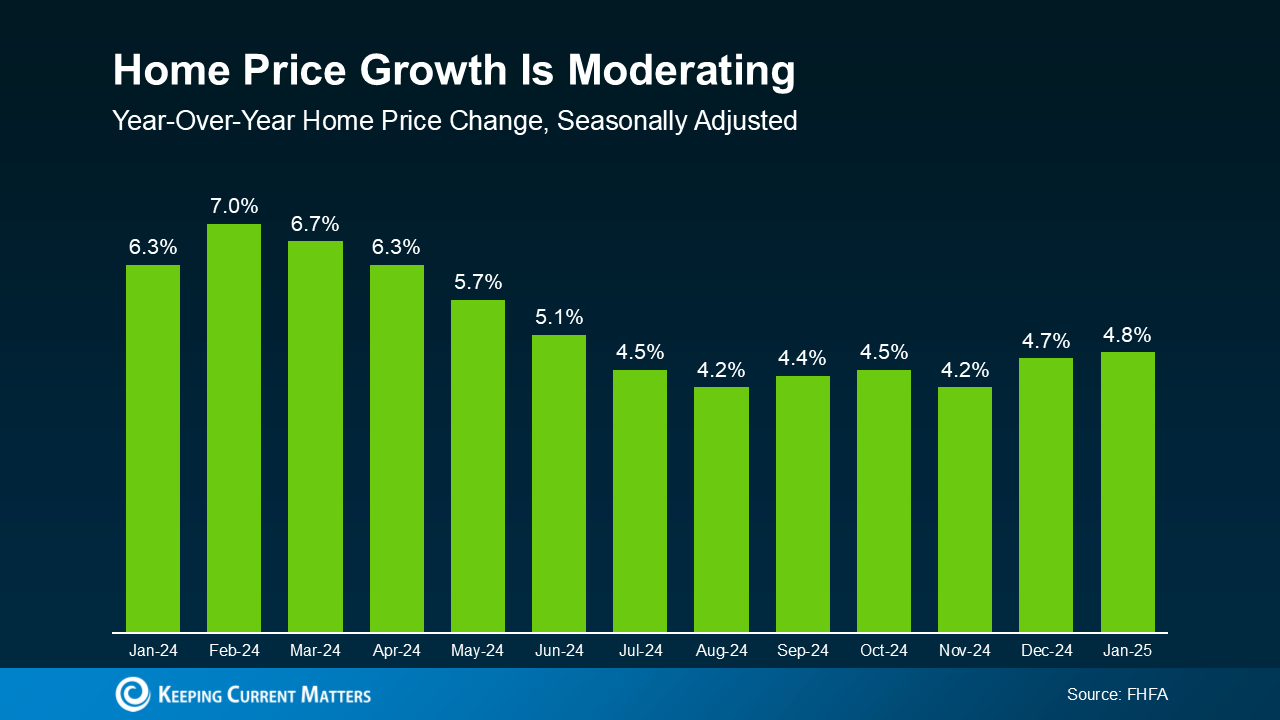

More Homes for Sale Means Price Growth Is Easing

And, as more homes become available, that takes some of the intense upward pressure off home price growth – leading to healthier price appreciation.

So, while prices aren’t falling nationally, growing inventory means they also aren’t rising as fast as they were. What we’re seeing is price moderation (see graph below):

And according to Freddie Mac, that moderation should continue through the rest of this year:

“In 2025, we expect the pace of house price appreciation to moderate from the levels seen in 2024, while still maintaining a positive trajectory.”

Put simply, that means prices will continue going up in most areas, just not as quickly. That’s good news for anyone who’s been having trouble finding a home and feeling sticker shock from the rapid price appreciation of the past few years.

But of course, what’s happening with prices and inventory is going to vary by local market. So, talk to your agent to find out what’s happening where you live.

Bottom Line

Don’t let the talk scare you. Experts agree that a housing market crash is unlikely in 2025. As Business Insider reports:

“. . . economists who study housing market conditions generally do not expect a crash in 2025 or beyond unless the economic outlook changes.”

Instead, we’re heading into a housing market that’s healthier and more balanced, with slower price growth and more opportunity.

Give me a call so we can chat about what’s happening in your local market and how you can make the most of it.

Should I Buy a Home Right Now? Experts Say Prices Are Only Going Up

At one point or another, you’ve probably heard someone say, “Yesterday was the best time to buy a home, but the next best time is today.”

That’s because nationally, home values continue to rise. And with mortgage rates still stubbornly high and home prices going up, you may be holding out for prices to fall or trying to time the market for that perfect rate. But here’s the truth: waiting for the right moment could cost you in the long run.

Home Prices Are Still Rising – Just at a More Normal Pace

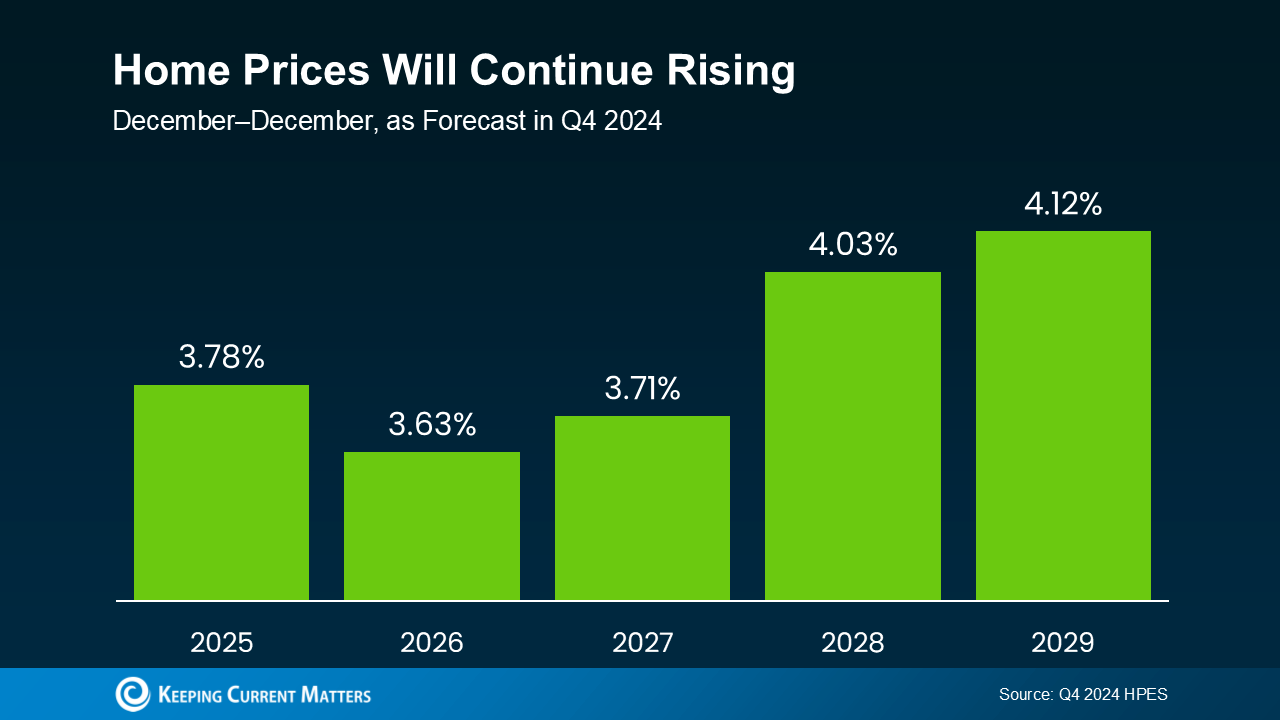

The idea that prices will drop dramatically is wishful thinking in most markets. According to the Home Price Expectations Survey from Fannie Mae, industry analysts are saying prices are projected to keep rising through at least 2029.

While we’re no longer seeing the steep spikes of previous years, experts project a steady and sustainable increase of around 3-4% per year, nationally. And the good news is, this is a much more normal pace – a welcome sign for hopeful buyers (see graph below):

What This Means for You

While it’s tempting to wait it out for prices or mortgage rates to decline before you buy, here’s what you’ll need to consider if you do.

- Tomorrow’s home prices will be higher than today’s. The longer you wait, the more that purchase price will go up.

- Waiting for the perfect mortgage rate or a price drop may backfire. Even if rates dip slightly, rising home prices could still make waiting more expensive overall.

- Buying now means building equity sooner. Home values are rising, which means your investment starts growing as soon as you buy.

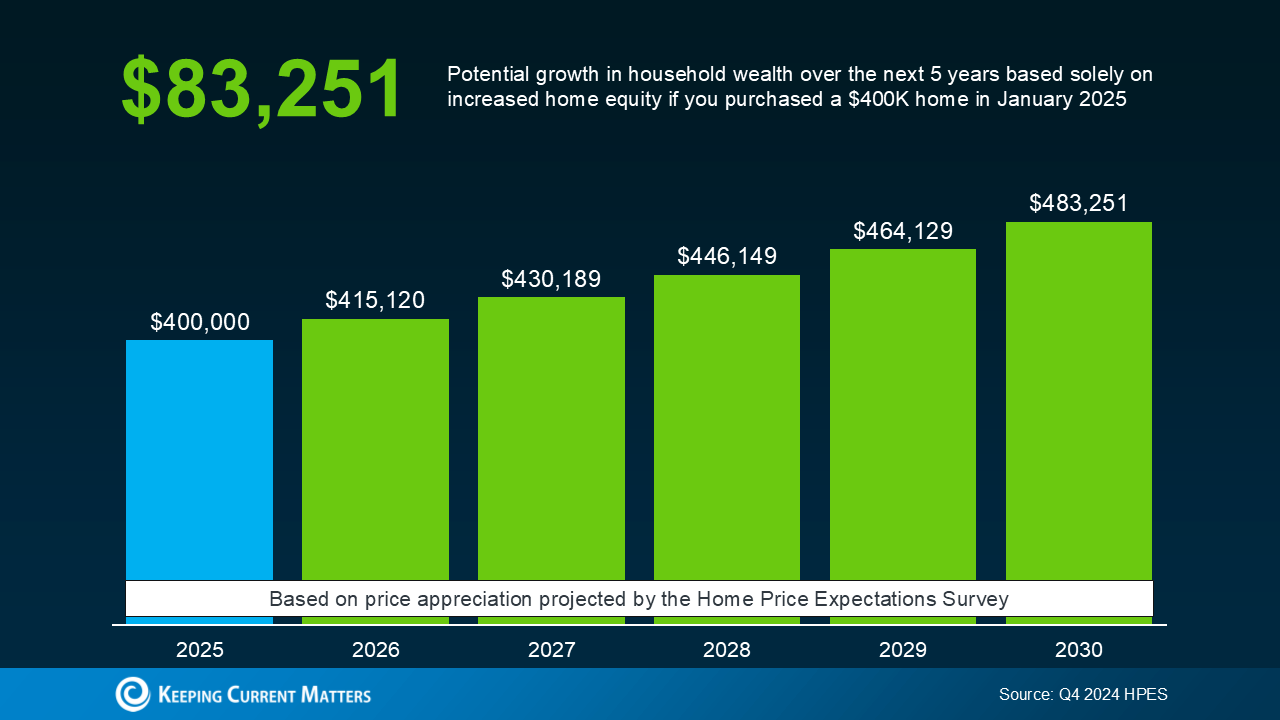

Let’s put real numbers into this equation. If you purchase a $400,000 home today, based on these price forecasts, it’s expected to go up in value by more than $83,000 over the next five years. That’s some serious money back in your pocket instead of being left on the sidelines (see graph below):

Why Aren’t Prices Dropping? It’s All About Supply and Demand

Even though there are more homes for sale right now than there were at this time last year, or even last month, there still aren’t enough of them on the market for all the buyers who want to purchase them. And that puts continued upward pressure on prices. As Redfin puts it:

“Prices will rise at a pace similar to that of the second half of 2024 because we don’t expect there to be enough new inventory to meet demand.”

While every market is different, most areas will continue to see moderate price growth. Some may level off a bit, but a major national drop? Not likely.

Bottom Line

Time in the Market Beats Timing the Market

If you’re debating whether to buy now or wait, remember this: real estate rewards those who get in the market, not those who try to time it perfectly.

Yes, today’s housing market has its challenges, but there are ways to make it work —exploring different neighborhoods, considering smaller condos or townhomes, asking your lender about alternative financing, or tapping into down payment assistance programs. The key is making a move when it makes sense for you rather than waiting for a perfect scenario that may never arrive.

Want to take a look at what’s happening with prices in your local market? Whether you’re ready to buy now or just exploring your options, reach out to a me so you have a plan in place that’ll set you up for success.

The Secret To Selling This Spring: Start the Prep Work Now

Spring is the busiest season in the housing market. It’s the time of year when buyers are most active – that means it’s when homes sell faster and for top dollar. If you’ve already got a move on your mind, why not list this spring and take advantage of the added buyer demand?

Since spring is just around the corner, now’s the time to start getting your house market-ready. You’ve got just over a month to do the prep work. And while that may sound like a decent amount of time, it’s going to go by quickly. And you won’t want to rush through this important task – especially this year.

The Right Repairs Will Matter More This Spring

Right now, two things are true. There are more homes on the market than there have been in years. And buyers are being extra selective. That combination means you need to invest some time and effort in making strategic repairs. And many homeowners already have a jump on this work.

In the 2025 Outlook for Home Remodeling, Carlos Martin, Director of the Remodeling Futures Program at the Joint Center for Housing Studies of Harvard University, explains:

“. . . homeowners are slowly but surely expanding the pace and scope of projects compared to the last couple years.”

And the most common projects they’re tackling are replacing water heaters, HVAC units, and flooring. Energy efficiency is a key consideration too, based on home improvement data from the Census.

What To Prioritize as You Plan Ahead

But just because that’s what other homeowners are doing, it doesn’t mean that’s what you have to tackle. Think about what you’d want to see if you were a buyer. Focus on quick wins that are easy to knock out with the time you have – but, don’t ignore key repairs, especially ones you think could turn off buyers.

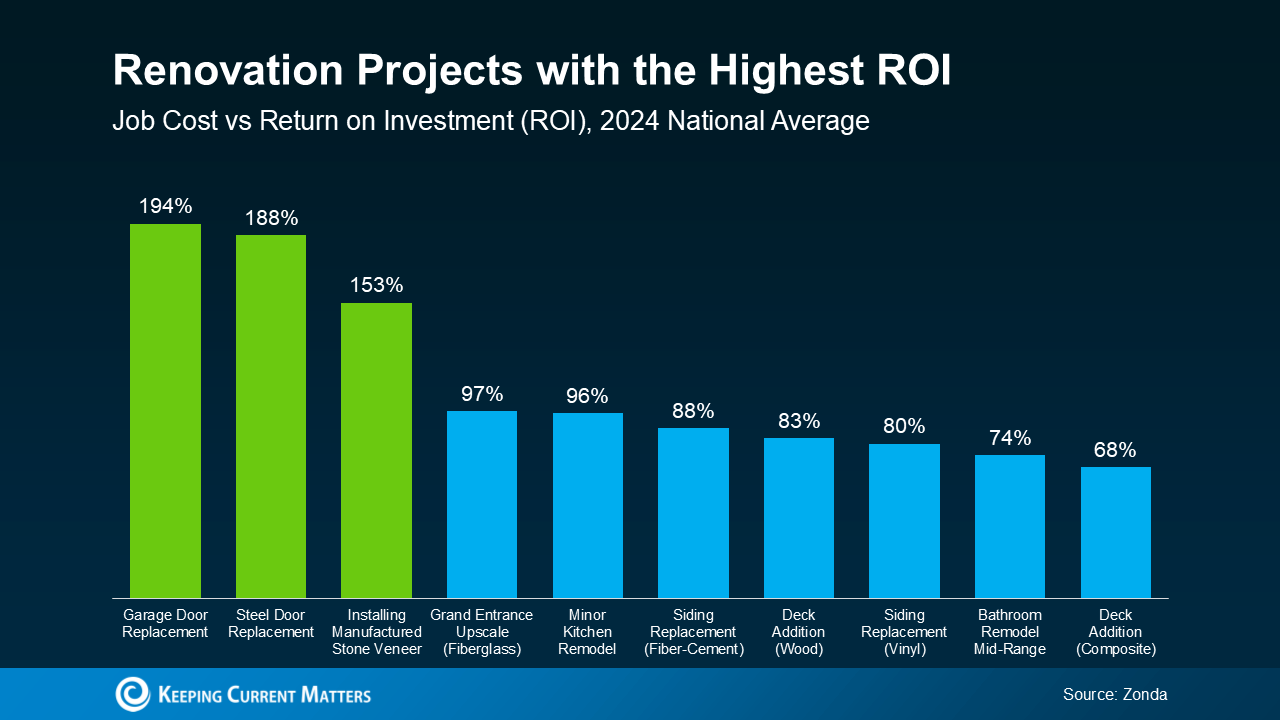

While big-ticket items like replacing an old roof or outdated flooring may seem daunting, they can pay off – especially if you focus on projects with the best return on investment (ROI).

An agent’s expertise is key in narrowing down your list to what’s actually worth it. They know what buyers in your area want and they also have data like this report from Zonda to guide you on which updates have the best ROI (see green in the graph below):

That’s why it’s so important to talk to a local real estate agent before you dive into any repairs. Bankrate puts it best:

“As a seller, it’s smart to be prepared and control whatever factors you’re able to. Things like hiring a great real estate agent and maximizing your home’s online appeal can translate into a smoother sale — and more money in the bank.”

It’s not too early to partner with an agent. By starting now, you’ve still got time to space out the work and find any contractors you need to get the job done. If you wait until spring to roll up your sleeves, you risk running out of time – and that means your house may be overshadowed by others who are more buyer-ready.

Bottom Line

If you’re planning to sell this spring, it’s time to start tackling your to-do list. But, before you get started, connect with an agent. That way you can make sure you’re spending your time and budget on projects that’ll pay off in the long run.

Seller Concessions: A Smart Strategy To Get Your House Sold

For the past few years, it’s been mostly a seller’s market. But dynamics are shifting as the number of homes for sale grows. And that means that the market is balancing out a bit. As a result, some sellers are finding they need to be more flexible to close a deal. One strategy that can help? Offering concessions.

As the National Association of Realtors (NAR) explains:

“As home inventory begins to grow and buyers regain some advantage in the market, sellers may consider offering more in negotiations to make the deal more attractive and get to the closing table.”

What Are Seller Concessions?

Concessions are homebuying costs that a seller agrees to cover as a way to get their house sold. And based on data from the National Association of Realtors (NAR), nearly 1 out of every 4 sellers (24%) offered a concession in 2024. Here are a few of the most common types of concessions:

- Covering Closing Costs: The seller pays for part (or all) of the buyer’s closing costs, like appraisal fees, title insurance, or loan fees.

- Price Adjustments: Instead of making repairs, a seller might lower the purchase price to make up for updates the buyer will need to tackle.

- Adding a Home Warranty: A seller may throw in a home warranty, giving the buyer peace of mind key repairs will be covered in the first year.

And don’t worry. This doesn’t mean you have to come up with more cash to make it happen. These are things that get subtracted from your profits at closing – not more funds you have to bring to the table. And not all concessions are about money.

There are other extras you could throw in. Like, if your buyer is coming from an apartment and has never had a yard before, they may ask if you’d be willing to leave your lawn mower behind. That’s another lever you could pull to keep them happy.

How Concessions Help Sellers

Offering concessions can be a smart strategy for sellers to get a deal done. As Dennis Shirshikov, Professor of Finance and Economics, City University of New York/Queens College told The Mortgage Reports:

“Pricing homes realistically and being willing to offer concessions, such as covering a portion of closing costs or including upgrades, will be key to closing deals . . . in a less frenzied market.”

For example, let’s say you accepted an offer from a buyer, but after their inspection, you found out there are some repairs they want you to tackle before you hand over the keys.

Rather than starting at square one and searching for a new buyer, you could offer a concession. One option is you can take on the repairs and cover the costs yourself. But, if you really don’t want the hassle of dealing with contractors, you could reduce your price by however much repairs would cost. Alternatively, you could offer to pay a portion of your buyer’s closing expenses with the idea they’d use the money they saved at closing toward doing the repairs themselves.

Either way, a concession can be a great way to meet in the middle. However, it’s important to have an agent on your side to help with these negotiations.

A good real estate agent can help you decide when and how to offer concessions, so you don’t give away too much while still ensuring your house gets sold. It’s all about finding the right balance.

Bottom Line

With the market becoming more balanced, seller concessions are coming back into play in some areas. The key is having an agent to help guide you through the process, so things work out in your favor.

How To Buy a Home Without Waiting for Lower Rates

Many people are hoping mortgage rates will come down before they buy a home. But will that actually happen? According to the latest forecasts, experts say rates will decline, but not by as much as a lot of people want.

The good news? Even if they don’t drop substantially, there are still ways to make buying a home more affordable.

How Much Will Rates Drop?

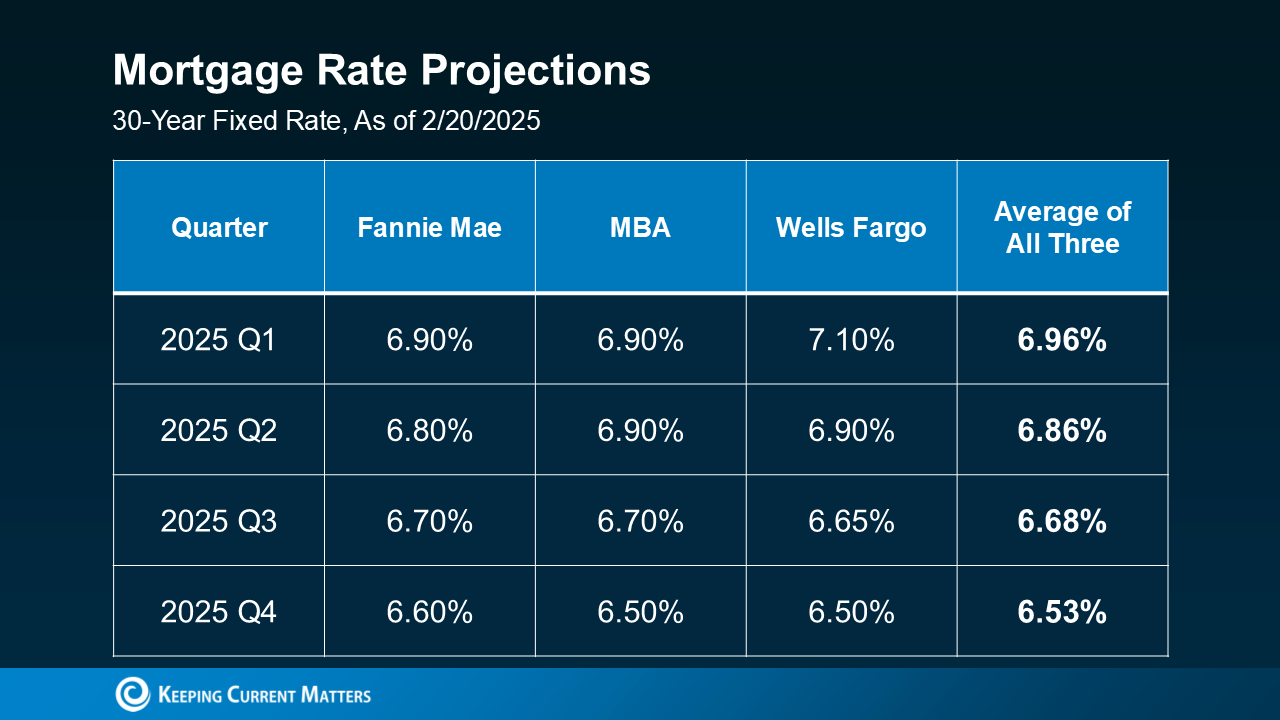

A few months ago, experts were forecasting mortgage rates could dip below 6% by the end of the year. But recent projections suggest that may not happen after all.

While mortgage rates are still expected to decline some later this year, projections from Fannie Mae, the Mortgage Bankers Association (MBA), and Wells Fargo now show them stabilizing closer to 6.5% by the end of the year (see below):

That means if you’re holding off on buying a home in hopes of much lower mortgage rates, you may be waiting a while. And if you need to move because something in your life has changed, like a new job, a new baby, or a marriage – waiting that long may not be an option.

Creative Financing Options in Today’s Market

Since rates aren’t expected to decline as much as originally expected, it may be worth considering alternative financing options that could help you get into a home sooner rather than later. Here are three strategies to discuss with your lender to see if any of these make sense for you:

1. Mortgage Buydowns

A mortgage buydown allows you to pay an upfront fee to lower your mortgage rate for a set period of time. This can be especially helpful if you want or need a lower monthly payment early on. In fact, 27% of agents say first-time homebuyers are increasingly requesting buydowns from sellers in order to buy a home right now.

2. Adjustable-Rate Mortgages

Adjustable-rate mortgages (ARMs) typically start with a lower mortgage rate than a traditional 30-year fixed mortgage. This makes them an attractive option, especially if you expect rates to drop in the coming years or plan to refinance later.

And if you remember the housing crash, know that today’s ARMs aren’t like the risky ones back then. Lance Lambert, Co-Founder of ResiClub, helps drive this point home by saying:

“. . . ARM products today are different from many of the products issued in the mid-2000s. Before 2008, lenders often approved ARMs based on borrowers ability to pay the initial lower interest rates. And sometimes they didn’t even check that (remember Ninja loans). Today, adjustable-rate borrowers qualify based on their ability to cover a higher monthly payment, not just the initial lower payment.”

In simple terms, banks used to give loans without checking to see if buyers could afford them. Now, lenders verify income, assets, and jobs, reducing the risks associated with ARMs compared to the past.

3. Assumable Mortgages

An assumable mortgage allows you to take over the seller’s existing loan — including its lower mortgage rate. And with more than 11 million homes qualifying for this option according to U.S. News, it’s worth exploring if you want or need a better rate.

Bottom Line

Waiting for a big decline in mortgage rates may not be the best strategy. Instead, options like buydowns, ARMs, or assumable mortgages could make homeownership more affordable right now. If you need to contact a lender, give me a call! I have a great recommendation!

Consumer Guide: Preparing for Homeownership

Whether you are a first-time buyer or planning your next move, you should consider many factors as you prepare for the home purchase process. Here’s what prospective buyers should know:

How should I begin to think about what kind of home suits my needs?

Before beginning the search process, you should consider what kind of home best suits your needs based on factors like size, location, convenience (including proximity to public transportation, schools, or recreational facilities), privacy, and amenities. It is also important to account for how your needs may change in the future. When deciding on which agent to work with, keep in mind that a REALTOR® is obligated to Put Client Interests Above Their Own. You can also ask a REALTOR® if they are familiar with your preferred markets and what their strategy is.

How important is my credit score?

Establishing a good credit history takes time, and it is never too early to start working on it. Your credit score will impact your approval for a home loan and the terms of your mortgage, including how much you can borrow and what programs will lend to you. Buyers with strong credit scores may benefit from lower interest rates on their mortgage. Using credit cards and paying the balance off on time and in full each month can help you improve or start building your credit score.

What is mortgage pre-approval?

Getting pre-approved for a mortgage can help buyers better compete in high-demand housing markets and, in some cases, can be required to make an offer. Pre-approval requires verified financial information and is different than pre-qualification, which provides an estimate of how much you can borrow using self-reported information. However, pre-approval does not lock in your mortgage rate, which may change with the market.

What if I can’t afford the cost of the down payment?

While down payments are typically 10-20% of a home’s purchase price, some buyers may qualify to pay a lower down payment, such as 3-5% of the purchase price through a government-backed mortgage, such as Federal Housing Administration (FHA) loans and those from the Veterans Administration (VA), or down payment assistance programs. However, these lower down payments often require mortgage insurance. A higher down payment can help you avoid the cost of mortgage insurance and potentially help you qualify for a better interest rate.

What other items should I budget for?

In addition to your down payment, mortgage payments, and closing costs, there are many other expenses to budget for when preparing to buy a home. Items like moving, maintenance and repair costs, utilities and monthly bills, homeowners insurance, and property taxes are also key considerations. Some buyers may also need to factor in annual or monthly payments to a homeowners association (HOA) or hazard insurance for floods or fire.

What resources are available to help me prepare for the buying process?

For many buyers, the process of purchasing a home can seem complicated and overwhelming. Prospective buyers can participate in homebuyer education classes or work with a HUD certified housing counselor to gain tools and information to help resolve financial roadblocks, develop a budget, and work on a plan to meet the financial requirements of homeownership. Agents who are REALTORS® and your state and local REALTOR® Associations can help you find the right resources for your needs.

How soon should I be ready to move?

While preparing to buy a home can take time, the process may move quickly once you begin looking at homes. Especially in markets with low inventory, home buyers will be best suited if they are prepared to act fast on a desired property or risk missing out on the first home they wish to purchase because they can’t act fast enough. Be sure to consider your timeline and flexibility well in advance to avoid an unnecessary rush or scheduling issues.

Practices may vary based on state and local law. Consult your real estate professional and/or an attorney for details about state law where you are purchasing a home. Please visit facts.realtor for more information and resources.

How Your Home Can Shelter You From Taxes

For most Americans, buying a home is the biggest investment they will make. There are ways to make it less taxing. The Internal Revenue Service spells out the details in Publication 530, Tax Information for Homeowners, which it updates each year. Here are some key things to know about when it comes to taxes and owning or buying a home.

DEDUCTIONS

Mortgage interest deduction

Taxpayers who itemize deductions, instead of taking the standard deduction, can deduct mortgage interest paid for loans on their main home and a second home—up to a point.

You generally can deduct home mortgage interest only to the extent the loan proceeds from your mortgage are used to buy, build or substantially improve the home securing the loan.

The loan can be a first or second mortgage, a home-improvement loan, a home-equity loan or a refinanced mortgage.

- For mortgages originated on or before Dec. 15, 2017, interest on up to $1 million of debt is deductible ($500,000 if married filing separately).

- For mortgages originated after Dec. 15, 2017, interest on up to $750,000 of debt is deductible ($375,000 if married filing separately).

These rules are subject to change after 2025, depending on whether Congress extends the 2017 tax-law provisions on mortgage interest deductions.

IRS Publication 936, Home Mortgage Interest Deduction, has more details.

Deduction for state and local property taxes

Homeowners who itemize deductions can deduct state and local real-estate taxes, subject to an overall SALT cap.

The deduction for state and local taxes, including income, sales or real-estate taxes, is limited to $10,000 per return ($5,000 if married filing separately).

That cap, though, is controversial, and lawmakers are fighting over its fate. The so-called SALT cap is one of the temporary provisions of the 2017 tax law that is set to expire at the end of 2025. If it does, or the level of the cap is increased, more taxpayers, especially in states with high property-tax rates, may be able to itemize and get a larger deduction.

Home-office deduction

Self-employed individuals who use part of their home exclusively and regularly for business purposes can deduct expenses related to a home office. The catch is that you have to have self-employment income. You can’t take the deduction for working from home for a job where you receive a W-2 from an employer.

A simplified method allows taxpayers to use a rate of $5 a square foot of the portion of the home used for business, up to a maximum of 300 square feet, to compute the business use of home deduction.

IRS Publication 587, Business Use of Your Home, has details.

What you can’t deduct

While homeownership brings many possible deductions, there are a number of things you can’t use to reduce your taxes, according to the IRS. These include:

• Insurance, including title insurance

• Wages you pay for domestic help

• Depreciation

• The cost of utilities or home repairs

• Internet or Wi-Fi

• Homeowners or condominium association fees

CREDITS

Energy-efficient home improvement credit

Homeowners who make certain energy-efficient improvements to their homes can claim a tax credit of up to $3,200 a year.

This credit equals 30% of the cost of allowed improvements. Insulation, windows and doors can qualify. Heat pumps, water heaters and biomass stoves can count, too.

There are sublimits for different types of improvements: $600 for windows, $2,000 for a heat pump, for example.

Unlike tax deductions that lower income, a tax credit is typically a dollar-for-dollar reduction of tax.

Certain efficiency standards must be met to qualify. For more information, see the IRS Energy Efficient Home Improvement Credit information page.

These credits were expanded under the Inflation Reduction Act of 2022. There is the possibility that some or all of them might come under fire in the new Trump administration.

Solar, wind and geothermal credit

Homeowners who add solar-, wind- or geothermal-power generation, solar water heaters or battery storage to their homes can claim residential clean-energy credits.

The credit covers 30% of the cost of allowed improvements, with no annual or lifetime maximum.

The credit is nonrefundable, meaning the amount you receive can’t exceed the amount you owe in tax. You can carry forward any excess unused credit to future tax years.

For more information, see the IRS Residential Clean Energy Credit information page.

These credits may also be called into question in the new administration and as the new Congress takes up tax legislation.

SELLING A HOME

Home seller’s exclusion

If you sell your home when you are living and it has gone up in value since you bought it, you will potentially owe capital-gains taxes on the gain.

The gain is the difference between the selling price and the adjusted basis—what you paid for the house, plus any renovations or other capital improvements and certain selling expenses. IRS Publication 523, Selling Your Home, has examples of improvements that count, such as new siding, a patio or ductwork.

The home-sale exclusion lets homeowners skip taxes on a large chunk of profit when they sell their homes.

• Single filers can exclude up to $250,000 of capital gains.

• Married couples filing jointly can exclude up to $500,000 of capital gains.

To be eligible, the homeowner typically must have used the house as a primary residence for at least two of the previous five years.

Leaving your home to heirs

Keeping your home until death is one of the ultimate tax breaks.

When an owner dies and leaves a property to heirs, the capital gains can effectively get reset to zero. This is called a step-up in basis. It means the heir would owe capital-gains taxes only on the home’s growth in value over the fair-market price at the time of the owner’s death.

The 3 Biggest Mistakes Sellers Are Making Right Now

If you want to sell your house, having the right strategies and expectations is key. But some sellers haven’t adjusted to where the market is today. They’re not factoring in that there are more homes for sale or that buyers are being more selective with their budgets. And those sellers are making some costly mistakes.

Here’s a quick rundown of the 3 most common missteps sellers are making, and how partnering with an expert agent can help you avoid every single one of them.

1. Pricing the Home Too High

According to a survey by John Burns Real Estate Consulting (JBREC) and Keeping Current Matters (KCM), real estate agents agree the #1 thing sellers struggle with right now is setting the right price for their house (see graph below):

And more often than not, homeowners tend to overprice their listings. If you aren’t up to speed on what’s happening in your local market, you may give in to the temptation to price high so you can have as much wiggle room as possible to negotiate. You don’t want to do this.

And more often than not, homeowners tend to overprice their listings. If you aren’t up to speed on what’s happening in your local market, you may give in to the temptation to price high so you can have as much wiggle room as possible to negotiate. You don’t want to do this.

Today’s buyers are more cautious due to higher rates and tight budgets, and a price that feels out of reach will scare them off. And if no one’s looking at your house, how’s it going to sell? This is exactly why more sellers are having to do price cuts.

To avoid this headache, trust your agent’s expertise from day 1. A great agent will be able to tell you what your neighbor’s house just sold for and how that impacts the value of your home.

2. Skipping Repairs

Another common mistake is trying to avoid doing work on your house. That leaky faucet or squeaky door might not bother you, but to buyers, small maintenance issues can be red flags. They may assume those little flaws are signs of bigger problems — and it could cost you when offers come in lower or buyers ask for concessions. As Investopedia says:

“Sellers who do not clean and stage their homes throw money down the drain. . . Failing to do these things can reduce your sales price and may also prevent you from getting a sale at all. If you haven’t attended to minor issues, such as a broken doorknob or dripping faucet, a potential buyer may wonder whether the house has larger, costlier issues that haven’t been addressed either.”

The solution? Work with your agent to prioritize anything you’ll need to tackle before the photographer comes in. These minor upgrades can pay off big when it’s time to sell.

3. Refusing To Negotiate

Buyers today are feeling the pinch of high home prices and mortgage rates. With affordability that tight, they may come in with an offer that’s lower than you want to see. Don’t take it personally. Instead, focus on the end goal: selling your house. Your agent can help you negotiate confidently without letting emotions cloud your judgment.

At the same time, with more homes on the market, buyers have options — and with that comes more negotiating power. They may ask for repairs, closing cost assistance, or other concessions. Be prepared to have these conversations. Again, lean on your agent to guide you. Sometimes a small compromise can seal the deal without derailing your bottom line. As U.S. News Real Estate explains:

“If you’ve received an offer for your house that isn’t quite what you’d hoped it would be, expect to negotiate . . . the only way to come to a successful deal is to make sure the buyer also feels like he or she benefits . . . consider offering to cover some of the buyer’s closing costs or agree to a credit for a minor repair the inspector found.”

The Biggest Mistake of All? Not Using a Real Estate Agent

Notice anything? For each of these mistakes, partnering with an agent helps prevent them from happening in the first place. That makes trying to sell your house without an agent’s help the biggest mistake of all.

Bottom Line

Avoid these common mistakes by starting with the right plan — and the right agent. Connect with an agent so you don’t fall into any of these traps.

How Home Sellers Can Use Concessions to Get to Closing

As home inventory begins to grow and buyers regain some advantage in the market, sellers may consider offering more in negotiations to make the deal more attractive and get to the closing table.

“With where interest rates are, buyers can be deterred if they don’t feel like they’re getting some kind of deal,” says Cooper Thayer, ABR, broker-associate at Keller Williams Action Realty in Denver. “We’re definitely advising sellers that they can expect to offer a concession to help a buyer get into their home specifically—if it’s not a super-hot product.”

What Are Seller Concessions?

A concession is when the seller covers certain costs associated with the purchase of the home. Concessions can make homeownership more accessible for buyers by reducing upfront costs. Seller concessions are often used in markets where buyers have more negotiating power or when the seller needs to stand out in a competitive environment.

Real Examples of Seller Concessions in Action

NAR data found that “given buyer demand and lack of housing inventory,” only 24% of sellers nationwide offered a concession in 2024, down from 33% the previous year.

While the 2025 housing market remains to be seen, several signs point to a healthier outlook: both pending home sales and existing-home sales jumped in November and there are more homes on the market compared to a year ago.

“Sellers do have to differentiate themselves in the market now with the levels of inventory that we’re at,” Thayer says.

In late 2024, NAR published a one-page resource on seller concessions, which is part of a series of Consumer Guides that NAR provides at facts.realtor. The consumer guides address many aspects of the homebuying and selling process as well as the real estate practice changes that went into effect last August. NAR members can share the guides directly with their clients.

Concessions can cover a wide range of costs, like those associated with a title search, home repairs or fees for real estate agents and appraisers. Closing costs were the most common concession in 2024, NAR data shows. That makes sense in markets with a high volume of first-time buyers, like Salt Lake City, where the median age of residents is 33.

“First-time home buyers are huge in our area,” Scott Robins, an associate broker at Summit Sotheby’s International Realty in Salt Lake City, says. “We have two universities in downtown Salt Lake City. We have four additional universities within an hour drive. If I’m working with a first-time home buyer, it’s almost given that they are going to need some help with concessions.”

He says those in their late-20s and early-30s “typically have their down payment, but they don’t have all of their closing costs.”

Robbins says 2-1 buydowns as a seller concession are popular. Essentially, the seller will pay to reduce the buyer’s mortgage rate by two percentage points for the first year and one percentage point for the second year. After those two years of monthly savings, buyers are on the hook for their agreed upon mortgage rate.

“The place where concessions or rate buydown offerings are really being successful right now is with new construction,” Thayer says. “We’re seeing builders utilize those kinds of incentives a lot more because they have the ability to, one, hold on to their inventory longer, and two, do a better job at marketing those incentives. They’ve got a little bit more marketing purchase power than the average [real estate broker or agent] has.”

Home repair credits are also common. Most buyers want a turnkey home, Thayer says, “so those concessions are a useful tool, but they’re definitely not the end-all, be-all.”

Marlene Llamas Leon, ABR, CIPS, of LPT Realty in Miami recalls a recent deal on a large estate in which her sellers chose to make a concession.

“What came up in the inspection were six roof leaks that [the sellers] had no idea they had, and the new roof for the home was $120,000,” she says. “So, that was definitely something that [if this transaction had fallen through] we would have had to disclose, and it would have been a turnoff for any buyer that would have walked in next. These sellers were very proactive, thank goodness. Once I spoke to them, they completely understood, and they said, ‘Please leave it up to the buyer. Do they prefer a credit or a price reduction?’”

The buyer went with a price reduction.

In general, Thayer advises his sellers to make repairs before putting their homes on the market.

“That is really the best strategy that we’ve seen … to really differentiate your home as much as possible so we don’t have to start talking about concessions and really minimize what may come up in an inspection objection,” Thayer says.

Real estate trends to watch in 2025

According to Ryan Lundquist over at the Sacramento Appraisal Blog, here are THINGS TO WATCH IN 2025:

Sellers will continue to thaw out: Last year we saw more listings come to the market. In fact, we had about 3,500 more new listings than 2023 in the region. But the wild part is we were still missing over 11,500 new listings from the pre-2020 normal level. Can you see why prices have remained higher? Anyway, right now it looks like 2023 was a bottom for seller inactivity, which is a good thing. This year I expect for new listings in 2025 to outpace 2024 levels as lifestyle moves come up for sellers. We still won’t be anywhere close to a normal number of listings though.

New construction will do well again this year: Locally, I expect new construction to still do well. That may not be the vibe in some markets around the country, but 2024 was one of the strongest years we’ve seen over the past decade locally. Part of the success comes from buyers aching for quality inventory, so builders have a captive audience. But let’s be real that the huge x-factor is builders offering incentives.

Buyer demand will thaw out more: In 2024, we did better than 2023 and 2007. I know that’s not a huge flex, but having about 6% more closed sales in the region feels like a real win. What this means is we had over one thousand more buyers purchase homes last year. Look, the math still won’t work for many people, so don’t expect the floodgates of volume to open up in 2025, but we should get more buyers as long as rates hover around 7% instead of going higher.

For the full blog post and list.. CLICK HERE