Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

More home sellers are paying capital gains taxes — here’s how to reduce your bill

More Americans are paying capital gains taxes on home sale profits amid soaring property values — but there are ways to reduce your bill, experts say.

In 2023, nearly 8% of U.S. home sales yielded profits exceeding $500,000, compared with about 3% in 2019, according to an April report from real estate data firm CoreLogic.

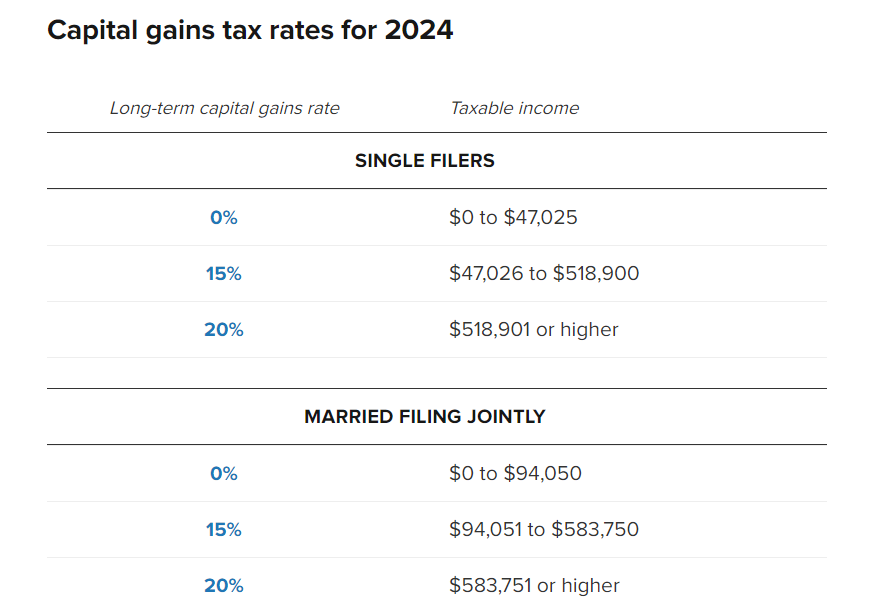

It’s key for a special tax break for homeowners who make a profit when selling a primary residence. Married couples filing together can make up to $500,000 on the sale without owing capital gains taxes. The threshold for single filers is $250,000.

Those capital gains exemption thresholds haven’t been indexed for inflation since 1997, said certified financial planner Jaime Quinones with Stockade Wealth Management in Marlboro, New Jersey.

“With the recent rise in home values, more sellers have been facing a capital gains tax hit,” Quinones said.

Home sale profits above the $250,000 or $500,000 thresholds incur capital gains taxes of 0%, 15% or 20%, depending on your income.

Capital gains taxes on a home sale are more common in high-cost areas. In 2023, the percentage of home sales that had profits exceeding $500,000 hit double digits in Colorado, Massachusetts, New Jersey, New York and Washington, the CoreLogic report found.

How to qualify for the capital gains exemption

The IRS has strict rules for qualifying for the $250,000 or $500,000 capital gains exemption, according to the IRS. To that point, you must own the home for at least two of the past five years before your home sale to satisfy the “ownership test.”

The “residence test” says the home must be your primary residence for any 24 months of the five years before the sale, with some exceptions. The 24 months don’t need to be consecutive.

How to reduce your capital gains tax bill

If you’ve lived in a home long enough to exceed the capital gains exemptions, there’s a “high probability” you’ve made improvements to the home, said Falls Church, Virginia-based CFP Parker Trasborg, senior financial advisor at CJM Wealth Advisers.

You can use those improvements to increase your home’s “basis,” or original purchase price, which reduces your profit, he said.

But routine maintenance and repairs don’t count. For example, you can increase your home’s basis by adding the cost of a new roof or addition. But fixes to leaky pipes won’t qualify.

After selling a home, the IRS receives Form 1099-S, which shows your closing date and gross proceeds. But you’ll need paperwork to prove any changes to your home’s basis in the case of an IRS audit.

PUBLISHED TUE, MAY 7 2024

What Buyers, Sellers Want Most From Real Estate Agents

When it comes to buying or selling a home, what are the top things that most clients are looking for when they hire a real estate agent? Let’s take a look..

The majority of home buyers and sellers rely on real estate agents—nearly 90% of them—but they’re looking for certain types of help, and what they need could differ depending on their age and experience in the market, finds a new study from the National Association of REALTORS®.

Home buyers, for example, don’t just want help with finding a home, but also with negotiating and with learning about the real estate process, according to NAR’s 2024 Home Buyers and Sellers Generational Trends Report.

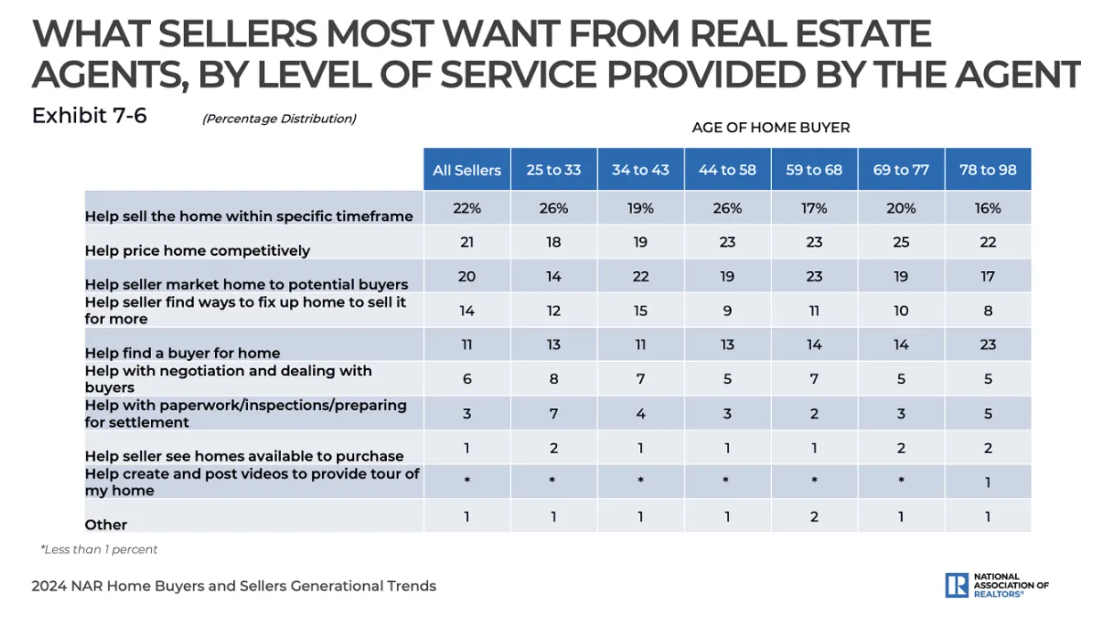

“While the internet is being utilized throughout the home search, agents remain the most-used information source in the home search, followed by mobile or tablet search devices,” the study reports. “Sellers, as well, turned to professionals to price their homes competitively, help market their homes to potential buyers, sell within a specific time frame, and find ways to fix up their homes to sell them for more.”

What Buyers Want: A Guide and Coach

Younger home buyers are more likely to say that one of the most difficult steps in the homebuying process—behind finding a property and saving for the down payment—is understanding the real estate process and the steps they need to take, the study finds. Older adults, ages 44 and up, tend to feel more confident heading into the purchase process, generally having had previous experience buying a home. Nearly a quarter of older adults cited “no difficult steps” in the homebuying process, the survey says. But they still report struggling with finding the right property and with completing the paperwork in a transaction.

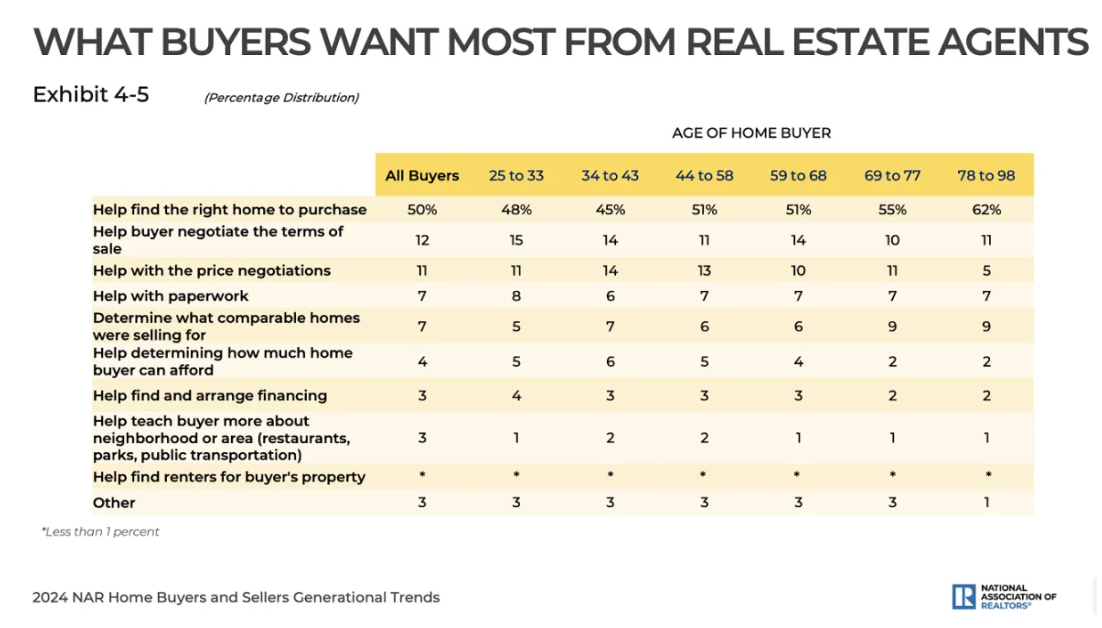

As buyers reflected on their experience, they reported that the most commonly cited benefits provided by real estate agents during the home purchase process were:

- Helping buyer understand the process: 61%

- Pointing out unnoticed features/faults with property: 58%

- Negotiating better sales contract terms: 46%

- Providing a better list of service providers (e.g. home inspectors): 46%

- Improving buyer’s knowledge of search areas: 45%

- Negotiating a better price: 33%

- Shortening a buyer’s home search: 23%

- Expanding buyer’s search area: 21%

When choosing an agent, buyers said their top criteria were the agent’s experience (21%), honesty and trustworthiness (19%), reputation (15%), and whether the agent was a friend or family member (12%). An agent’s reputation tended to be slightly more important to older generations than to younger generations, the study says.

Home buyers also said they valued constant communication from their real estate agent, identifying their top likes as agents who personally call them to inform them of activities (73%), those who send them property information and communicating via text message (71%), and those who send them postings as soon as a property is listed or when the price changes or the listing is under contract (70%).

What Home Sellers Want: Make Their Home Stand Out

More than one-third of home sellers—across age groups—relied on a referral from a friend, neighbor or relative to find their real estate agent, the survey finds. Only 5% relied on internet searches to find one. Sellers reported their top criteria for choosing their real estate agent was the agent’s reputation, their honesty and trustworthiness, and whether the agent was a friend or a family member.

7 Types of Tax-Deductible Home Improvements

Here’s an overview of a few examples of tax-deductible home improvements. As always, you should consult a tax professional to understand more about what qualifies for deductions.

Energy-Efficient Upgrades

Homeowners can potentially qualify for an Energy Efficiency Home Improvement Credit of up to $3,200 for energy-efficient improvements made after Jan. 1, 2023. The credit for 2024 is 30% of qualified expenses, but it has certain limits depending on the type of improvement.

Energy efficient upgrades can help reduce energy usage and strain on a home’s critical systems. Upgrades can include structural improvements to the home and the installation of new systems. Here are some sample projects:

- A home energy audit may be eligible for a tax credit of up to $150. An auditor will help your clients understand where they’re losing energy and identify health and safety issues in their home. A home energy audit could help save up to 30% on energy bills, according to the Department of Energy. To qualify for the credit, the audit must be conducted by a qualified home energy auditor or someone who is supervised by a qualified auditor. It also must include a written report prepared and signed by a qualified home energy auditor, and the report must be consistent with industry best practices. Find more information in Notice 2023-59.

- Install ENERGY STAR’s Most Efficient exterior windows and skylights for a credit of up to $600 based upon eligibility. Replacing windows can help improve insulation and reduce the need to run the HVAC system.

- Install biomass stoves that meet ENERGY STAR’s requirements for up to a $2,000 credit. Biomass stoves must have a thermal efficiency rating of at least 75% to qualify, and costs may include labor to install. Biomass can consist of wood pellets and grasses. Although burning biomass can reduce energy usage, insurance experts recommend following wood-burning best practices to help reduce fire and other health risks.

Clean Energy Upgrades

Homeowners could potentially qualify for the Residential Clean Energy Credit if they install new renewable energy properties in their homes. There is no dollar limit for this credit except for fuel cell properties ($500 for each half-kilowatt of capacity).

Using clean energy can help lower reliance on traditional utilities and lower usage and bills. Systems like solar panels are generally easy to maintain, typically only requiring regular cleaning to prevent debris buildup. Here are some sample projects:

- Installing a solar water heater can help reduce strain on a traditional water heater and help prolong its life, depending on the type installed. For example, a two-tank solar water heater preheats water before it reaches a traditional water heater. Water heating is typically the second largest energy expense in any home.

- Installing geothermal heat pumps can help heat and cool a home more efficiently than traditional heating and cooling systems by transferring heat to the ground rather than generating heat. They tend to be expensive, but according to the Department of Energy, it could potentially see a return on investment for homeowners in five to 10 years depending on available financial incentives.

- Battery storage technology helps store excess energy generated from clean energy sources. This gives a home a reliable energy source if the grid goes down.

Historic Home Upgrades

The Federal Historic Rehabilitation Tax Credit could apply if homeowners are undergoing a renovation of a historic home. Historic homes can qualify for this tax credit and other grants since many organizations wish to preserve historical buildings. Taking advantage of these can help lower the financial burden of potential repairs while helping to restore a home’s original beauty. Here are some sample projects:

- Upgrading or replacing old pipes may qualify for this tax credit and may be necessary to bring the home up to code and help prevent water damage.

- Replacing deteriorated parts in the structure of a home, like posts or beams, may qualify for this credit. Replacement should be visually similar to the original and at least equal to the original’s load-bearing capabilities.

- Fully replacing a deteriorating set of stairs using the same or compatible substitute material can make a home safer and also may qualify for this tax credit. The new set of stairs should look similar to the original.

Medically Necessary Upgrades

Homeowners could potentially include medically necessary home upgrades as a part of a medical expense deduction. These include improvements that help make a home more accommodating for a person with a disability, spouse or dependents that live in the home. The amount that can be included in a medical expense deduction depends on how the improvement impacts the home’s value:

- If the home’s value increases as a result of the improvement, the medical expense is considered the cost of the improvement minus the increase in home value.

- If the home’s value does not increase, it can include the entire cost in the medical expense deduction.

Homeowners can invest in upgrades that can help make their home more accessible and help prevent future maintenance issues (which is especially important if they plan to age in place). For example, lowering kitchen cabinets or installing pull-down shelves can help prevent potential falls and damage when straining for out-of-reach items. Here are some sample projects:

- Installing modified smoke detectors and other monitoring systems can help alert those with a disability, like alarms with strobe lights for those who are hard of hearing. Smart monitoring systems, like water leak detectors, can also make it easier to detect issues early in hard-to-reach areas.

- Grading, or leveling, the ground can improve accessibility and also help protect a home from water runoff. Grading can help reduce steep slopes and create more accessible pathways for those with mobility challenges. It can also help direct runoff away from a home and prevent standing water.

- Bathroom modifications, like grab bars and railings, can help prevent slips and falls. These modifications also can help prevent water splashes that could lead to mold or mildew over time.

Home Office Repairs and Improvements

Homeowners may be eligible to deduct home office repair expenses if they have a dedicated part of their home that they regularly use as their main place of business. The amount that can be deducted depends on whether the project impacts the entire home or just the office. Home office improvements are not tax deductible and would be categorized similarly to capital improvements. Here are some sample projects:

- If installing a full home security system, homeowners could potentially deduct the cost of maintaining and monitoring the system that relates to the business part of their home.

- Repairing damaged outlets and wiring may be tax deductible and, more importantly, a crucial project to help prevent electrical fires and potential damage to devices. Electrical distribution or lighting equipment (which includes wiring and outlets) was the leading cause of home property damage from 2016 to 2020, according to the April 2023 National Fire Protection Association Home Structure Fires Report.

- Replacing home office windows with dual or triple-pane windows to help improve insulation and reduce noise also may be eligible. In addition to the tax benefits, homeowners may find it good for resale value, too, since this can help lower the need for cooling and heating and lower the strain on an HVAC system.

Rental Property Repairs

If homeowners rent out a part of their home, they may be able to deduct repair expenses from the amount of taxable rental income they receive. Limitations apply, such as if they’re renting a space in their current residence.

Maintaining the parts of their home that they rent can help prevent issues from impacting the rest of their home. For example, issues like water leaks or drafts in one area can lead to bigger issues if left unaddressed. Here are some sample projects:

- Repairing leaks in a tenant’s bathroom can help prevent long-term mold and mildew issues. Leaks also could impact a home’s structural integrity if drywall or floor joists are left wet over time.

- Addressing air leaks in a tenant’s area can help improve insulation, keep them comfortable and lower the need to cool or heat that part of a home. Updating the weather stripping around windows and doors may also apply.

- Routinely checking the air vents in a tenant’s part of the home can improve the chances of catching airflow issues early, including dirty vents or leaky ducts. Improved airflow can help boost indoor air quality and regulate temperature throughout your home.

Capital Improvements

Capital improvements are projects that extend a home’s life, add value or refit a home for new uses. These differ from home repairs, which are part of property maintenance but don’t necessarily add value (like fixing a leak). There are some limitations to the types of eligible improvements. For example, homeowners cannot include the cost of installing carpeting if they later remove it. They also cannot include energy-related improvements if they received subsidies or tax credits for those improvements.

Homeowners can add the value of qualifying capital improvements to the cost basis of their home. When they sell their home one day, they may be able to subtract their adjusted cost basis from the sale price. This can help reduce the amount of capital gains taxes they may owe. However, they’ll also need to take into account the tax implications of the capital gains from the sale of their home.

Although homeowners won’t see tax benefits from these improvements right away, these projects can help proactively protect a home by getting ahead of potential issues. Here are some sample projects:

- Installing a new HVAC system to replace one that’s over 10 to 25 years old, isn’t running efficiently or is worn beyond repair can help save money and help protect a home. A modern and efficient HVAC system can improve air circulation, maintain temperature control, and help cut down on utility costs in the process.

- Installing attic insulation can cost about $1.80 per square foot and can help reduce heating and cooling costs, easing stress on an HVAC system. A better-insulated attic can also help maintain a roof’s temperature and prevent related damage, like the expanding and contracting that can occur with winter ice dams.

- Installing water softeners can help reduce calcium and magnesium in the water. This helps reduce buildup in plumbing fixtures and pipes and helps appliances run more efficiently and last longer.

By Courtney Klosterman, home insights expert and director of communications at Hippo Insurance

Let Your Home Equity Fund Your Retirement

Struggling with Money? Learn about Home Equity Conversion Mortgages (HECMs)

If you’re low on cash, you might consider a Home Equity Conversion Mortgage (HECM). It’s like a reverse mortgage backed by the government. This means if you meet certain requirements, you can borrow money against the value of your home. The Federal Housing Administration (FHA) guarantees repayment to the lender, so it’s secure. In recent years, HECMs have become more popular, especially among older folks who need extra cash and plan to stay in their homes forever.

Understanding HECM Rules

To qualify for an HECM, you need to be at least 62 years old. Also, you’ll have to pay back the loan when you move out, sell your house, or pass away. You must own your home or have a significant portion paid off, and it must be your primary residence. Plus, you’ll need to have a session with a counselor approved by the Department of Housing and Urban Development (HUD).

Limits and Considerations

The amount you can borrow depends on factors like your age, current interest rates, and the value of your home. Typically, older homeowners with more valuable properties can borrow more.

HECM vs. Regular Mortgages

Unlike traditional mortgages, with HECMs, the amount you owe increases over time. You’ll still need to cover property taxes, insurance, and upkeep costs. Also, the interest you pay isn’t tax-deductible until you pay off the loan.

How You Get Paid

You can choose to receive HECM funds as a lump sum or in monthly payments or a line of credit. You’re free to use the money as you wish, whether for essential expenses, paying off debts, or enjoying life.

HECMs offer a flexible way to access cash when you need it, especially for retirees looking to boost their income.

Attractive features

An HECM offers some compelling advantages if your circumstances fit:

- You can plan on staying in your “forever” home, where you are settled, and can perhaps renovate it, allowing you to age in place.

- You can enjoy a reliable cash flow in order to provide more comfortable senior years.

- You need not make monthly payments on the loan balance.

- Your spouse can usually remain in the home even if you die or move to another accommodation.

- You can pay off debt balances, such as medical bills.

- You can use the proceeds to pay off existing mortgages and thereby prevent foreclosures.

- You can avoid paying withdrawal penalties on other retirement accounts.

- You can fund a grandchild’s education or any other meaningful purpose.

- Integrated protections limit your heirs’ responsibilities.

But is it right for you?

There are several significant drawbacks, so seniors must take extra care with such an important decision:

- Fees tend to be high, including upfront financed origination charges of about 2% and around .5% for annual review of mortgage insurance premiums.

- You could compromise your benefits from needs-based programs, such as Medicaid.

- You could inadvertently default by failing to meet loan requirements, including by living outside the home most of the year, neglecting property taxes or home insurance, or not making maintenance repairs. An unresolved default might lead to eviction and foreclosure.

Alternative loans may be more appropriate. For example, those under age 62 could use home equity loans (HELOCs). More expensive properties may require a jumbo reverse mortgage, with higher interest rates but no mortgage insurance. By contrast, single-purpose reverse mortgages are cheapest and can be used for specified expenses such as taxes or repairs.

Your financial advisor can help you compare different types of reverse mortgages, payment options and other considerations.

Why 90% of Homebuyers Will Continue to Choose Working with Real Estate Agents: Insights from the National Association of Realtors

Members of the National Association of Realtors will continue to be the most reliable partner for the millions of Americans striving to realize the American dream through homeownership.

Specifically, the settlement will prohibit offers of compensation from being shared on multiple listing services (MLSs), the databases that show real estate brokers the properties for sale, and it will require MLS participants to enter into written agreements with their buyers.

These changes will go into effect in mid-late July 2024.

It’s important to note that the National Association of Realtors does not set commissions, and nothing in this proposed settlement would change that. Commissions would continue to be negotiable among buyers, sellers, and their brokers.

The “cooperative compensation” rule that has been subject to litigation says that selling brokers have to specify on each listing an offer of compensation to buyers’ brokers. That offer could be any amount, even zero.

Cooperative compensation, where the compensation a seller pays to their broker is shared, covering the cost of a buyer broker’s services, will continue to be an important option for consumers in all transactions and especially those involving lower and middle-income homebuyers, who may already have a difficult-enough time saving for a down payment.

The bottom line is that consumers will continue to be able to choose what kind of professional real estate advice they’d like–and how much, and how, they will pay for the work of a real estate professional.

Historically, nearly 90% of homebuyers have opted to work with a real estate agent or broker. That figure is unlikely to change.

Even in an era where seemingly everything can be researched and purchased electronically, the clear value added by realtors remains evident. Nine in 10 home buyers would use their agent again or recommend their agent to others.

Seasoned agents and brokers also offer insights into property values, taxes, regulations, and zoning laws while overseeing thorough due diligence processes. And we connect buyers and sellers with other reputable real estate-related professionals such as lawyers, lenders, contractors, and inspectors–any of which can make or break a transaction.

When it comes time to make or evaluate offers, real estate professionals have a decades-long track record as skilled negotiators, ensuring that their clients submit the most competitive bids for their dream home–or hold out for what their home is really worth. And at the settlement table, we help our clients confidently close on what is likely the most significant financial transaction of their lives.

Even post-sale, real estate agents and brokers are crucial advisors for their clients, providing ongoing support, answering queries, and offering guidance as people confront the challenges and delights of homeownership.

NAR’s proposed settlement agreement and the associated practice changes will not change what makes realtors valuable: specialized knowledge, diligence, and a commitment to our clients’ best interests. And it does not change the fact that millions of people will continue to rely on us to help them fulfill their dream of homeownership.

Find the original article here

4 Tips To Make Your Strongest Offer on a Home

Are you thinking about buying a home soon? If so, you should know today’s market is competitive in many areas because the number of homes for sale is still low – and that’s leading to multiple-offer scenarios. And moving into the peak homebuying season this spring, this is only expected to ramp up more.

Remember these four tips to make your best offer.

1. Partner with a Real Estate Agent

Agents are local market experts. They know what’s worked for other buyers in your area and what sellers may be looking for. That advice can be game changing when you’re deciding what offer to bring to the table.

2. Understand Your Budget

Knowing your numbers is even more important right now. The best way to understand your budget is to work with a lender so you can get pre-approved for a home loan. Doing so helps you be more financially confident and shows sellers you’re serious. That gives you a competitive edge. As Investopedia says:

“. . . sellers have an advantage because of intense buyer demand and a limited number of homes for sale; they may be less likely to consider offers without pre-approval letters.”

3. Make a Strong, but Fair Offer

It’s only natural to want the best deal you can get on a home, especially when affordability is tight. However, submitting an offer that’s too low does have some risks. You don’t want to make an offer that’ll be tossed out as soon as it’s received just to see if it sticks. As Realtor.com explains:

“. . . an offer price that’s significantly lower than the listing price, is often rejected by sellers who feel insulted . . . Most listing agents try to get their sellers to at least enter negotiations with buyers, to counteroffer with a number a little closer to the list price. However, if a seller is offended by a buyer or isn’t taking the buyer seriously, there’s not much you, or the real estate agent, can do.”

The expertise your agent brings to this part of the process will help you stay competitive and find a price that’s fair to you and the seller.

4. Trust Your Agent During Negotiations

After you submit your offer, the seller may decide to counter it. When negotiating, it’s smart to understand what matters to the seller. Once you do, being as flexible as you can on things like moving dates or the condition of the house can make your offer more attractive.

Your real estate agent is your partner in navigating these details. Trust them to lead you through negotiations and help you figure out the best plan. As an article from the National Association of Realtors (NAR) explains:

“There are many factors up for discussion in any real estate transaction—from price to repairs to possession date. A real estate professional who’s representing you will look at the transaction from your perspective, helping you negotiate a purchase agreement that meets your needs . . .”

Bottom Line

In today’s competitive market, be sure to work with a local real estate agent to find you a home you love and craft a strong offer that stands out.

Finding Your Perfect Home in a Fixer Upper

If you’re trying to buy a home and are having a hard time finding one you can afford, it may be time to consider a fixer-upper. That’s a house that needs a little elbow grease or some updates, but has good bones. Fixer-uppers can be a really great option if you’re looking to break into the housing market or want to stretch your budget further.

Basically, since the number of homes for sale is still so low, if you’re only willing to tour homes that have all your dream features, you may be cutting down your options too much and making it harder on yourself than necessary. It may be time to cast a wider net.

Sometimes the perfect home is the one you perfect after buying it.

Here’s some information that can help you pinpoint what you truly need so you can be strategic in your home search. First, make a list of all the features you want in a home. From there, work to break those features into categories like this:

- Must-Haves – If a house doesn’t have these features, it won’t work for you and your lifestyle.

- Nice-To-Haves – These are features you’d love to have but can live without. Nice-to-haves aren’t dealbreakers, but if you find a home that hits all the must-haves and some of these, it’s a contender.

- Dream State – This is where you can really think big. Again, these aren’t features you’ll need, but if you find a home in your budget that has all the must-haves, most of the nice-to-haves, and any of these, it’s a clear winner.

Once you’ve sorted your list in a way that works for you, share it with your real estate agent. We can help you find homes that deliver on your top needs right now and have the potential to be your dream home with a little bit of sweat equity. Lean on our expertise as you think through what’s possible, what features are easy to change or add, and how to make it happen.

Your agent can also offer advice on which upgrades and renovations will set you up to get the greatest return on your investment if you ever decide to sell down the line.

Bottom Line

If you haven’t found a home you love that’s in your budget, it may be worth thinking through all your options, including fixer-uppers. Sometimes the perfect home for you is the one you perfect after buying it. To see what’s available in your area, you can search here!

Why We Aren’t Headed for a Housing Crash

If you’re holding out hope that the housing market is going to crash and bring home prices back down, here’s a look at what the data shows. And spoiler alert: that’s not in the cards. Instead, experts say home prices are going to keep going up.

Today’s market is very different than it was before the housing crash in 2008. Here’s why.

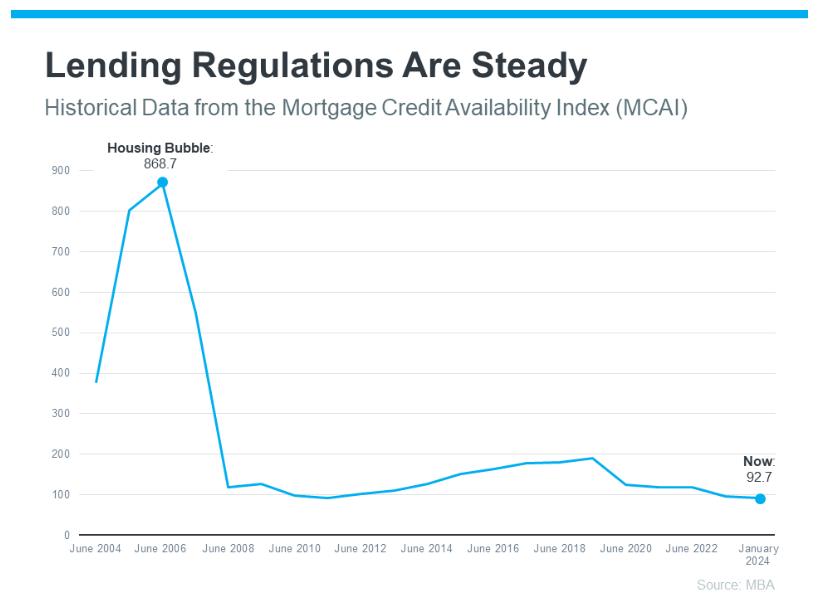

It’s Harder To Get a Loan Now – and That’s Actually a Good Thing

It was much easier to get a home loan during the lead-up to the 2008 housing crisis than it is today. Back then, banks had different lending standards, making it easy for just about anyone to qualify for a home loan or refinance an existing one.

Things are different today. Homebuyers face increasingly higher standards from mortgage companies. The graph below uses data from the Mortgage Bankers Association (MBA) to show this difference. The lower the number, the harder it is to get a mortgage. The higher the number, the easier it is:

The peak in the graph shows that, back then, lending standards weren’t as strict as they are now. That means lending institutions took on much greater risk in both the person and the mortgage products offered around the crash. That led to mass defaults and a flood of foreclosures coming onto the market.

There Are Far Fewer Homes for Sale Today, so Prices Won’t Crash

Because there were too many homes for sale during the housing crisis (many of which were short sales and foreclosures), that caused home prices to fall dramatically. But today, there’s an inventory shortage – not a surplus.

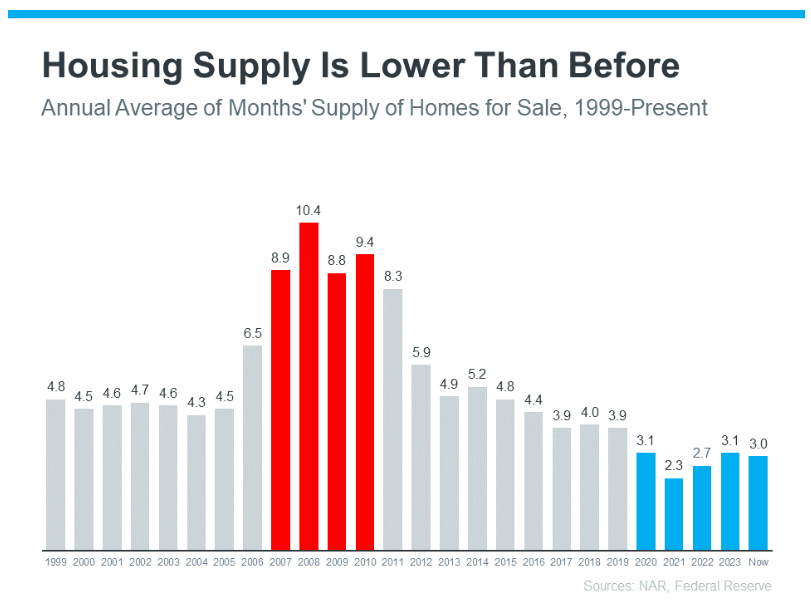

The graph below uses data from the National Association of Realtors (NAR) and the Federal Reserve to show how the months’ supply of homes available now (shown in blue) compares to the crash (shown in red):

Today, unsold inventory sits at just a 3.0-months’ supply. That’s compared to the peak of 10.4 month’s supply back in 2008. That means there’s nowhere near enough inventory on the market for home prices to come crashing down like they did back then.

People Are Not Using Their Homes as ATMs Like They Did in the Early 2000s

Back in the lead up to the housing crash, many homeowners were borrowing against the equity in their homes to finance new cars, boats, and vacations. So, when prices started to fall, as inventory rose too high, many of those homeowners found themselves underwater.

But today, homeowners are a lot more cautious. Even though prices have skyrocketed in the past few years, homeowners aren’t tapping into their equity the way they did back then.

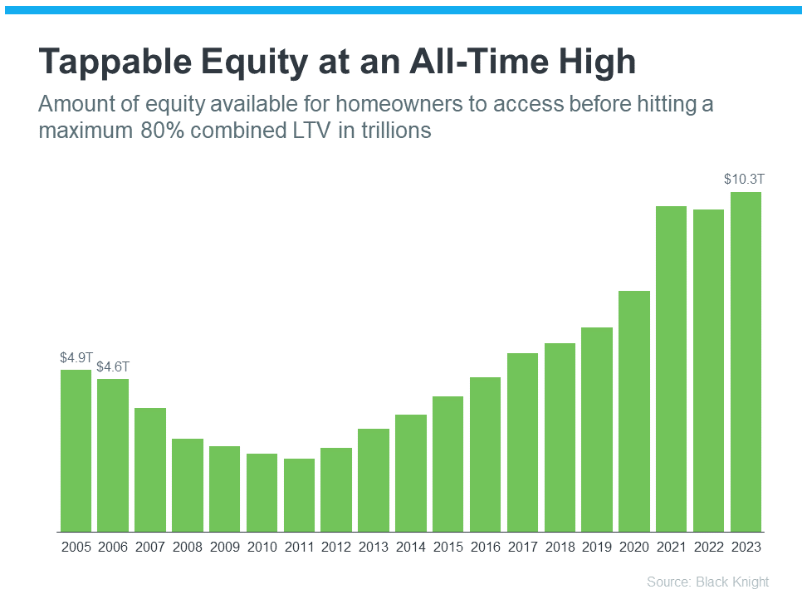

Black Knight reports that tappable equity (the amount of equity available for homeowners to access before hitting a maximum 80% loan-to-value ratio, or LTV) has actually reached an all-time high:

That means, as a whole, homeowners have more equity available than ever before. And that’s great. Homeowners are in a much stronger position today than in the early 2000s. That same report from Black Knight goes on to explain:

“Only 1.1% of mortgage holders (582K) ended the year underwater, down from 1.5% (807K) at this time last year.”

And since homeowners are on more solid footing today, they’ll have options to avoid foreclosure. That limits the number of distressed properties coming onto the market. And without a flood of inventory, prices won’t come tumbling down.

Bottom Line

While you may be hoping for something that brings prices down, that’s not what the data tells us is going to happen. The most current research clearly shows that today’s market is nothing like it was last time.

Should you wait for rates to fall before purchasing a home?

According to this article, if you’re in the market for a new home, today’s mortgage rates can hinder your efforts. After all, the higher your mortgage rate, the higher your monthly payments will typically be. So, it can be difficult to find affordable housing options in today’s high-rate environment.

But the good news is that there are still good housing options available. And, while waiting for a lower interest rate might seem like a smart move, some experts say doing so would be a mistake. But why wouldn’t you want to wait for lower mortgage rates before you purchase a new home?

Why some experts say you shouldn’t wait for mortgage rates to fall

Interest rates are a common consideration among home buyers — but should you wait until mortgage rates fall to buy? Many experts say no. Here’s why.

Lower rates could lead to lower inventories and higher prices

“Buying a home is a big decision that needs careful consideration,” says John Dustman, SVP, head of consumer lending and advisor banking at Axos Bank.

“One common concern among buyers relates to market conditions and how changes in interest rates impact home prices and inventory levels,” says Dustman. “As most house hunters know, inventory levels in just about every community in the U.S. are very low and have been since the COVID-19 pandemic and historically low mortgage rates available in 2020 and 2021.”

“Active inventory fell to levels that were a third or less than inventory levels in 2019 during the 2021 peak in demand,” says Dustman. “Since then, inventory levels have increased but are still at levels equal to about 50-60% of available inventory in 2019.”

Considering the low inventory levels, home prices would typically rise. However, with rates as high as they are right now, it may be keeping home values from increasing further, according to Dustman. But that may change.

“Many buyers have been waiting on the sidelines due to high rates and challenges they are facing qualifying for mortgages with high rates and home prices,” says Dustman. As rates fall and these buyers on the sidelines flood the market, inventory could fall further and home prices could rise.

That’s why, generally speaking, the best time to buy a home is when rates are higher and demand is lower, according to Dustman.

You could miss out on your dream home if you wait too long

It can be difficult to find your dream home with inventories low across most housing markets nationwide. However, if you wait too long, you could miss out entirely.

“People are always going to need to buy homes — whether they are upsizing with a growing family, downsizing as empty nesters, moving for a job or are simply ready to take the next step in their life’s journey and become a homeowner for the first time,” says Austin Niemiec, chief revenue officer for Rocket Mortgage.

“Maybe someone’s dream home becomes available and it doesn’t coincide with the most favorable rate environment, but waiting for rates to drop could mean missing out on that perfect opportunity,” says Niemiec. “As long as they can comfortably afford the payment now, the homebuyer always has the chance to refinance if rates drop in the future to get a better monthly payment.”

It’s hard to time the market

“Trying to time the homebuying market and rates is difficult because no one has a 100% accurate crystal ball to predict what conditions will look like even in a few months from now,” says Bob Driscoll, SVP and director of residential lending at Rockland Trust Bank. “The ‘perfect time’ to buy a home is a myth.”

“Instead, prospective homebuyers should buy a home on a timeline that works best for their life and future plans,” says Driscoll. “Aligning your home purchase with your goals and values will certainly have a better return on your investment than waiting around for rates to fall.”

Learn more about your mortgage options now.

The bottom line

Interest rates could drop in the future, but you may not want to wait for that to happen to buy a home. If you wait for rates to fall, you could face higher home prices or miss out on your dream home. Rather than waiting for rates to fall, it may be a wise choice to purchase your home now and consider refinancing later.

Should I Buy a House Now or Wait for Mortgage Rates to Go Down?

Contemplating the purchase of a home or diligently saving for a down payment? The recent surge in mortgage rates may have prompted a crucial question in your mind: Is now the best moment to invest in a home, or should you bide your time until mortgage rates go down?

In order to assist you in making an informed decision that aligns with your family’s best interests, let’s dive into the financial aspects—without any intimidating mathematical complexities. Together, we’ll explore whether the current circumstances favor your home-buying endeavors or if it might be prudent to defer this decision for a more favorable period.

Let’s take a look at what financial Guru Dave Ramsey had to say about this question:

Should I Buy a House Now or Wait?

Yes, you should buy a house now if you’re financially ready to do so. Here are the biggest reasons why that’s the best move:

- If interest rates continue to drop, then house prices will start going up. Lots of folks haven’t been able to afford a house because of high interest rates, so they’ve been sitting and waiting. As rates keep getting lower, more and more of those people will start buying homes—and sellers will be able to raise their prices because of that increase in demand.

- You can always refinance down the road. If you buy now and interest rates continue dropping over the next year or two, you can still take advantage of the lower rates by refinancing your mortgage. On the other hand, if you wait to buy and home prices go up, you’re stuck with the higher prices.

- Mortgage interest rates may be high right now, but they’ve already begun to drop. That means, if you buy now, you’ll already be getting a better deal than you would have in 2023.

- The Federal Reserve (also known as the Fed) is unpredictable. We never know exactly what the Fed will decide to do with the federal funds rate, which directly impacts mortgage rates across the country (more on that later).

Here’s the deal, though: You should only buy a house if you’re prepared financially. How do you know if you’re financially ready to buy a house? Let’s break it down.

Am I Prepared Financially to Buy a House?

If you’ve checked these four boxes, you’re in the clear to buy a house!

- You’ve paid off your debt. Focus on paying off all your consumer debt before you buy a house. Getting rid of student loans, credit card payments and car notes will give you more margin in your budget—and that’s super important as a homeowner.

- You have a full emergency fund. Saving up an emergency fund of 3–6 months of your typical expenses before you buy will be the difference in whether a broken HVAC unit, fridge or washing machine is a catastrophe or merely an inconvenience.

- You’ve saved a strong down payment. If you’re a first-time home buyer, you need a down payment of at least 5–10%. But if you can swing a 20% down payment, that’s even better. Why? Putting 20% down will keep you from having to pay for private mortgage insurance (PMI), an extra monthly fee that could add hundreds to your house payment.

- You can afford the house payment. Don’t buy a house if the monthly payment (including principal, interest, homeowners insurance and HOA fees) on a 15-year fixed-rate mortgage would be more than 25% of your take-home pay. Any more than that, and you run the risk of not having enough money left in your budget each month to put toward other important financial goals—aka, you’ll be house poor.

If you haven’t checked one or more of those boxes, that’s where you need to direct your focus for now. We know how badly you want to be a homeowner and start building equity. But we talk to people every day who bought a house before taking those steps and wound up regretting it because they got stuck with a giant, expensive burden.

Will Mortgage Rates Go Down in 2024?

Yes, mortgage rates are expected go down in 2024. Average U.S. rates for both 30-year and 15-year fixed-rate mortgages began steadily dropping in November 2023, and that trend continued into January 2024.2 Rates will likely keep going down throughout the rest of the year, especially since the Fed projected that it will lower the federal funds rate three times in 2024.3

But even as mortgage rates continue to go down in 2024, odds are the drop won’t be drastic—it’s not like rates are going to quickly return to the 2–3% range we saw at the end of 2021. The bottom’s not about to fall out here.

For example, even though the National Association of REALTORS® believes rates will go down in 2024, they’re only predicting a 1.2% drop (from 7.5% to 6.3% for 30-year mortgages) by the end of the year.4 A lower rate is definitely nice, but that small of a drop would only save you a couple hundred bucks on your monthly payment, if that.

It’s a discount, sure, but it’s not worth waiting around for—especially since, like we talked about earlier, you can refinance down the road.

How Do Federal Interest Rate Hikes Affect Mortgages for Home Buyers?

When interest rates go up in the real estate world, so do monthly payments and the total amount of interest you’ll pay on a mortgage. How much? Here’s an example.

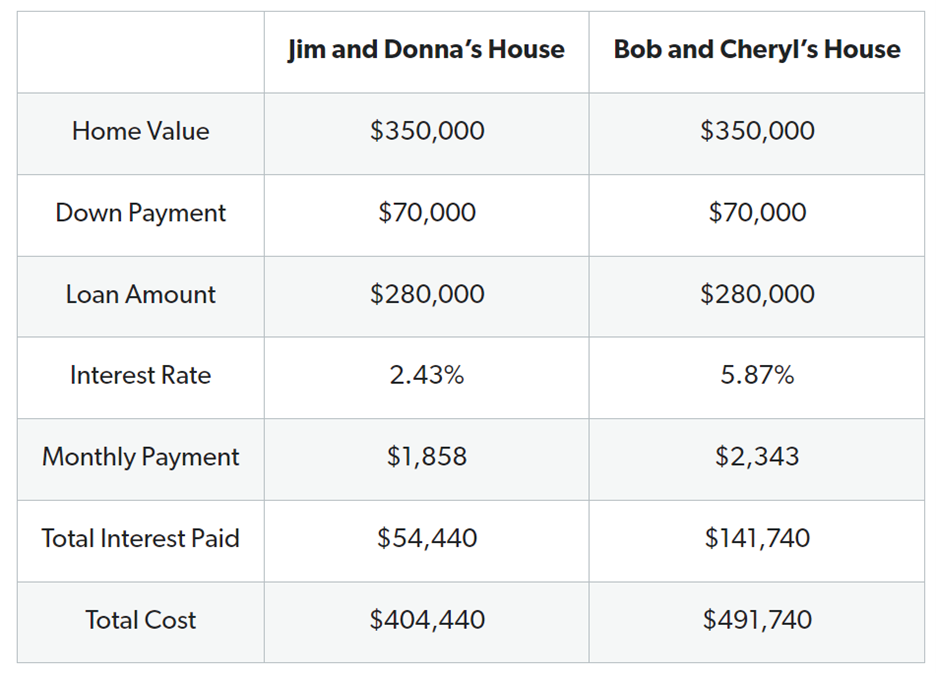

Let’s say we have two couples who each bought $350,000 houses with 20% down and 15-year fixed-rate mortgages. Couple #1, Jim and Donna, bought their house in January 2022 when the typical interest rate was around 2.4%. Couple #2, Bob and Cheryl, bought their house less than two years later in January 2024—when the average rate was nearly 5.9%.5

We used our Mortgage Calculator to see what both couples will pay for their houses. To keep things simple, we left out costs for property taxes, homeowners insurance, and homeowners association (HOA) fees.

Bob and Cheryl will pay over $90,000 more in interest than Jim and Donna—even though their home value and loan terms are the same. Plus, Bob and Cheryl’s house payment is over $500 more per month. Ouch!

What Is the Federal Reserve?

Okay, we’ve mentioned the Fed a couple of times and talked about how interest rate hikes can affect you. But what is the Fed anyway?

Well, the Federal Reserve is the U.S. central bank that creates money and sets interest rates. Its main goal is to keep the economy running smoothly by having low unemployment and low inflation.

The Fed is kind of like a mechanic who tinkers around with a car to make it purr like a kitten, and one of its favorite tools is (shocker) interest rates.

Why Does the Fed Raise Interest Rates?

The Fed raises interest rates to encourage people to borrow less, spend less and save more—which should slow down inflation.

Now, the Fed doesn’t tell commercial banks what interest rates to charge on loans, but they do influence the banks’ rates by setting their federal funds rate. The fed funds rate is the interest rate banks charge to each other for overnight loans, and it influences most other interest rates.

So, even though the Federal Reserve doesn’t actually set mortgage interest rates, its decisions can still affect your mortgage. For example, mortgage rates went up in early 2022—even before the Fed started raising rates. That’s because banks saw what was coming and started upping interest rates to protect their profits.

The Bottom Line

No one likes it when interest rates go up, but it’s not the end of the world. This is still a great time to buy a house—you’ll just pay more than you would’ve a couple years ago. It’s also a good time to sell a house. And if you already have a fixed-rate mortgage locked in, you’re in good shape too.

While it’s smart to get the lowest possible interest rate on your mortgage, that doesn’t mean you have to wait years to buy or sell a house—or to refinance if your current loan just isn’t working for you. You get to decide when to buy a house based on what’s right for you and your family, not what the Fed is doing.

Frequently Asked Questions

Will the Fed raise interest rates again?